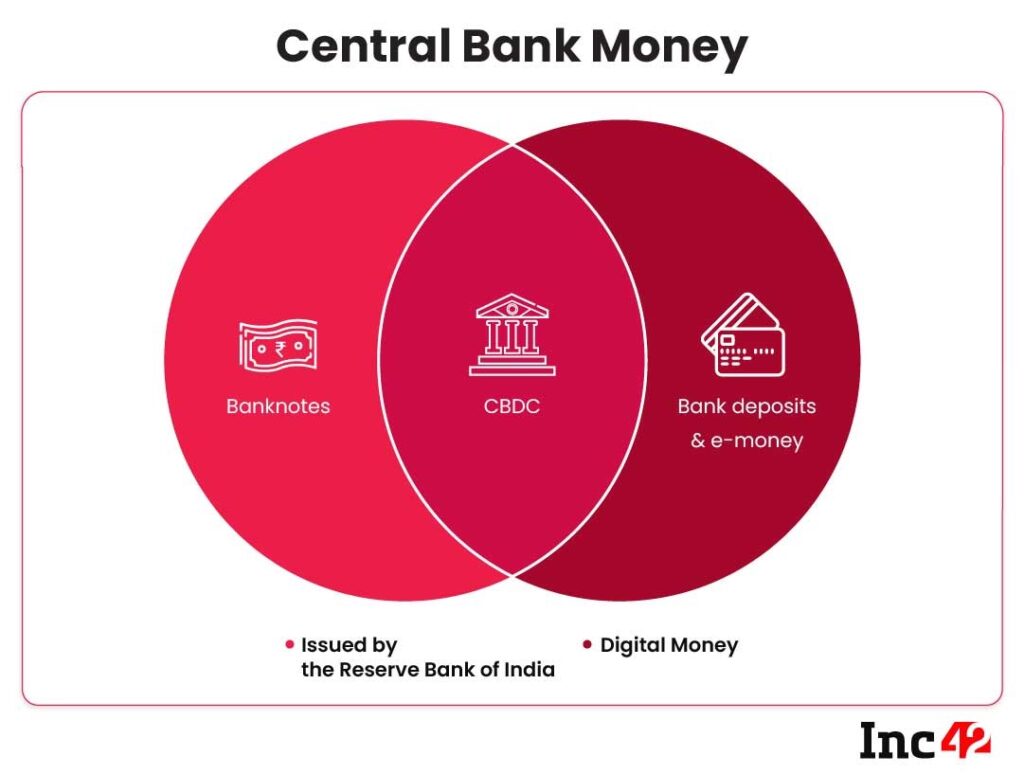

According to the RBI, “CBDC is the legal tender issued by a central bank in a digital form. It is the same as a fiat currency and is exchangeable one-to-one with the fiat currency.”

Source - Inc42

A government-issued currency is known as fiat money. It is viewed as a form of accepted legal tender for the exchange of goods and services. Banknotes and coins served as the traditional forms of fiat money, but technological advancements have made it possible for governments and financial firms to add digital currency to the system.

Although tangible currency is still extensively accepted and exchanged, its use has significantly declined in several advanced economies, a tendency that increased during the COVID-19 pandemic. Digital currencies and cashless societies are now becoming widespread as a result of the development and adoption of cryptocurrencies and blockchain technology. As a result, central banks and governments all over the world are looking into the use of digital currencies that are backed by the government. These currencies, like fiat money, would have the complete trust and support of the government that authorized them when and if they were adopted.

A Central Bank Digital Currency is a nation’s fiat currency in digital form. A country’s central bank or monetary authority issues and controls CBDCs. Many nations are creating CBDCs, and some have even put them into practice, to see how their economies, current financial networks, and stability will be impacted.

How CBDCs differ from current electronic payments

Banking solutions have been at the core of all the digital payment formats currently in use. You require a bank account to move cash from one account to another. An account is required even for wallets, cards, and UPI payments. The associated commercial banks are responsible for these account transfers. However, until and unless it is actual cash, customers cannot engage in direct transactions for which the Central Bank is liable. The Central Bank or RBI in the case of India will be responsible for CBDC’s obligations. Making digital payments might not require having a bank account, unlike making traditional digital transactions.

