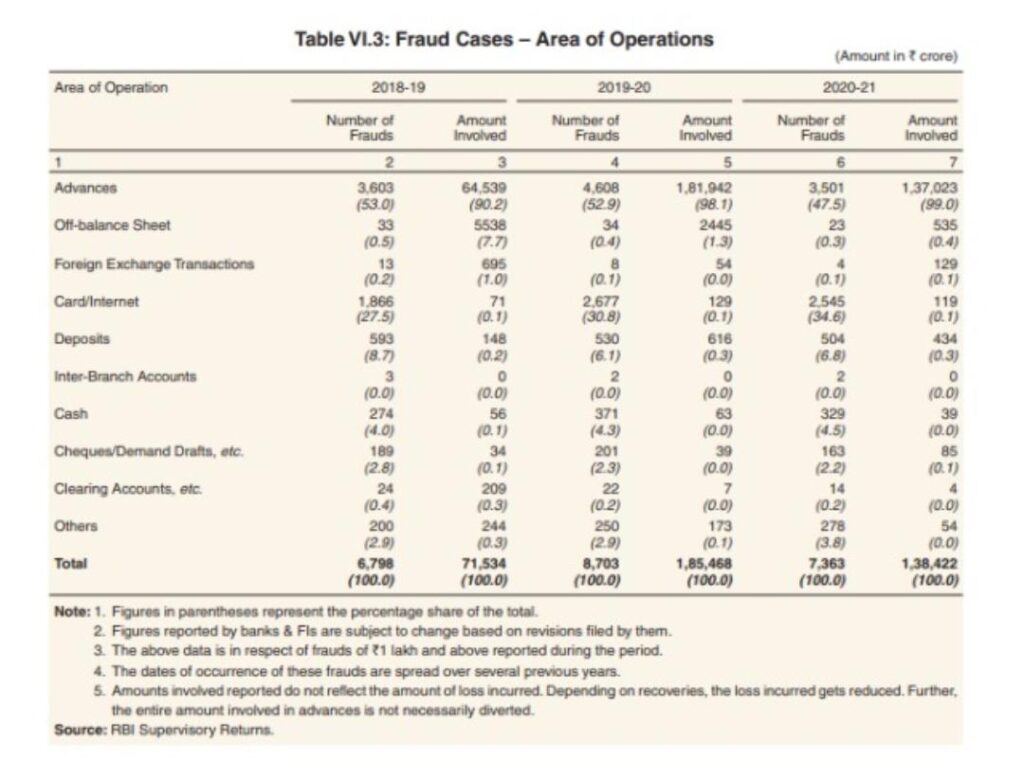

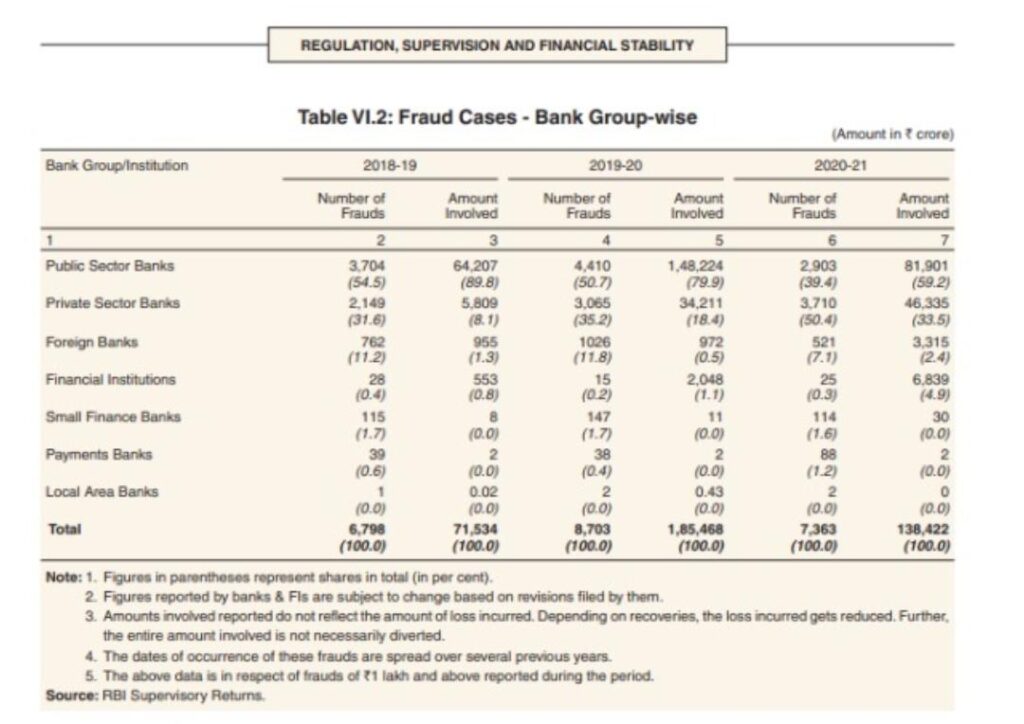

As per the RBI Annual Report 2020-21, the number of bank frauds reported during the year decreased by 15% in terms of number and 25% in terms of value, vis-à-vis 2019-20 (See tables below). The share of PSBs in total frauds (both in terms of number and value) decreased while that of private sector banks increased during the corresponding period. Even though the fraud cases seem to have been reduced, the proportion of loan frauds or frauds in advances remains substantial (98-99%).

