The Covid-19 pandemic has compelled the global economy to kneel and seek mercy from one of the most fatal problems that the human race has ever dealt with. The water is so deep, that in an age of robust digitization and affordable internet access, economies are working towards de-globalization. In other words, the pandemic has dented spirits across the board and nations fear interdependencies of any sort, especially apropos to trade and commerce.

While the world is battling a multitude of issues, back home the Indian economy has its own set of worries to fret over. Besides the fact that the GoI’s effort to contain the spread of the virus is turning out to be futile, there seem to enough and substantial economic and geo-political pain-points for the policy-makers to address.

Apart from the spread of the coronavirus disease, the anti-China narrative is gripping ground across the nation and perhaps the globe, with The United States having long-drawn trade issues with the Chinese coupled with the fact that it is the originating source land of Covid-19. When it comes to the Indian policy-makers, they are doing every possible thing under the sun to cut-off its ties from the Red Dragon nation and become ‘Aatmanirbhar’, post a filthy border spat with the in-news Asian counterpart. Excluding the political aspect of this narrative, optimists look at the situation as a perfect time to woo global investors and world-class organizations from China, the world’s second-largest economy, into India and provide the economy with the much-needed impetus.

However, to achieve this, the policy-spearheads need to have some serious deliberations. On account of this, the GoI has come up with Production-Linked Incentives (PLIs) to provide an overall enhancement mechanism to the participating players in specific, and the ecosystem in general. The start has not been bad as we have seen heightened interests from global electronics manufacturers, including the likes of Foxconn Hon Hai and Pegatron, to set up local manufacturing units in the country, eventually giving massive boosts to the circumscribed scheme of things. Another green flag in this pursuit has been the transfer of powers from the Ministry of Finance to the Reserve Bank of India (RBI) as far as dealing with Foreign Direct Investment (FDI) regimes is considered. This move will help iron out the extra couple of months these investment processes were subject to, wearing out positive sentiments.

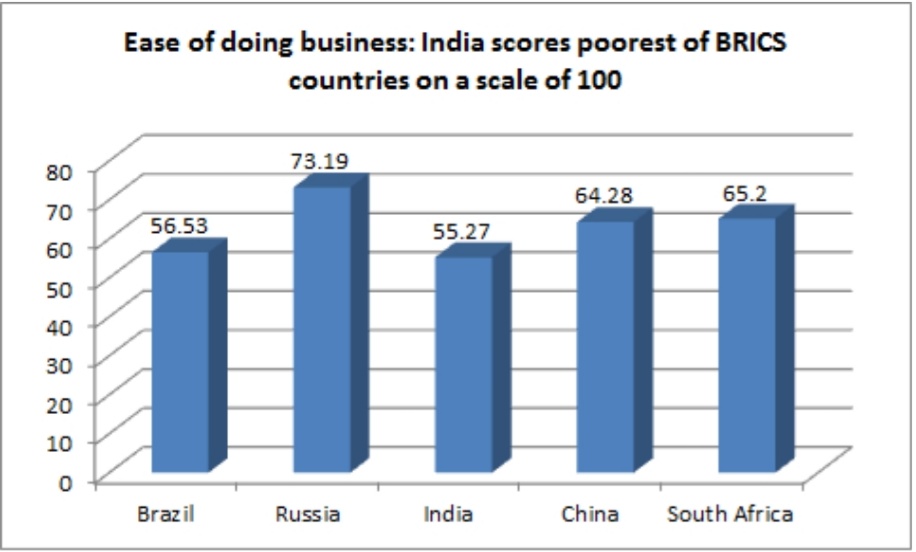

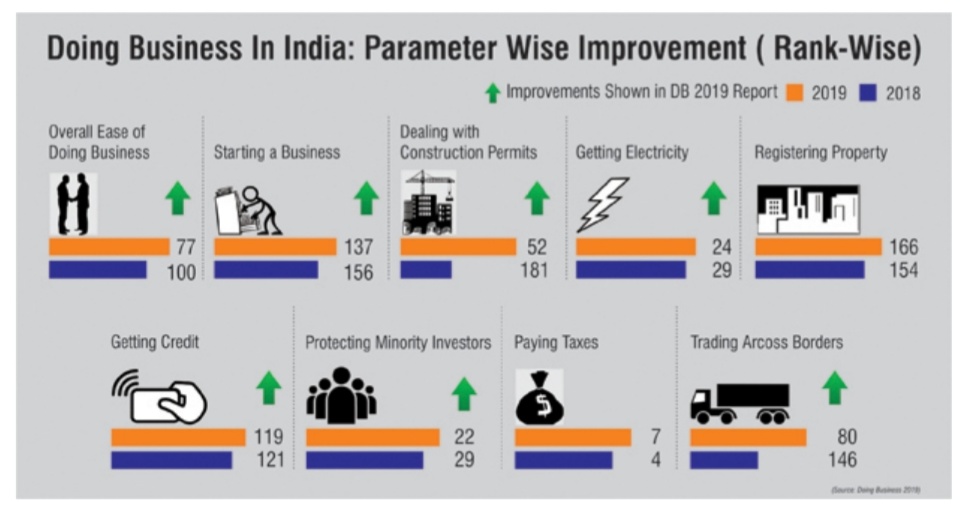

What is the idea behind all of this? The idea is simple and that is to enhance the ease of doing business and investing in India. Are we making progress in that direction? Not sure. India, as an economic centre, has always been a victim of long-drawn and unnecessary approval nomenclatures. While the regulatory bodies view it as a structure, investors view it as a dis-incentive. The sooner they realize this, the better will be the outcome. Because believe it or not, we are living in an age where we expect our business deals to get closed at the same time we expect our pizzas to get delivered.

To put things into perspective, the same aforementioned electronics manufacturers have raised concerns vis-à-vis the multiple approval system that the Indian authorities have in place. The divided approval mechanism between the centre and the states is bugging these investors, paving the way for fractured investor sentiments. Albeit the Department for Promotion of Industry and Internal Trade (DPIIT) is making efforts to get a nationwide single-window clearance system, Investment Clearance Cell in situ, the timeline projected is another six months. Now, that is a fairly long time and who even knows that we might end up missing the bus altogether.

The fact that emerging and accessible nations like Vietnam and Singapore are delivering strong competition in terms of providing flexibility in conducting business operations, especially relating to the Asia-Pacific region, connotes the importance of India’s need to be agile and proactive. A lot depends on the non-domestic capital inflows tap and if by any means that runs dry, one could witness lethargy in the spirits of domestic players too.

Notwithstanding a host of adverse marks that the coronavirus pandemic will leave on the Indian economy, we as the citizens and as administrators of the country must start to assume responsibilities in a much more disciplined fashion. The first half of the new decade has painted a squeaky-clean picture, accentuating the preponderance of unity as a nation at this crucial juncture. Many a time we have worked our ways through cosmetic lip service, but unfortunately, this crisis won’t let us get away easy. The way India gets out of the tunnel post the pandemic will only go forward to determine her future on a global scale. The only set of words that I can leave you with is from the great Netaji Subhas Chandra Bose and he said, ‘No real change in history has ever been achieved by discussions.’ Perhaps, it’s time to introspect.

Written by- Shyam Agarwal

Imagery Sources:

- Financial Express;

- Textile Excellence.