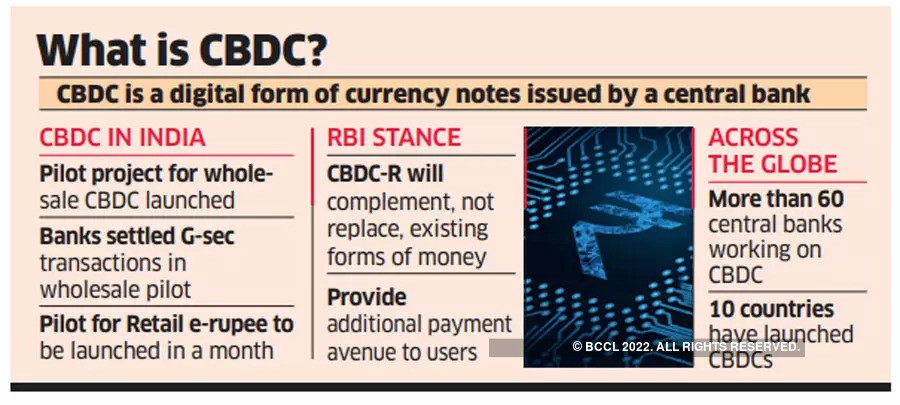

RBI’s CBDC - e₹

The digital rupee, or CBDC, would be issued by the RBI in the upcoming fiscal year, according to a statement made by Finance Minister Nirmala Sitharaman during her Budget speech on February 1.

“Introduction of Central Bank Digital Currency (CBDC) will give a big boost to the digital economy. Digital currency will also lead to a more efficient and cheaper currency management system. It is, therefore, proposed to introduce Digital Rupee, using blockchain and other technologies, to be issued by the Reserve Bank of India starting 2022-23,” – FM Nirmala Sitharaman

Source - Economic Times

The first wholesale CBDC pilot has been launched by RBI.

CBDC wholesale transactions resemble keeping reserves in a bank. An institution receives a bank account from the central bank to deposit money into or utilize to complete interbank transfers. Then, central banks can control lending and set interest rates through instruments of monetary policy like reserve requirements or interest on reserve balances.

On November 1, 2022, the first pilot for the Central Bank Digital Currency (CBDC), also known as the Digital Rupee for the wholesale segment (e₹-W), commenced. Nine banks have been chosen to participate in the pilot project, including the State Bank of India, Bank of Baroda, Union Bank of India, HDFC Bank, ICICI Bank, Kotak Mahindra Bank, Yes Bank, IDFC First Bank, and HSBC, according to the RBI.

Source - Corporate Finance Institute

RBI is in the final stages of the CBDC pilot rollout

Retail CBDC, in contrast to wholesale CBDC, is a form of currency that has been distributed to the general population. It is based on distributed ledger technology, or DLT, and has traceability, anonymity, and availability around the clock and throughout the year. It also has the potential to be used for an interest rate application.

In general, a currency is always released by the Reserve Bank at the wholesale level and subsequently travels to designated institutions to reach retail hands, unless and until we are discussing a type of DBT (direct benefit transfer).

People informed of the developments indicated that the Reserve Bank of India (RBI) is nearing completion with the launch of the retail central bank-backed digital currency, which will be compatible with the current forms of payment systems. According to officials, the CBDC platform will resemble the UPI platform already in use and will be hosted by the National Payments Corporation of India (NPCI). With 10,000 to 50,000 users for the pilot projects, the central bank urges each bank to test the retail CBDC.

Source - Insights IAS

Conclusion

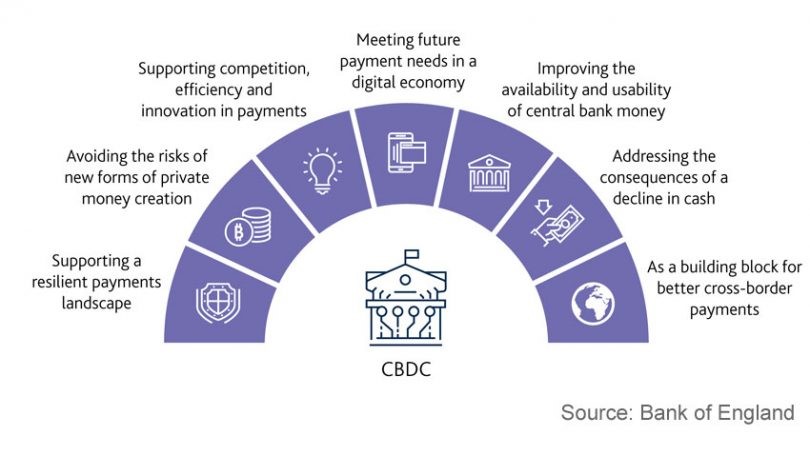

Faster than anyone could have predicted, people and businesses are adjusting to digital forms of financial transactions. The advent of CBDCs is a game changer for the financial ecosystem since it promotes payment efficiency and adds another operational and technological option to the existing money paradigm. Understanding CBDCs’ capabilities and the effects they have on the larger payments landscape is crucial in light of this.

In conclusion, given their ability to ensure efficient international payments, CBDCs may be the next significant development in the financial sector. Additionally, users can benefit from speed and security for their transactions.