Source – Fundstiger.com

But why are loan frauds still haunting our economy?

To start with, a de-facto definition of a loan fraud could be any fraud occurring in a loan account (i.e., advances by financial institutions). To arrive at the reasons for this problem, we would have to first look at the steps taken by the RBI to cure this malady.

On May 7, 2015 RBI, after considering the recommendations of an Internal Working Group (IWG), various banks and other stakeholders, announced a Framework for Fraud Risk Management. The following measures were stressed/introduced as an antidote-

Early Warning Signals (EWS) and Red Flagged Accounts (RFA)

An RFA is one where a suspicion of fraudulent activity is thrown up by the presence of one or more Early Warning Signals (EWS). These signals in a loan account should immediately put the bank on alert regarding a weakness or wrong doing which may ultimately turn out to be fraudulent. A bank cannot afford to ignore such EWS, but must instead use them as a trigger to launch a detailed investigation into an RFA. The framework also contains an illustrative list of EWS.

Early Detection and Reporting

The most effective way of preventing frauds in loan accounts is for banks to have a robust appraisal and an effective credit monitoring mechanism during the entire life-cycle of the loan account. Therefore, specific guidance on pre-sanction, disbursement, annual review, staff empowerment, role of auditors, incentive for prompt reporting may be provided.

Filing complaints with Law Enforcement Agencies

Banks are required to lodge the complaint with law enforcement agencies immediately on detection of fraud. There should ideally not be any delay in filing of the complaints with the law enforcement agencies since delays may result in the loss of relevant documents, non-availability of witnesses, absconding of borrowers and also the money trail getting cold, in addition to asset stripping by the fraudulent borrower.

Central Fraud Registry

RBI has designed a Central Fraud Registry (CFR), a centralised searchable database, which can be accessed by banks. The per RBI Annual Report 2020-21, one of the goals for the year was to develop a state-of-the-art single searchable CFR for SCBs, UCBs and NBFCs to assist them in taking informed decisions on providing credit.

Source – RBI

Now, considering the steps taken by RBI and their direction let us explore the reasons for loan frauds in India.

As discussed above, the most effective way of preventing frauds in loan accounts is to have a robust appraisal and an effective credit monitoring mechanism during the entire life-cycle of the loan account.Many RBI circulars and reports highlight the cracks in the current system.An RBI circular ‘Frauds-Classification and Reporting’ describes the lacunae more clearly as follows:

It has been observed that frauds are, at times, detected in banks long after their perpetration. Sometimes, fraud reports are also submitted to RBI with considerable delay and without complete information. On some occasions, RBI comes to know about frauds involving large amounts only through press reports. Banks should, therefore, ensure that the reporting system is suitably streamlined so that frauds are reported without any delay. Banks must fix staff accountability in respect of delays in reporting fraud cases to RBI. Delay in reporting of frauds and the consequent delay in alerting other banks about the modus operandi and issue of caution advices (now in CDRs) against unscrupulous borrowers could result in similar frauds being perpetrated elsewhere.

Source - RBI

Further,as per RBI annual report 2020-21, the average time lag between the date of occurrence of frauds and the date of detection was 23 months for the frauds reported in 2020-21. However, in respect of large frauds of 100 crore and above, the average lag was 57 months for the same period.

Also, fraudulent information, security provided by the borrower and insufficient oversight remainimportant reasons. As highlighted in the RBI circular ‘Frauds-Classification and Reporting’, it is observed that a large number of frauds are committed by unscrupulous borrowers; including companies, partnership firms/proprietary concerns and/or their directors/partners by various methods including the following:

i. Fraudulent discount of instruments or kite flying in clearing effects. ii. Fraudulent removal of pledged stocks/disposing of hypothecated stocks without the bank’s knowledge, inflating the value of stocks in the stock statements, and drawing excess bank finance. iii. Diversion of funds outside the borrowing units, lack of interest or criminal neglect on the part of borrowers or their partners, etc. and also due to managerial failure leading to the unit becoming sick, and due to laxity in effective supervision over the operations in borrowal accounts on the part of the bank functionaries rendering the advance difficult to recover.

In several large value frauds, serious gaps in credit underwriting standards are evident. Some of the often-seen gaps are liberal cash flow projection at the proposal stage, lack of continuous monitoring of cash flows and cash profits (EBITDA), lack of security perfection and overvaluation, gold plating of projects, diversion of funds, double financing and general credit governance issues in banks. Moreover, almost all corporate loan related fraud cases get seasoned for 2-3 years as NPAs before they are reported as fraud. (As per Chapter III: Financial Sector: Regulation and Development, of Financial Stability report June 2017)

Thus, the undertreated lacunae in the system, namely insufficient oversight, asymmetry of information on unscrupulous borrowers among banks, fraudulent details and documents provided by the borrowers become the predominant reasons for loan frauds in the banking space of India.