Out of all the jargon of the financial industry, ‘shadow banks’ confuses most. Why, if you may ask- Well, these institutions look like a bank and even act like one; but are not actual banks. There is a fine line between a traditional bank and a shadow bank. In fact, as the name suggests, these banks quite literally operate in the shadows, out of the eyes of the regulators, mostly. For instance, two of the most well-known NBFCs– Lehman Brothers and Bear Stearns ended up being at the epicentre of the 2008 financial crisis. Additionally, a few of them are even responsible for some of the biggest banking scams to date not just in India but across the world.

Coined in 2007 by the economist Paul McCulley, the term ‘shadow banks’ refers to a collection of non-bank financial intermediaries (NBFIs) that offer services similar to traditional commercial banks, but operate outside the scope of traditional banking regulations.

So, what makes a shadow bank different from a commercial bank? It’s the fact that these institutions typically don’t have banking licenses and in spite of that they aren’t illegal, however, their activities are subject to the rules and regulations of the country they are operating in.

While commercial banks are government-authorized financial institutions that provide a range of banking services to the public, such as accepting deposits- by way of FD, savings account, etc., granting loans, and offering various banking products and services; NBFCs engage in the business of loans and advances, acquisition of shares/ bonds/ securities, leasing, hire-purchase, insurance business, chit fund, etc

Also, NBFCs are not allowed to accept deposits from the public. Instead, they raise funds from the public, either through bonds, or other financial instruments or take loans from traditional banks.

Commercial banks are regulated and supervised by central banking authorities. They need to comply with certain regulations, maintain reserve requirements, and follow specific guidelines issued by the regulatory authorities. In contrast, NBFCs, have relatively fewer regulatory restrictions.

The DHFL Scam

It might have just been this key characteristic of NBFCs that led to the biggest scam of the banking industry in India- The DHFL scam. The company is said to have cheated banks out of Rs.34,000 Cr.

DHFL, once known for being a prominent housing finance company in India, and providing loans for home purchases; now holds the number one position in the list of frauds in India -topping ABG Shipyard scam of Rs. 23,000Cr, Nirav Modi scam of Rs. 14,000Cr and Vijay Mallya scam of Rs. 9,000Cr.

So, how did this scam take place?

While expanding its operations, DHFL had taken loans amounting to Rs 43,000Cr from a consortium of 17 banks between 2010 and 2018. To perpetrate this scam, DHFL had set up a dummy branch that existed only on paper. It was a virtual account carved out in the internal loan management software. They made it seem as if they disbursed home loans to 2.60 lakh individuals. Instead, they lent out the money to 91 shell companies, which in turn routed the funds back to the promoters.

This scam highlighted broader issues of corporate governance and regulatory oversight in the Indian financial sector, specifically in NBFCs.

Another major scam that caused a significant loss of confidence in India’s NBFC sector is the IL&FS scam.

The IL&FS Scam

Infrastructure Leasing & Financial Services (IL&FS) was again a NBFC with a significant presence in infrastructure financing. It had borrowed extensively to fund these infrastructure projects and ended up with an outstanding consolidated debt of Rs. 94000 Cr.

So, what went wrong and how did IL&FS start to default on its loan?

Well, the primary reason would be the asset-liability mismatch coupled with inadequate risk management practices, which refers to a situation where the maturity or cash flow patterns of an NBFC’s assets (loans and investments) do not align with those of its liabilities (borrowings and obligations). IL&FS had borrowed money by way of short-term debt instruments- like Commercial Papers, whose maturity period can only be up to one year; and used that money to fund long-term projects.

This strategy of using a high level of debt and very little equity worked as long as the projects generated revenue, but it became unsustainable when many of them faced delays and cost overruns. As a result, IL&FS started defaulting on its loan repayments worth thousands of crores, starting from August 2018 but did not disclose these defaults promptly. This lack of transparency led to a false impression of the company’s financial health.

So, when the news about IL&FS, a systemically significant Core Investment Company with the Reserve Bank of India, defaulting on its loan repayments broke, it set the Indian market in a frenzy.

Additionally, when ICRA, a rating agency, reduced the ratings of both short-term and long-term borrowing programmes due to defaults; it instilled fear among equity investors and put other non-banking financial institutions in danger due to a default scare.

Consequently, NBFCs struggled as investors withdrew substantial sums from significant NBFCs, especially housing lending institutions. This led to a severe funding shortage in 2018 and the NBFCs experienced a liquidity crisis.

This liquidity crunch severely impacted the economy and industries that significantly rely on NBFC lending, like commercial real estate, consumer durables, and cars.

On the brighter side of things, the administration of NBFCs has come under stricter scrutiny in the wake of the IL&FS disaster. The Indian government and RBI took measures such as providing liquidity support, implementing stricter regulations, and facilitating asset sales to stabilize the NBFC sector.

Conclusion

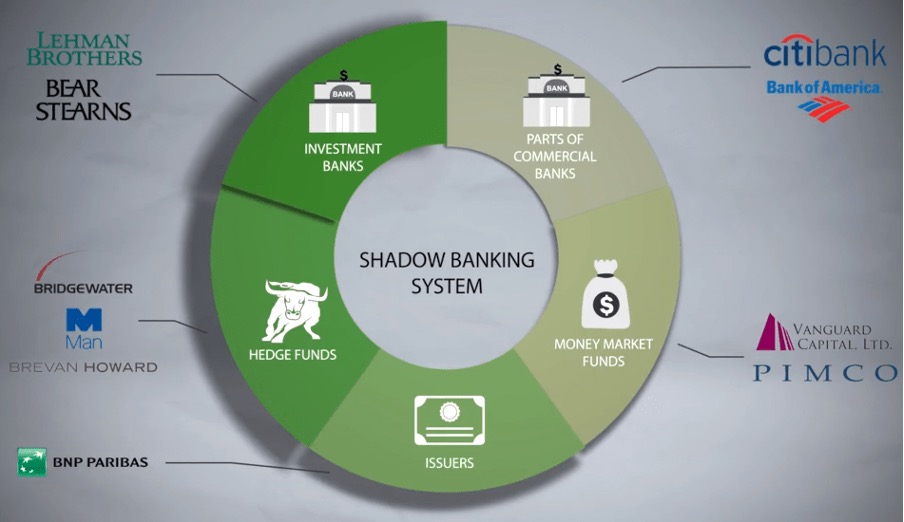

The origins of shadow banking can be traced back to the increase in demand for credit and financial services that traditional banks were unable to fully meet. Shadow banks, such as investment banks, hedge funds, money market funds, and specialized lending institutions, stepped in to cater to this demand and provide alternative funding options. Additionally, shadow banks often rely heavily on short-term funding and may be more vulnerable to liquidity risks. However, over the years, there has been a significant increase in non-bank mortgage lending.

Overall, the rise of non-bank lending reflects the evolving landscape of the financial industry, with non-bank lenders playing an increasingly important role in meeting the diverse financing needs of individuals and businesses. It is a trend that merits attention from policymakers, regulators, and market participants to ensure a balanced and resilient financial system.

Written by – Shambhavi Gupta

Edited by – Saba Godiwala