What is the most underappreciated yet essential article in your wallet? Credit Card is a decent answer to start with. Today through popular shows and films, Credit Cards have become synonymous with shopaholism and monthly episodes of debt-induced self-loathing.

It is incredible to realize how such a simple object is the centerpiece of a financial culture that has managed to normalize and even celebrate debt of the working class, to an extent where modern-day consumer demand ceases to exist without it. And these flimsy, vibrant cards have quite a bit of history to them.

Recounting the origin of Credit Cards would be premature without examining the very idea of credit itself. The broad concept of credit revolves around the capacity to engage in purchase of goods and services under an agreement to recompense the due amount at a future date. This ability to incur and maintain debt has undeniably become the very soul of finance and economic stability and growth as we see today. It’s existence dates back to the Babylonian Civilization where the historic Code of Hammurabi established rules of loaning and repayment of debt as well as charging interest rates.

This is a remarkable development for the era, as trade was uncommon due to contemporary barter system’s limitations. The convenience of credit, alongside the inception of simple forms of money, had allowed trade and it’s benefits to bloom not only within simple settlements but between entire civilizations. It’s hard to imagine a history of humanity without such an impetus to trade, which allowed the integral exchange of cultural and scientific ideas through the ages.

Despite being a very recent iteration of the basic concept of credit, Credit Card as a distinct term appears as early as late 19th century. ‘Looking backward’ by Edward Bellamy was a novel published in 1890 which is set in a utopian society that successfully manages to bring peaceful social and economic revolution.

The book – wildly popular in it’s time – is largely forgotten now, except for an item that Bellamy had christened Credit Card, which was curiously referenced a total of 11 times in it. Being described as a card that allowed people to spend their allowance from government on purchases, Bellamy’s Credit Card was ironically more similar to Debit Card than it’s modern day counterpart.

Nevertheless, his imagination was potent enough to envision a futuristic card that will come to drastically transform the very nature of financial transactions as was perceived then.

Around the same time, crucial milestones had already been laid towards making debt accessible and affordable to public by businesses. Coins made of celluloid and metals like steel, copper and aluminum called charge coins were devised in 1860s as a simple tool to conduct credit transactions with specific businesses.

Each one was embossed with the name of the issuing merchant or establishment and a particular charge account, thus allowing credit records to be kept on the imprinted account. This would evolve into charge plates in 1928, which were made from the same material as their predecessors albeit much more sophisticated and safe.

Popularly referred to as charga-plates, they were produced by mainly departmental stores based on military dog tag system and had information such as customer name, address and even signature. While a recording purchase, the card was placed in the recess of the imprinter with a paper slip on top, thus marking the information on the card on the slip. This allowed paper ledgers of businesses to be much efficient and error-free in documenting transactions. About 300 to 500 charga-plate types are known to have existed and they remained in use till 1950s.

Another influential model came six years after the invention of charga-plate, in the form of Air Travel Card. It introduced the landmark unique numbering scheme on the card to identify customers. It allowed booking of flight based on credit as well as offer discount, making air travel in America much more convenient and widespread. By 1940s, almost all American Airline companies issued their own Air Travel Cards as they had bumped up revenue for the entire industry.

