In the year 2008, a company called Foodiebay was established. It was renamed Zomato Media Pvt. Ltd. in 2010. Zomato began as a restaurant finding application and website, founded by DeepinderGoyal and PankajChaddah. It has about 3.5 million active restaurant listings as of 2020. We met the Zomato delivery lad in 2015, when the company extended its delivery service to compete with Swiggy. Zomato is one of India’s most popular online food delivery services.

If you enjoy ordering meals or dining out, you have probably heard of Zomato. The business has been in operation for 13 years. Food delivery, restaurant listings, ratings, and dine-out services are currently available to customers in 526 cities across India and 24 countries across the world. However, India accounts for 90% of the company’s income. Zomato also boasts 3.5 million active restaurant listings that use the network to gain clients and build their business.

Source – Index Daily &The Morning Context

Where does Zomato earn from?

1. Zomato Pro: It is a premium paid membership service. It has 1.4 million subscribers as of December 2020. 2. Hyperpure: It is a programme in which the corporation offers raw ingredients to restaurants as a subsidy. It works with around 6000 restaurants in six locations. 3. Food delivery service: It makes money via delivery fees and restaurant commissions. 4. Dining out: Where people utilise it to find new restaurants to eat at. 5. Business consulting services: Provides insights to organisations using its client database.

Strengths

1. Zomato’s network effect: As more individuals use Zomato, more restaurants add their establishments, bringing in even more customers. 2. It employs around 1,61,637 active delivery executives (as of December 2020), who complete 94.9 percent of orders in less than 30 minutes. 3. Strong brand recognition in India: Significant customer retention has resulted in increased income as clients increase their spending. 4. Zomato’s valuation is higher than the combined price, yet its financials are less enticing. 5. Zomato (60,000 cr) > Jubilant Foods (41,500 cr) + Burger King (6,400 cr) + Westside Development (7,900 cr) + Barbeque Nation (3, 400 cr) 6. With only 8% of total internet users in India ordering food, there is a significant opportunity for growth, since countries like the United States and China have roughly 53% and 38%, respectively.

