Would the United States have been in such a position if the coronavirus never occurred? Would they have eventually gotten into such an economic turmoil? In my opinion, the difference would have been in magnitude and speed, by looking at the data; in my previous articles, one can see that things were getting much stretched:

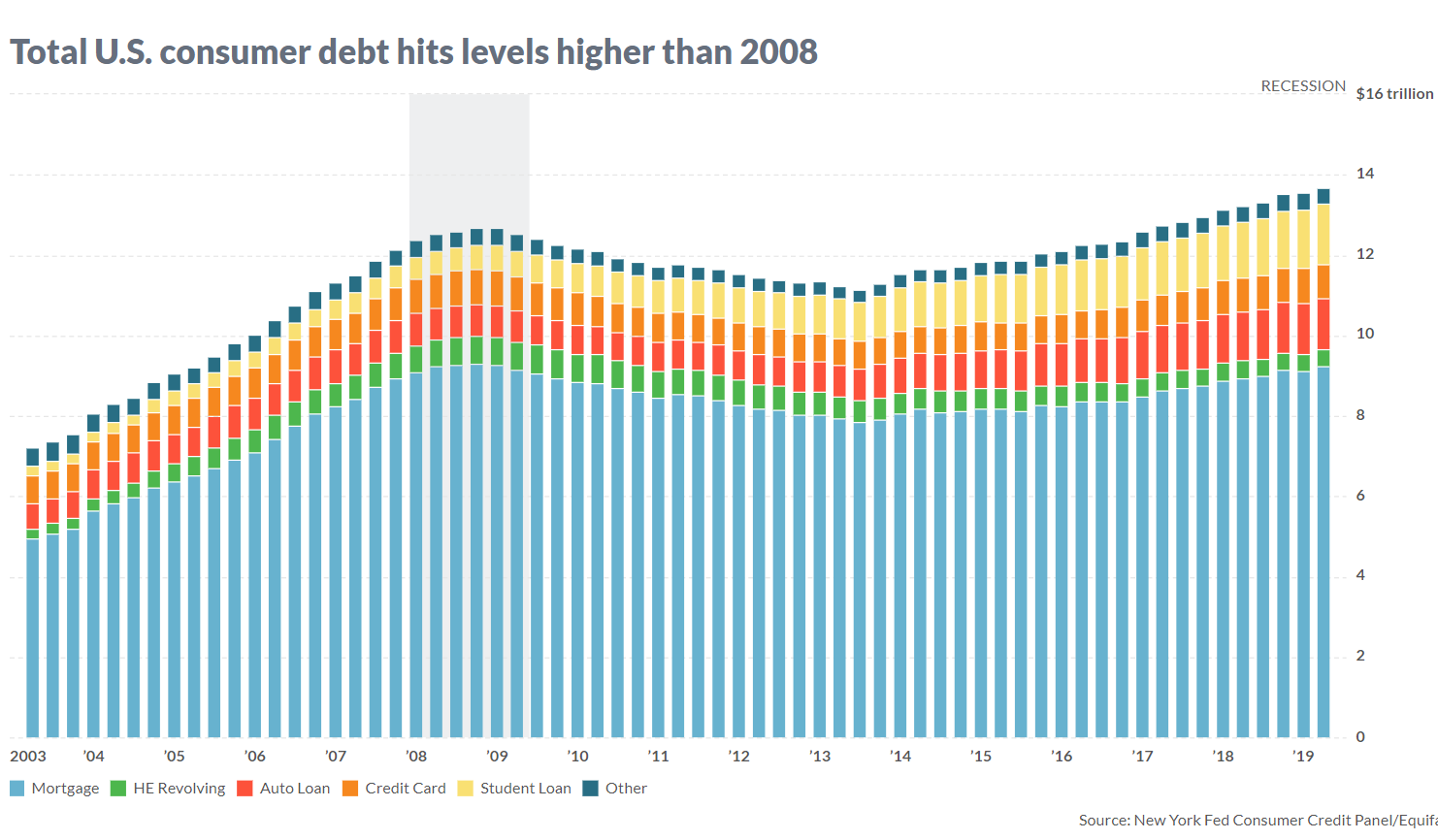

Consumer debt is higher than it’s ever been – Personal Consumption typically forms two-thirds of the US economy, that’s the way it’s been year-in and year-out for a very long time. But in 2019 personal consumption rose to about 90% of the US GDP as the federal reserve did everything they could to elevate the stock market, kept risky assets’ prices up, and people kept ‘feeling’ wealthy because they looked at their 401k and spent beyond their means. The Federal Reserve would have probably been able to float the financial markets through the next election because they were so aggressively keeping interest rates at artificially low levels. They were so aggressively growing their balance sheet, even though they were not calling it quantitative easing; however, because of all this, the bubble was getting inflated in the corporate debt market and the stock market. It was a ‘slow-moving’ slowdown, but it was definitely a slowdown. Apart from the USA, this slowdown was happening in Germany, China, and India as well.

