Coronavirus has not solely halted and affected the final public activities however additionally it’s afflicted the world economic process. The new coronavirus, that first emerged within the Chinese town of the city last December, has infected one hundred ten countries and territories globally, as per the planet Health Organization.

The virus occurrence has become one in every of the most important threats to the world economy and monetary markets. Meanwhile, fears of the coronavirus impact on the world economy have rocked markets worldwide, with stock costs and bond yields plunging. The complete world is suspending all operational activities and obligatory lockdown, in order to mitigate human resource loss. Economic contagion is currently spreading as quickly as the disease itself.

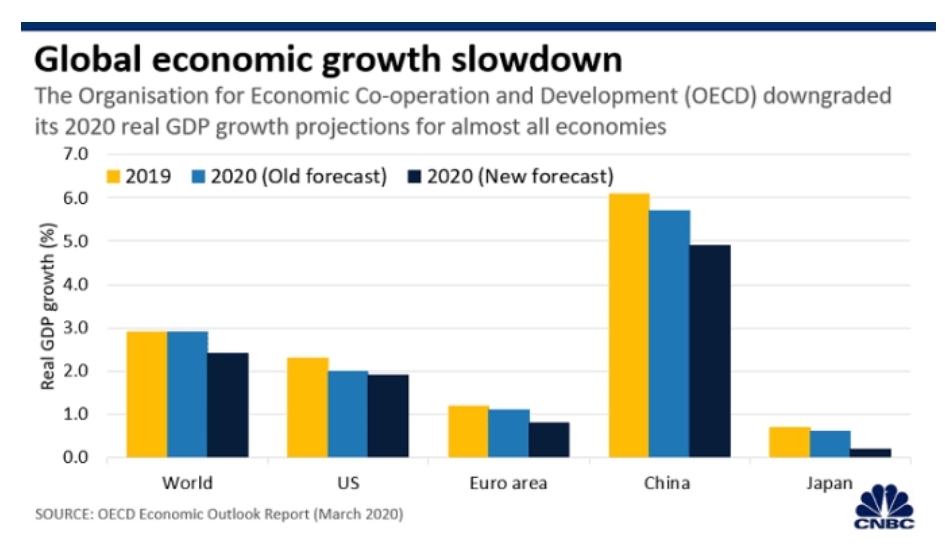

The outbreak has led major institutions and banks to cut their forecasts for the global economy. In a March report, the OECD aforementioned it downgraded its 2020 growth forecasts for pretty much all economies.

China’s gross domestic product growth saw the biggest downgrade in terms of magnitude, per the report. The Asian economic big is predicted to grow by 4.9% this year, slower than the sooner forecast of 5.7%, said OECD. Meanwhile, the world economy is predicted to grow by a 2.4% in 2020 — down from the 2.9% projected earlier, aforementioned the report. China’s manufactory activity shrunken in February, coming back in at a record-low reading of 40.3%. A reading below 50 indicates contraction.

Such retardation in Chinese producing has hurt countries with shut economic links to China, several of that square measure Asia Pacific economies like Vietnam, Singapore and South Korea. The Market Services PMI for China came in at simply 26.5 in February, the primary drop below the 50-point level since the survey began virtually 15 years past.

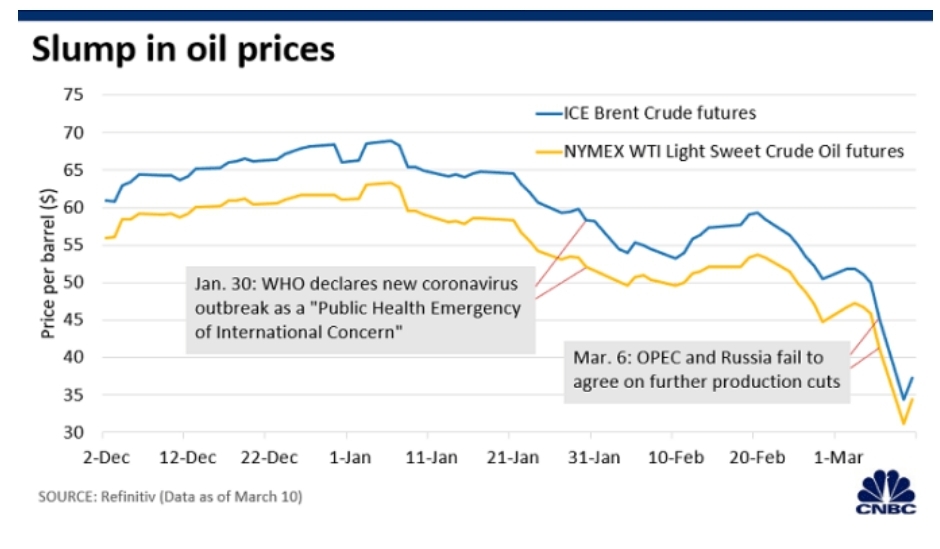

China, the geographical point of the coronavirus occurrence, is that the world’s largest fossil oil. A decline in international economic activity has lowered the demand for oil, taking oil costs to multi-year lows.

