As the Reserve Bank of Australia has announced a tenth consecutive interest rate hike to counter an inflation driven largely by factors outside of its control, or susceptible to its hikes, it may be appropriate to see just how much damage it has done to Australian citizens. The data below shows how the RBA has not only managed to crush consumer sentiment and demand but also set the Australian economy on a sustained path to below trend growth.

While the RBA Governor was announcing the hike, the RBA released its usual publication suite used to justify the rate hike.

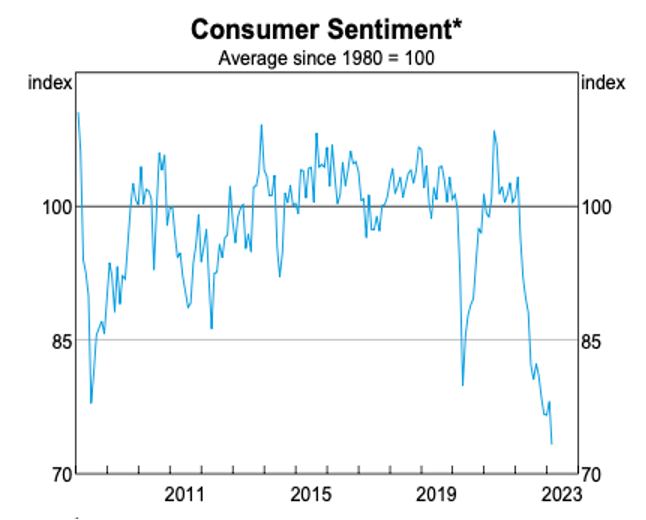

One of the graphs from the publication show just how brutally the RBA’s rate hikes have depressed consumer sentiments, to levels far below that seen ever in the aftermath of the 2007 Financial Crisis and the pandemic :-

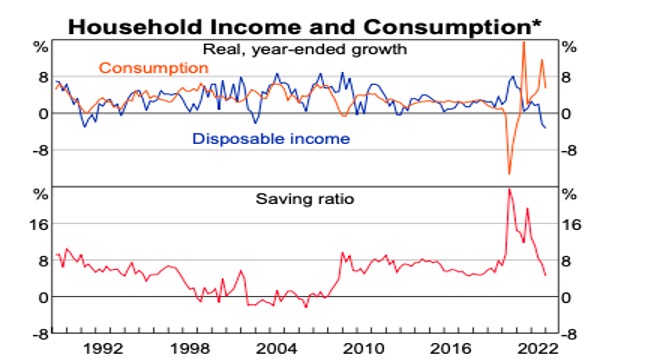

If that was not enough, the graphs below indicate how household disposable income and spending have plummeted. The graphs below show the aggregate picture, therefore it’s important to remember that the situation may be much worse for low income households:-

Perhaps it’s no surprise that the RBA failed to adjust nominal disposable spending for population growth in its press release, even then the picture looks bleak.

Over the 12 months to December 2022, real Household disposable income per capita has fallen by 4.9 per cent, which is a disastrous decline commensurate with the deepest recessions in recent history. As shown by the graph below, the only time disposable income fell by such a high level was during the 1982 recession, meaning that the RBA has engineered a higher fall in disposable income than even trumps the fall in the aftermath of the Financial Crisis.

Further, the RBA predicts that the economy will continue to grow well below trend for the next “couple of years.” An assessment which comes at a time when the Australian economy grew at a rate of 2.7% yearly, well below its trend of 3.2-3.5%, which will likely result in rising unemployment over the next few years.

All of the data is indicative of an Australian economy that has been pushed into an unnecessary slump by the RBA- and they’re not quite done yet.

Justification for the Rate Hikes

In the backdrop of the data above, it would seem that the RBA would have very little scope for justifying their rate hikes, nevertheless, their justification at least proved that the RBA is oblivious to the damage it is doing.

The RBA Governor claimed that inflation is by far the biggest evil and that he is willing to push unemployment as high as possible to tame inflation.

That statement, by extension, implies that the data above is likely to get even worse and the Australian economy will continue to be mired with low growth.

Note that while monetary continues to squeeze households, increasing the interest rate implies that the RBA will pay a higher interest rate on the reserve (known as ES in Australia) balances that banks maintain with the RBA, which are already in excess as a consequence of the RBA’s bond buying spree during the pandemic.

Which once again shows that not only is monetary policy a blunt tool but also one that has negative redistributional effects.

The Governor’s justification becomes even more perplexing when the RBA admits that inflation in Australia has peaked and inflation expectations remain well anchored.

Regardless, it looks like the RBA is set to continue on its misguided path until households are further drained of their savings and the economy is tipped into a recession.

Cherry-Picking Data

The RBA then went on to justify its hikes by stating that unemployment remains at a 50-year low, and that Australia is at full employment.

Why the RBA only picked a 50 year period, instead of 60 years, when Australia’s unemployment was around 2% is anybody’s guess.

Further, it is flawed to say Australia is at full employment when the current unemployment is at 3,7% and underemployment is at 6.1%, meaning that the economy is well short of full employment levels.

The RBA also states that data shared to it by corporations shows a dangerous wage pressure which could induce a wage-price spiral.

Needless to say that this data has not been released to the public.

These justifications from the RBA only serve to misguide the public debate on inflation. The claims of being at full employment only provides cover for corporations to increase their markups and further squeeze households.

Conclusion

All the data and RBA’s meek and unsubstantiated justification only expose the very characteristics of monetary policy that make it a poor counter stabilisation tool- it is redistributional towards the wealthy, operates with long lags, and has many negative unintended consequences- such as rising unemployment.

However, after ten hikes, there is little reason to believe that the RBA will realise this.

Till then, banks will continue to cash in on higher reserve payments, corporations will use inflation as a cover to raise prices and households will be forced to dig into their plummeting savings, and the Australian economy will continue to grow substantially below trend, and full employment will remain a pipe dream.

Written by – Rohan Dubey

Edited by – Shamonnita Banerjee

*This article was written in February 2023