Weaknesses

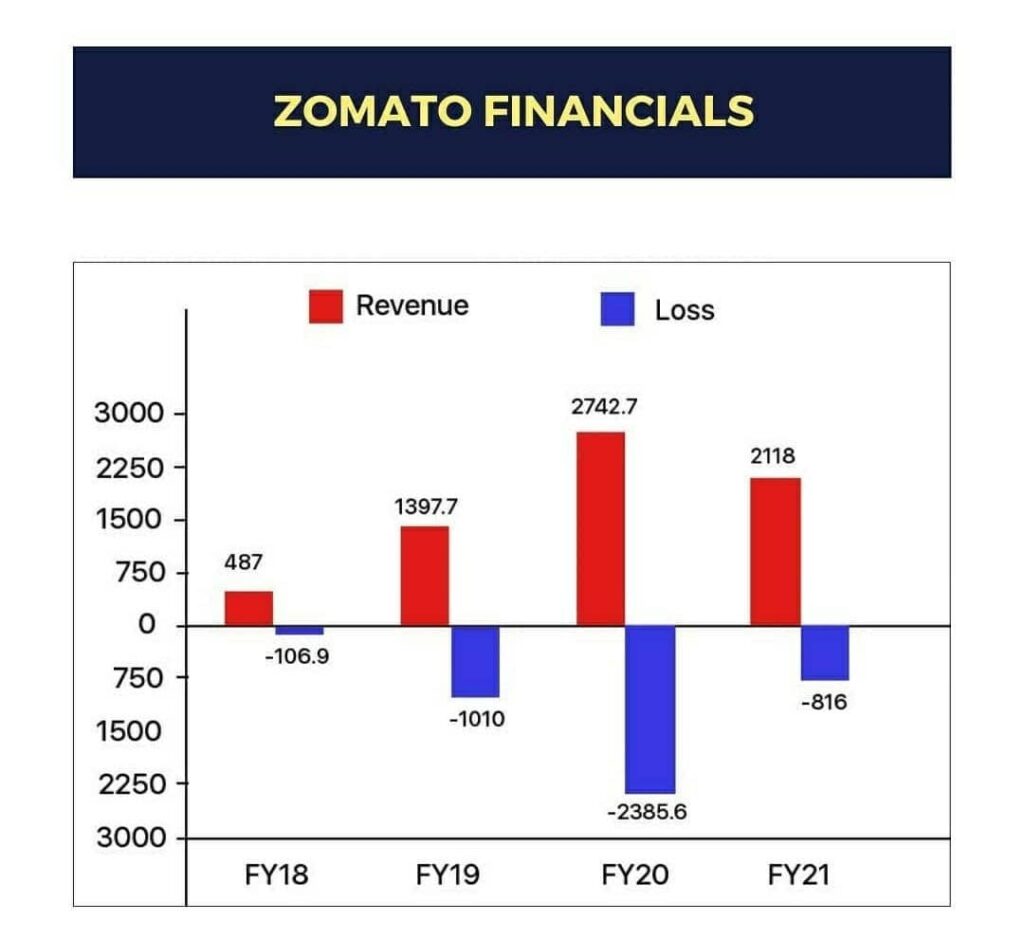

1. It has not turned a profit. This could continue because the corporation has budgeted for expenses. In each of the four years, the company’s expenses exceeded its revenues, resulting in a loss. 2. Swiggy is a major competitor to Zomato, and with Amazon and JIO reportedly in talks to enter the food delivery sector, any meal delivery company may find it difficult to sustain profit margins and thrive. 3. Zomato, which is backed by Jack Ma, has stated that it will remain a foreign-owned and controlled corporation. This means it falls under the FDI policy and other foreign investment legislations.