Fear close the impact of COVID-19 on the world economy has hurt capitalist sentiment and brought down stock costs in major markets. Fitch Ratings cut India’s growth forecast to 5.1% for FY 2020-21, speech communication the coronavirus occurrence is probably going to hit business investment and exports. Fitch had in Dec 2019 projected India’s growth at 5.6% for 2020-21 and 6.5% within the following year.

Supply-chain disruptions square measure expected to hit business investment and exports. we tend to see gross domestic product growth to stay loosely steady at 5.1% within the year 2020-2021 following growth of 5.0% in 2019-2020,” Fitch aforementioned.

The difficulties facing the Indian economy are exacerbated by affirmative failure, it said. “Fragilities within the national economy can more undermine sentiment and domestic disbursement. The general national economy remains burdened with weak balance sheets, which is able to limit any side to credit and growth despite policymakers’ efforts in recent months to ease stresses”, Fitch added.

Inflation and the Fed

The coronavirus crisis has created an ideal storm. Additionally, to the health consequences and human prices, it’s resulting in a severe slump. On the one hand, by preventing individuals from attending to work, inflicting them to be sick and disrupting provide chains, it’s a large shock to productivity. Kind of like associate oil value shock or a natural disaster, the restricted provide of labor and production can produce inflationary pressures. On the opposite hand, the necessity for social distancing has led to the cancellation of enormous events, ravaged the travel business, and closed businesses, restaurants, and looking centers, resulting in an outsized negative demand shock. The combination of each shock can apace increase the percent and trigger an outsized economic recession. However, the decline of each demand and provide means we should always not expect to examine the falling costs and deflation that occurred throughout the good Recession and economic crisis.

For years once the good Recession, the Fed has been attempting to elevate a rate of inflation nearer to their long objective. The coronavirus crisis may simply be the event which will offer them an excessive amount of what they had been searching for.

The aftermath of a crisis

In the short run the Federal Reserve’s emergency loaning programs can add the liquidity required to stay credit markets functioning, and therefore the planned tax rebates can facilitate people and businesses that square measure most adversely affected. Whereas each of those policies can keep demand from collapsing, lowering interest rates in response to such a health-related event won’t place infected people back to figure. Ultimately, the solution to the slump may be a solution to the health crisis, and it should return from the response of public health officers and organizations.

While the benefits of cutting a federal funds rate already close to zero are limited, there will be risks associated with the Fed’s policy in the aftermath of the coronavirus crisis. In particular, when containment is achieved, production will still be restrained by those infected and unable to work and by those displaced by unemployment and struggling to find other jobs that may not fit their qualifications. However, there will be a surge in demand as fear abates, customers return to shopping centers and restaurants, and businesses and consumers look to borrow at historically low-interest rates. Ultimately, the imbalance can produce a lopsided recovery with slow output growth with fast costs and inflation; in different words, stagflation.

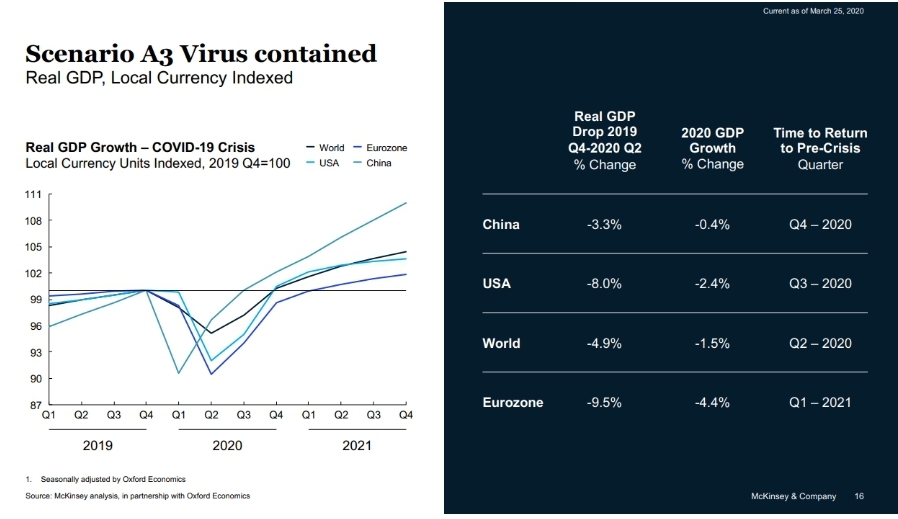

In this state of affairs, whereas the world economy would recover to pre-crisis levels by the third quarter of 2022, the North American country economy would want till the primary quarter of 2023 and Europe till the third quarter of the same year. If the general public health response is stronger and a lot of triple-crown – dominant the unfold of the virus in every country among two-to-three months – the outlook can be a lot of positive, with economic recovery by the third quarter of 2020 for the U.S.A., the fourth quarter of 2020 for China and therefore the half of 2021 for the Eurozone.

As supply chains around the world are disrupted, the report warns that the full impact is yet to be felt. Business leaders must prepare for the effects on production, transport and logistics, and customer demand. These include a slump in demand from consumers leading to inventory “whiplash”, as well as parts and labour shortages due to manufacturing plants shutting or reducing capacity.

By Sameexa R. Patel

Literary Sources: CNBC, McKinsey & Co., Wikipedia