The three bank failures in 2023 did not snowball into anything similar to the 2008 crisis. Even as Silicon Valley Bank became the second-largest bank failure in US history, the Fed, FDIC, and Treasury, armed with experience from 2008, acted swiftly to ensure that all deposits — even beyond the $250,000 limit — would be insured, essentially bailing out all depositors at the bank. However, it would be naive not to take lessons from these failures and understand how regulation and monetary policy adapt to the challenges that financialization and volatile economic conditions pose to the banking system.

How Interbank Markets Work

The interbank market is where banks lend reserves to each other. The transactions in this market are fast, large denomination, short-maturity transactions. The transactions, even though international in nature, usually take place in dollars. To understand these bank failures and the role of monetary policy in preventing systemic crises, we need to emphasize how the central bank intervenes in the interbank market to achieve its monetary policy objectives. Central banks set their target interest rate range (for example, the Fed Funds rate in the US). This is the key rate of the central bank and is closely watched by market participants as it sets the benchmark for all rates in the economy.

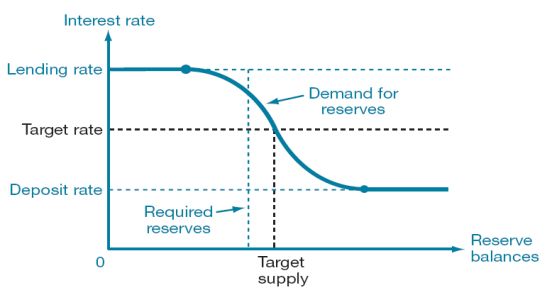

Nowadays, central banks have decoupled this rate from the liquidity in the interbank markets by using the channel or floor system of monetary policy. As the figure below shows, this system involves the use of an interest rate paid on excess reserves as the lower bound and the conventional discount window rate (the rate at which the central bank lends in the interbank market). The interest paid on reserves decouples the target rate from the liquidity in the interbank market by incentivizing banks to hold their excess reserves with the central bank instead of offering them in the interbank market, thereby inducing downward pressure on the target rate. This explains how central banks have been able to raise interest rates aggressively in response to the pandemic supply shock without unwinding their post-2007 Quantitative Easing (QE) policies.

The key lesson, however, from the mechanics of the reserve market is that banks’ risk appetite is determined by the wider nature of how the central bank conducts monetary policy. While the interest rate on reserves does decouple monetary policy from reserve availability, years of QE have radically transformed banking behavior as banks search for higher yields.

QE & Unstable Deposits

Another critical issue, pointed out in this study by former RBI Governor, Raghuram Rajan, relates to the issue of uninsured deposits. Naturally insured depositors are certain of getting up to $250,000 in case of a bank failure, making them less likely to participate in a run. However, ninety percent of SVB’s deposits were uninsured. This, coupled with the nature of depositors (majorly tech startups), meant that SVB faced a devastatingly rapid withdrawal demand and failed to raise sufficient capital or obtain enough reserves to prevent the bank run from perpetuating into a bank failure.

Further, uninsured deposits usually rise when the Fed engages in Quantitative Easing. By purchasing securities on the longer end of the yield curve and flooding the banking system with reserves, the Fed indirectly drives the increase in flight-prone uninsured deposits. Naturally, as the Fed embarked on the most aggressive tightening since Volcker brought the economy to a standstill three decades ago, these deposits were going to be the first to be withdrawn. Note also that SVB was hamstrung in its ability to fulfill these withdrawal requests as it had heavily invested in long-term bonds whose value fell as interest rates rose. The regulators and SVB failed to appreciate the interest rate risk of investing in longer-term bonds, probably because they believed that the era of loose monetary policy would continue well beyond the pandemic. Further, the high-interest rate environment also hurt the profitability of the SVB’s tech startups and other depositors, which further incentivized the run.

Regulatory Failure

Another chink in the armor of the Fed that the SVB failure revealed was that while big banks are subject to stress tests, smaller banks like SVB are not. Stress tests are conducted by the Fed to evaluate how a bank would perform under certain economic conditions such as high-interest rates, recession, or the failure of other systemically important banks. The aim of the stress test is to evaluate if a bank has sufficient capital, access to reserves, and is prudently managing risk. There is a strong case for extending such stress tests to smaller banks too.

Clearly, there’s a case for attributing blame to the Fed for how its unconventional monetary policy incentivized more risk-taking from banks. By no means does the role of the Fed, however, imply that the officials at SVB are without blame. As discussed above, they chased higher yields and failed to appreciate the supply disruptions that the pandemic would cause and the Fed’s monetary policy recourse in response to such disruptions.

Instead of appreciating the role of monetary policy in influencing banking behavior (with debatable outcomes on the wider economy), the general public seems to have ignored what was the second-biggest bank failure in US history simply because the regulators bailed out depositors. Replacing the problem of too big to fail by bailing out depositors essentially creates a too-many-to-fail problem whereby depositors will chase the highest possible yields assuming the implicit guarantee of even their uninsured deposits.

Conclusion

Financial regulation and monetary policy are continually evolving in a world with dynamic geopolitical conditions, technological developments, and constant financial innovation. Undoubtedly, we cannot expect regulators to get it right all the time. However, that doesn’t negate the fact that such circumstances will warrant volatile monetary policy if conventional macroeconomic thinking is to be followed. We shouldn’t be surprised if this volatility comes with unexpected consequences in the banking sector.

Perhaps it’s time to reevaluate the more flexible, transparent, and targeted system of influencing the economy — fiscal policy.

Written by – Rohan Dubey

Edited by – Khalid Khursheed