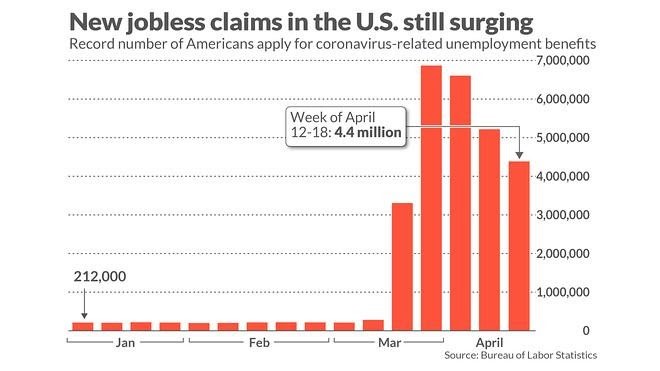

If you had looked at the employment sector pre-coronavirus, there was weakening at every front of the job market. Right now, there are predictions that the unemployment rate could approach great depression era levels in the USA. At the apex of the great depression, 1 in 4 Americans were out of work. Two weeks into the shutdown due to the coronavirus pandemic, there were close to 10 million jobless claims; approximately 1 in 16 Americans were already unemployed, and this only worsened as more and more states in the USA went into lockdown. This is a cultural shift which is taking place in the USA; it is unlike any generation has seen since those who survived the great depression

Let’s say that the worst of the virus has passed, it doesn’t mean that the economy will heal itself within months, it might take years, and that’s what people are not factoring in because if you experience something of such magnitude that it changes the way you view the world, and it changes the way you view spending, then there will be a shift in the mind-set of people on how they view money. There are two waves:

Wave1: The fear among people in terms of being in densely populated areas and events post the coronavirus pandemic. This is the initial fear factor, which is short term.

Wave2: The second wave is what comes after this initial fear factor – it is a realization on the part of an average working person that they need to save more in the future. This wave has both short term and long term implications. In the short term, it’s going to mean that the recession we’re in is going to be more protracted and drawn-out than what many are assuming right now as the ‘worst case.’ The long term implications will turn out great as the savings rate in the economy will go up, and people will become more frugal in the way they approach everyday purchases.

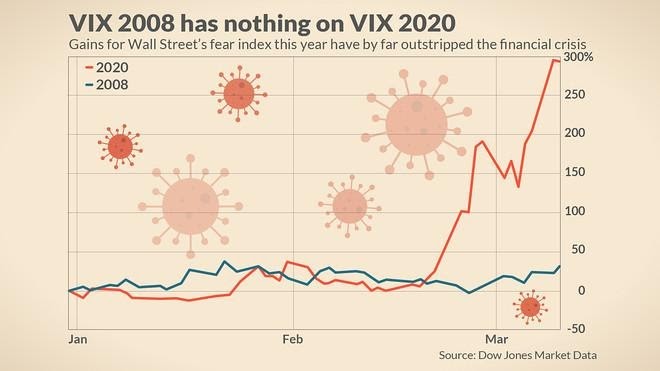

What we are experiencing right now with the whole coronavirus situation is very dynamic, and hence to draw any stubborn conclusion would be foolish. But, when a country’s fundamentals are weak, such as the USA, one cannot avoid contemplating whether that country truly is a ‘safe’ haven.

Written By:

Raghav Agarwal

Citations:

Bohn, H. (2011). The Economic Consequences of Rising U.S. Government Debt: Privileges at Risk. FinanzArchiv / Public Finance Analysis, 67(3), 282-302. Retrieved May 2, 2020, from www.jstor.org/stable/41303592

•Schwarcz, Steven L., Rollover Risk: Ideating a U.S. Debt Default (January 30, 2014). Boston College Law Review, Vol. 55, No. 1, p.1 2014. Available at SSRN: https://ssrn.com/abstract=2307569 or http://dx.doi.org/10.2139/ssrn.2307569

•Vuletic, Dominik, Next Global Crisis: Greatest Recession in the History of Capitalism is at the Doorstep (September 21, 2015). Available at SSRN: https://ssrn.com/abstract=2663630 or http://dx.doi.org/10.2139/ssrn.2663630

•Lo Duca, Marco and Nicoletti, Giulio and Martinez, Ariadna, Global Corporate Bond Issuance: What Role for US Quantitative Easing? (February 18, 2014). ECB Working Paper No. 1649. Available at SSRN: https://ssrn.com/abstract=2397787