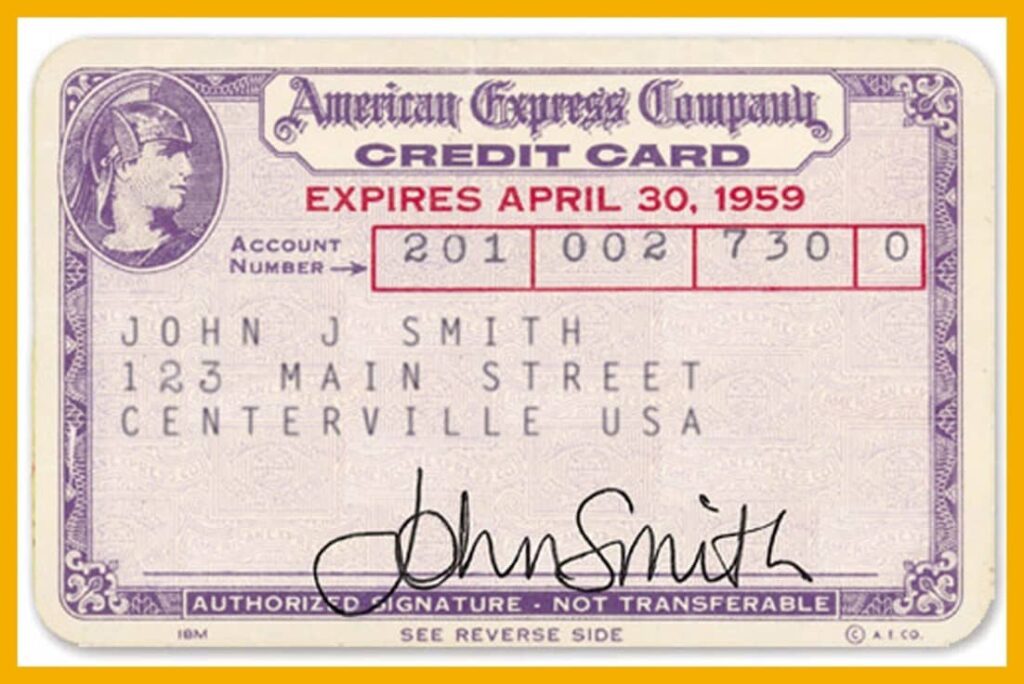

However, the more popular version of Credit Card is credited to Frank McNamara and Ralph Schneider, who founded the Diner’s Club in 1950. As the well-known story goes, Frank McNamara went to a business dinner without his wallet and like any other flustered person, ended up questioning the practicality of carrying cash at all.

This prompted him to think in terms of creating a general purpose card that could be used even if the user actually had no money. And thus was born the Diner’s Club Card, which claimed the title for being the very first Credit Card in widespread use. Early on, Diner’s Club Card was a cardboard card used for ‘travel and entertainment purposes’ with due payments having to be cleared every month.

That brings us to a very significant aspect of the Credit Cards that was still missing then. Earlier prototypes, while allowing credit transactions, required due amount to be reimbursed by customer regularly to ensure a clean slate with every statement cycle. Obviously, only people who had stable incomes could afford to actually use the Club Cards regularly.

But things came around in 1958, when Bank of America started issuing BankAmericard, which successfully introduced the practice of revolving credit. Revolving credit basically allowed credit card balances of every month to be carried forward to the next month, allowing customers to obtain a steady line of credit for a longer period of time through interest or nominal charge payment.

Initially introduced experimentally in just California, BankAmericard soon hit it off with the public like never before. It was mass-produced and mass-mailed to even consumers with a bad credit history, resulting in quite a bit of financial chaos and consequent legal regulations to mitigate a potential debt disaster. This step was big enough to allow other banking institutions, more famously Master Card and Visa to join the newly born Credit Card industry in the 1960s.

Even then, the technology behind Credit Cards was still much behind. An average usage of credit card required the merchant to call the respective Credit Card company who would have an employee manually look up and verify the details of the card. This cumbersome processing time would only come to shorten with the computerization of transactions under Visa to a remarkable window of one minute.

The real wave would come hit the shore only with the invention of chip-based processing, whose invention in 1980s was the technological advancement Credit Cards needed to attain it’s modern avatar. Finally in 1996, Europay, MasterCard and Visa co-published the standard smart chip specifications, called EMV chips.

These chip-enabled cards had the advantage of using encrypted communication rather than relying on an unencrypted magnetic stripe and became as safe as we see today. From here on out, the iconic set Credit Cards haven’t had to look back much, except for frequent technological updates.

Following the footsteps of Edward Bellamy, it’s interesting to try and predict where the Credit Card will go from here on out. In the recent years we’ve witnessed the emergence of contactless payment card – which allows transactions to be completed with just a tap to the new payment terminal and even smartphone based payment services by tech giants like Apple and Google.

It’s easy to see a future with virtual, contactless devices; some of which have already been tried and tested for easy functionality compared to the conventional methods. However transition hasn’t happened in any significant proportion as most sellers and buyers prefer the old school Credit Cards.

Some even go so far to suggest the future incorporation of Biometric technology such as through fingerprint, iris and facial recognition to enhance security of existing system. What, however, is certain is that they will inevitably continue to evolve to suit the ever-changing needs of mankind in the bigger scheme of things.

Written By – Hisham Shajahan

Edited By – Heeral Datwani