In February 2023, Union Finance Minister Nirmala Sitharaman announced the Union Budget 2023- 2024 which included some important changes and features in terms of the tax structure. One such change was the policy defining the 20% TCS on Foreign Remittances under the Liberalized Remittance Scheme (LRS), which will come into effect from 1st July, 2023.

What is meant by TCS?

TCS, short for Tax Collected at Source, is a sort of tax collected by the seller from the buyer on selected goods and services. When speaking in terms of Foreign Remittances, this tax is collected from a person when they send money abroad, which is not restricted to sending money to someone but can also include taking an overseas trip, buying of assets, purchasing of goods, etc.

Why was TCS increased from 5% to 20%?

Primary answer is to increase the tax revenue on part of the government. The other reason is the increase in outward remittances over the past year—in the financial year 2022, outward remittances hit an all-time high of $19.61 billion.

What does LRS mean?

Liberalized Remittance Scheme or LRS, is a facility introduced by the RBI to enable a quicker, easier and simpler process regarding outward remittances from India. As per the scheme, an Indian resident can transfer up to US $ 2, 50,000 outside India in a given financial year.

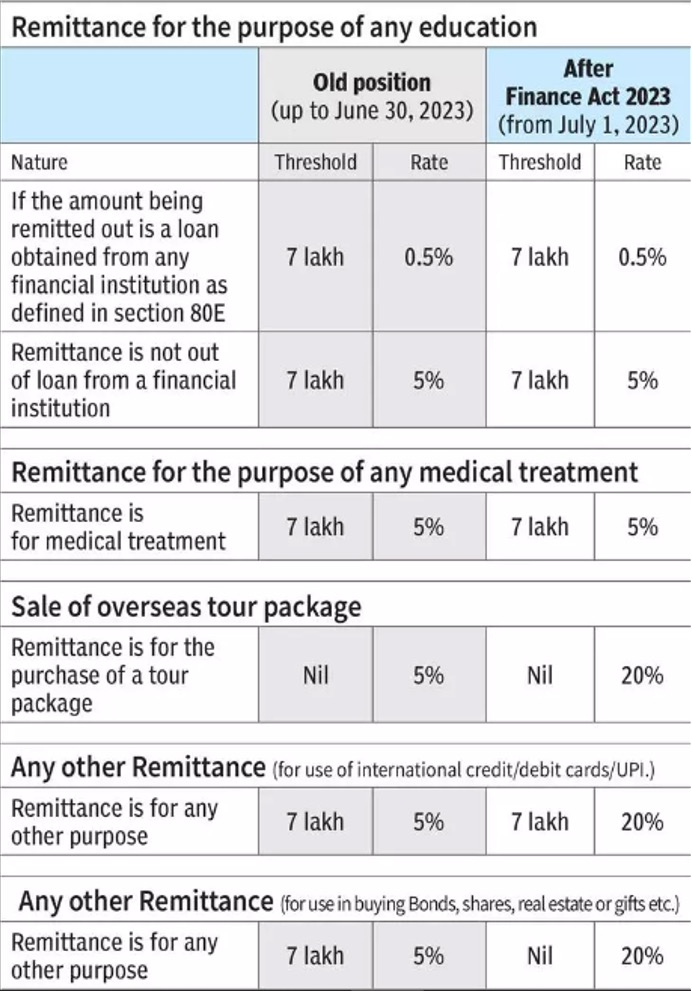

Prior to the Union Budget 2023, TCS, under the LRS scheme was 5% for funds exceeding ₹7 lakh. With the new rule this rate will increase to 20% without any threshold limit, with effect from 1st July 2023, which has to be paid by everyone except for those involved in education or medical treatment. With changes in the Foreign Exchange Management (Current Account Transaction) Rule, the government in consultation with the RBI has bought credit card transactions under the LRS scheme limit of $2, 50,000. With TCS provisions being applied to all LRS remittances, it means that TCS of 20% will be applied to credit card transactions as well. The government has clarified that any payment by an individual using international debit or credit card up to ₹7 lakh in a financial year will be excluded from the LRS limit and hence, from TCS. Unlike Credit cards, Debit cards were already under the LRS limit and this exclusion of credit cards, it is believed, has led to individuals exceeding the limit. It has been noted that outward LRS remittances have increased to $27.1 billion in the last two years and the government believes that this is an underestimation due to the exemption of credit cards from the LRS limits. “People who want to spend money overseas will need to be mindful of the overall limit of $2,50,000 under LRS. One will have to plan the use of the limit between direct remittances and credit card usage for foreign currency transactions,” says Girish Vanvari, founder of Transaction Square.

With the new rule in effect citizens have to be aware of the LRS limit of $2,50,000 and the associated tax implication. According to Russell Gaitonde, Partner with Deloitte India, “Indians have to remember to pay TCS when using international credit cards for transactions as well as claiming credit for tax payment when filing annual income tax return in India.” He goes on to explain that rule change will also apply to forex transactions, say for online purchasing from a foreign company while sitting in India through international credit card. If foreign companies offer Indian customers products in INR and they use international credit cards to pay INR, then no TCS will be levied as it will not be a part of LRS. However, if the product is offered in any foreign currency and the customer pays in INR, then that will be converted into the foreign currency and will be remitted outward to the company. Thus, applicable under LRS and for TCS.

According to Neeraj Agarwala, Partner, Nangia Anderson India, introduction of the new rule may prove to be a major challenge for banks as the banks issuing credit cards will be responsible for the collection of TCS. A strong IT department will be needed to be able to keep up with the data, while ensuring proper management and compliance. EY National Tax Leader, Sameer Gupta pointed out the issue with business visits and its associated costs and personal expenditure. In his view, “Operational mechanics of distinguishing between official and personal expenditure on international credit/debit cards need clarity.” This view was supported by Sunil Badala, partner and head of BFSI taxation at KPMG. According to international tax expert, TP Ostwal, this new rule proves to be more burdensome for banks while impacting all stratum of consumers. In his opinion, the RBI should offer more clarity on the matter and a 5% TCS seemed to be the most rational way out. Those who misuse this rule should be punished separately instead of levying a heavy burden on everyone as a whole.

With this new rule coming into effect from 1st July 2023, the exact impact on transactions and the economy cannot be judged beforehand. There is opposition coming from tax executives and organizations but the real impact can only be guessed after its implementation to see who actually better analyzed the aftermath of this policy.

Written by Iesha Tandon

Edited by Aryaa Dubey