Source – Invest Therapy

Source - Invest Therapy

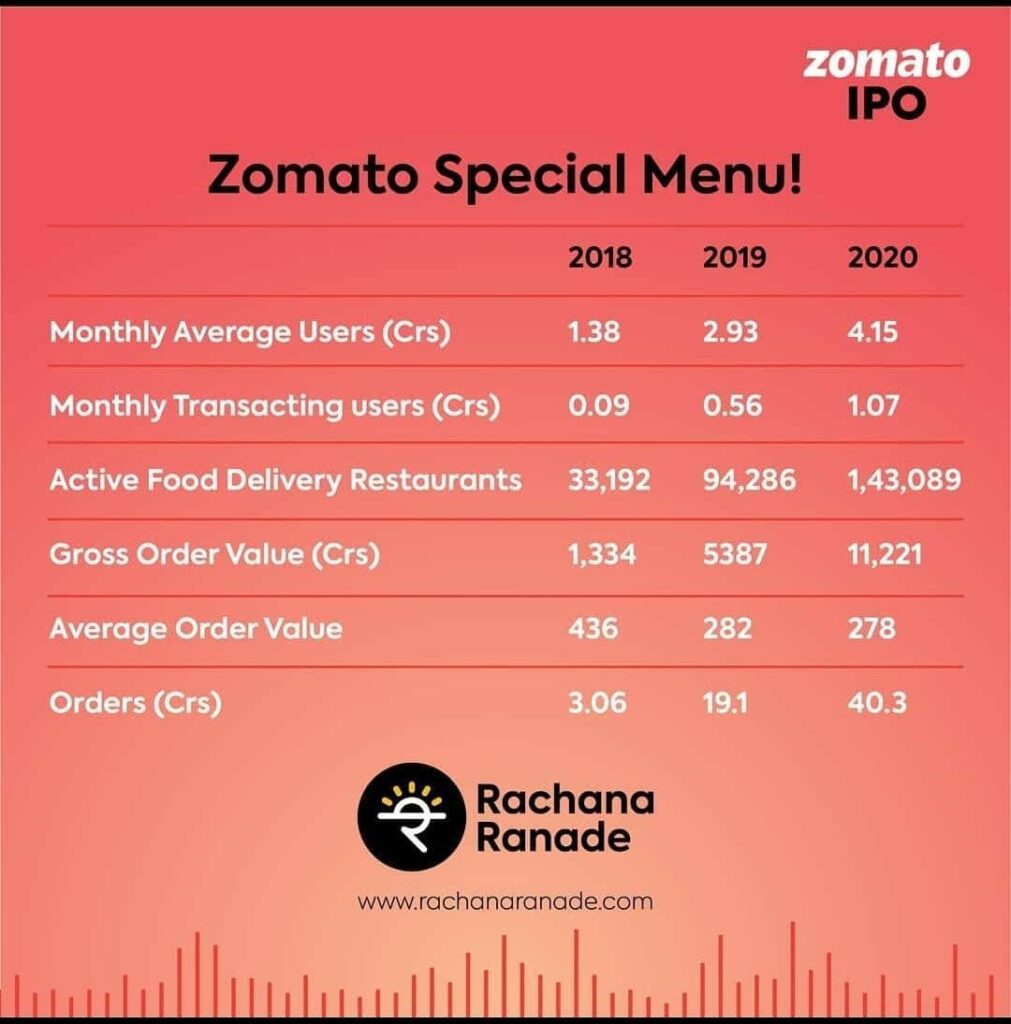

Zomato has grown from a promising young start-up to a blooming giant in the previous few years. In 2020, the company expects to process close to 400 million orders, up from 30 million in 2018. From a mere 1,400 crores in 2019, to upwards of 2,700 crores the following year, Zomato has come a long way from working with a few thousand restaurants to around 4 lakhs.

The much-anticipated IPO of Zomato is poised to enter the markets, thanks to the approval of market regulator SEBI. With the IPO of Zomato, India has entered a new period in which a new generation of companies aiming for hyper-growth at the expense of cash flow will list on the Indian stock exchanges. Zomato’s IPO will usher in a new age of technology firms in the same way that Infosys’ IPO did in 1993. Because it is the first online aggregator unicorn to list, it has created a lot of buzz in the industry.

Source - RachanaRanade

In FY19, Zomato’s average order value (AOV) was Rs 264.6. In Q3, FY21, the figure was Rs 407.8, and in Q4, FY21, it was Rs 394. As the name implies, the average order value is the total value of all orders placed on the app. So, if you have three orders with values of 200, 300, and 400, you have a total of three orders. In this scenario, the average order value is $300.

But there is a catch: if the average order value continues to rise, Zomato will have a higher chance of breaking even and possibly profiting on each order. The higher the average order value, the higher the commission collected on that order. Zomato’s AOV has been steadily increasing over the last two years, which is a positive sign.

The argument is simple: Zomato spends roughly the same amount of money transporting a $100 order as it does a $500 one, i.e., the costs are the same. However, by claiming a commission on the whole order amount, they get more money from the $500 order. A 20% commission on a total of $100 equals $20. When an order is valued at $500, the commission is increased to $100. The second transaction is a more profitable venture, and if clients seek out more expensive orders on a regular basis, you will observe an increase in average order value.

As a result of the higher AOV, Zomato’s unit economics will improve. This is the way to profit, and it is exactly what happened during the pandemic.

Source - Invest Therapy

Zomato lost roughly Rs 30.5 for every order they served in Financial Year 20. During the first few months, there was a noticeable drop in gross order value (GOV). Zomato has made a full recovery from the pandemic. The order volume dropped dramatically at the start of the pandemic. Following the first wave of pandemic, the volume increased dramatically in the months that followed. The organisation is currently making a nice sum of Rs 22.9 for every order they deliver in Financial Year 21. The margin is predicted to rise as the average order value rises.

Zomato plans to use the net proceeds from the new offering to fund organic and inorganic growth efforts (totalling Rs 6,750 crore) as well as general company purposes. Over the last several months, the company’s income has risen rapidly across all its business verticals, yet it lost money in FY21. While the company generated Rs 1,367 crore in revenue in the first three quarters of FY21, excessive expenses resulted in a loss of Rs 684 crore.

According to experts, the IPO can bring good listing returns, but considering their pricing and profitability, holding it for the long term may be a big challenge. “These types of companies will invest all their profits into acquiring customers, difficult to estimate when they make real profits”, says Ramdeo Aggarwal of Motilal Oswal.

They have also just invested in Grofers and may soon begin dabbling in online grocery shopping. However, the food delivery company is currently the sole thing that dominates the top line, that is how the company will be valued.