?Introduction:

The word has it all .Reserve Bank of India (RBI) holds on to this policy as it introduces a new system for commercial banks to sanction all new loans linked with MCLR . Marginal Cost of Funds based Lending Rate (MCLR) is applicable on and after 1 April,2016. Altering the existing lending rate system followed by all banks across India.

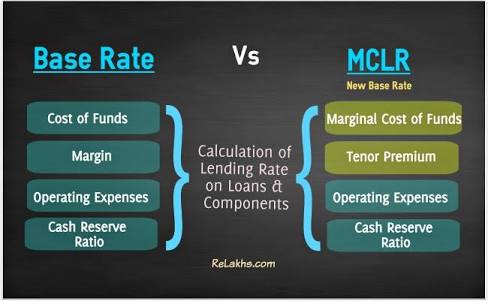

Previously the Banks did not pass on the rate cuts to the borrowers. Before MCLR, lending rates were related to Base Rate . There was only one base rate for all the loans .

Loans were given at base rate + Spread. This Spread was constant during the term of the loan. If the bank reduced Base Rate, interest rate on both new loans and old loans will go down. In case of rate cuts by the Reserve Bank, banks could always say that even though the cost of fresh borrowing has gone down, they have deposits for which the interest rate remains high.

To offset this quick transmission of interest rate cuts, RBI has introduced MCLR so that banks links their lending rates to marginal funding costs (cost of fresh or incremental borrowings).

MCLR counts these two factors:

- Interest rate offered by banks on deposits and;

- Repo rate that banks furnish to obtain funds from the RBI, necessary for calculation.

Why MCLR?

Last year, the RBI exaggerated the changing rate cuts with regards to its base lending rates. However, the banks were slowly adopting these rate cuts and the RBI had to repeatedly reprove the banks for their atypical delay. Repo rates kept changing, but the banks were hesitant to likewise update their base lending rate and interest rates on deposits. A considerable reason for the same was that banks choose to utilize RBI’s Liquidity Adjustment Facility (LAF) in order to source their short term funds from the RBI. This saved them from timely update of lending and deposit rates. RBI is hopeful that MCLR is faster comeback to wipe out these shortcomings of the current base rate system.

Impacts on Banks

As clever as a fox, RBI has its ways . With cuts in repo rate and easy access to loan; RBI had great difficulty since bank took their own time to implement the changes with regards to their own Base Lending Rate(BLR) and interest rate on deposits. With this new lending system the banks are moreover forced to consider the current base lending rate while calculating their own MCLR.

It forces the banks to line up their interest rates on a monthly basis. The banks can subscribe to the latest repo rates and implement the same, also keeping up with RBI’s updates.

In this fast-pacing economy, a cut in the base lending rate at the apex bank level must reach the common masses in the shortest time frame. Rate cuts encourage people to subscribe to loans and invest in the popular investment options. As luck would have it, this is only possible when banks implement said rate cuts in a quick, uniform and responsible way. MCLR is conceived to encourage the banks when it comes to adopting the latest repo rates as endorsed by the apex bank of India.

Features of MCLR

Banks must revise MCLR on a monthly basis, while including the latest RBI repo rates as part of the calculations.

Marginal cost includes interest paid on cost incurred in maintaining the Cash Reserve Ratio and are factored while calculating lending rates.

Marginal costs must also be considerate to repo rates, which were not considered in the previous lending rate system.

MCLR also includes a number of contributing factors, including a range of interest rates that the bank has to satisfy in its bid to accumulate the necessary funds

MCLR must also take into account higher interest rates that apply to long term loans. This is also known as Tenor Premium.

How to calculate MCLR?

MCLR is associated with fresh (incremental) cost of borrowing. Borrowings not just consists of rates of fixed deposits. It also includes current account balances, savings account balances, wholesale borrowings, borrowings from RBI.

The various components of MCLR.

- Marginal Cost of Funds: This is cost of fresh (incremental) borrowing to the bank. It takes into account interest rates of different types of deposits (current, savings, term deposits etc). Marginal cost of funds is not just the deposits (borrowings) that the bank has accepted, it also includes some equity. Hence, cost of equity is also considered.

Marginal cost of funds = Marginal cost of Borrowing X 92% + Return on Net worth X 8%

- Negative Carry on Cash Reserve Ratio: Banks have to keep a certain level (4% as on April 5, 2016) of their deposits with the Reserve Bank. This ratio is the Cash Reserve Ratio (CRR). Banks don’t earn any interest on the amount. Essentially, they can use 96% of the deposits for lending and the remaining 4% does doesn’t provide any returns and is kept idle.

- Operating Costs: Bank’s costs are not limited to interest it pays on deposits. There are expenses on salaries, branch rent or other expenses that are not directly charged to the customers. Cost of raising funds is also included under this head.

- Tenor Premium/Discount: Higher the loan tenor, higher the tenor premium. Tenor refers to the period of interest rate reset. Even though an individual’s loan tenor is 15 years but if the loan reset is done every year, 1-year MCLR will be applicable.

How does it work?

MCLR ensures that the rates are revised based on the repo rates prevailing, the marginal cost of funds incurred by the bank and the tenor premium. This means that your bank’s lending rates could change more frequently than earlier. MCLR rates are reviewed every month but are fixed for a period of at least 1 year with respect to long-term loans.

What is meant by spread in banking terms and its impact on MCLR?

In banking terms, net interest rate spread refers to the difference between the interest that the bank earns on products such as loans and securities, versus the interest payable by it on deposits.

With relation to MCLR, the RBI stipulates that banks must add the varied components of the spread onto the MCLR when determining the applicable lending rate. This will also allow banks to charge a higher interest rate on loan portfolios wherein the borrower is deemed as risky.

What about the existing loans that comes under the range of Base Lending Rate?

RBI has a clear status-quo of Base Lending Rate. It maintains that existing loans/credit limits that subscribe to Base Rate will continue to do so, until repayment or renewal, whichever comes first. Moreover existing borrowers, in compliance with their lenders, can switch their loan from the Base Lending Rate model to MCLR. The banks will charge switching fees .

Caution : It is not likely for borrower to opt for base lending rate once it opts for MCLR.

Conclusion:

It’s too early to say whether it will do good or not but the situation with respect to lending rate will get better than before. With this new system, RBI will ensure that all the benefits pass to the populace, forcing the bank to realign its interest rate on monthly basis. MCLR adamantly forces the bank to adopt the latest repo rate. Consequently, an individual’s home loan EMIs will reflect these changes instantly.

By Vibhashi Nagda