The rise of India’s middle class, particularly in urban areas, has been a significant driver of economic growth and societal change. According to a survey conducted by the People Research on India’s Consumer Economy (PRICE), India’s 63 biggest cities are now home to more than a quarter of its middle class. These cities generate 29% of the country’s disposable income, driving demand for goods and services and fueling an economic boom.

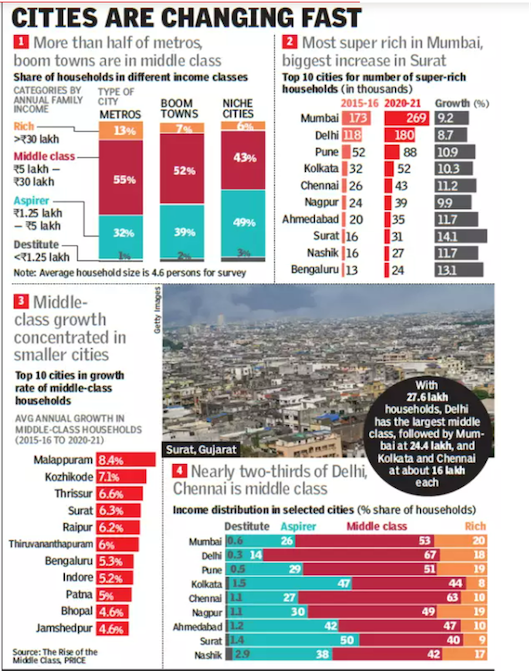

The survey categorizes households into various income groups, revealing that households with an annual income between Rs 5 lakh-Rs 30 lakh ($6,700-$40,000) constitute the middle class. In metros, nearly 55% of households were classified as middle class, with 13% categorized as rich and 32% as aspirers. Furthermore, the survey shows that boomtowns and niche cities also have significant middle-class populations, accounting for over 50% of households in boomtowns and over 40% in niche cities.

The distribution of wealth within these cities is striking. Surat, a textile city in Gujarat, recorded the sharpest growth in the number of super-rich households between 2015-16 and 2020-21. Mumbai had 2.7 lakh super-rich households compared to 1.8 lakh in Delhi, highlighting the concentration of wealth in certain urban centers.

However, defining the middle class in India involves more than just income thresholds. It encompasses broader socio-economic indicators, including education, occupation, social status, and consumption behavior. While income is crucial, lifestyle and access to amenities also play significant roles in defining middle-class status.

The distinction between middle income and middle class is noteworthy. While the former pertains to a specific income range, the latter encompasses a broader socio-economic identity. Thus, discussions about the middle class in India often involve a nuanced understanding of both income levels and social indicators.

The rapid urbanization observed in India’s cities further accentuates the importance of understanding the middle class’s dynamics. The nine metros, including Mumbai, Delhi, Kolkata, Bengaluru, Chennai, Hyderabad, Surat, Ahmedabad, and Pune, serve as India’s consumption centers. The 16 boomtowns and 38 niche cities are emerging as significant markets with their unique characteristics and growth trajectories. This is exactly why it is so important to delve deeper into the emerging trends of these cities to understand the broader consumerism preferences in India.

Why is there a divide?

The analysis of the Monthly Per Capita Consumer Expenditure (MPCE) data and the RBI Consumer Survey underscores the stark income disparities within the so-called “middle class” of India. Despite being commonly grouped under the umbrella of the middle class, individuals within this category exhibit vastly different economic realities and consumption patterns.

The MPCE data reveals a significant divergence in spending power among households, with the gap between rural and urban expenditure levels widening over the years. For instance, from 2012-13 to 2022-23, while the Monthly Per Capita Consumer Expenditure (MPCE) continued to rise steadily, real wages stagnated for most income households. Additionally, the widening gap between rural and urban MPCE levels further highlights the deepening urban-rural economic divide. The gap between the top two income segments and the rest of the population is stark, with the top 4 percent of consumers having seven times the income of the other 96 percent.

Moreover, perceptions regarding economic conditions and future prospects vary significantly across income brackets. According to the RBI Consumer Survey, lower-income groups express more pessimism and uncertainty, with a concerning trend emerging among individuals earning less than Rs 5,000, where the majority (62%) perceive a monthly worsening economic situation. In contrast, higher-income earners exhibit greater optimism and confidence, with the highest income bracket of Rs 1 lakh and above demonstrating the most positive perception, with 55% reporting an improvement monthly.

The K-shaped economic recovery observed post-COVID further accentuates this disparity, with certain segments of the population benefiting disproportionately from economic growth while others struggle to make ends meet. The data indicates a widening gap in perceptions, expectations, and economic realities across income brackets, challenging the homogeneous portrayal of the middle class.

Urban exclusion in India’s cities highlights the stark disparities between the affluent and the marginalized, particularly within the context of the urban middle class. As India’s cities experience rapid urbanization and economic growth, the concentration of wealth among a few rich individuals in posh neighborhoods stands in stark contrast to the poverty and deprivation prevalent in low-income areas and slums. The urban rich enjoy a lifestyle characterized by luxury amenities and security measures, while the urban poor struggle with inadequate housing, lack of basic amenities, and limited access to education and healthcare. This segregation leads to a widening urban-rural economic gap, perpetuated by factors such as unequal access to employment opportunities, poor infrastructure, and inefficient government policies. Despite efforts to address urban poverty through schemes like the Jawaharlal Nehru National Urban Renewal Mission (JNNURM) and the National Urban Health Mission (NUHM), the magnitude of inequality remains a significant challenge, requiring comprehensive interventions to mitigate urban exclusion and promote inclusive development.

Therefore, while the term “middle class” may imply a certain level of economic stability and security, the reality is far more complex. Within this category lie individuals with vastly different economic trajectories – from affluent consumers enjoying luxury vacations to those grappling with job insecurity and financial instability. As such, the categorization of the middle class masks the wide income gap and economic disparities prevalent within this segment of society.

Spending trends: Is the Indian Young Middle Class becoming the “prodigal son”?

India’s young middle class is navigating a delicate balance between aspirational consumption and financial prudence, with spending trends revealing a nuanced shift towards borrowing to fuel lifestyles. Despite economic challenges, such as high inflation and slowing growth, a staggering 84% of Indian millennials own smartphones, indicating their eagerness to delve into the credit sector. This demographic comprises two-thirds of the country’s population, underscoring its significant influence on consumer behavior.

Initiatives like Pay It Forward aim to address the financial literacy gap among young professionals. However, despite access to resources like MoneyControl and apps like Mvelopes and Wally, many millennials struggle with impulsive spending habits driven by peer pressure and social media influence. This trend is reflected in statistics, with 70% of millennials in India admitting to being influenced by social media in their purchase decisions.

Urban unemployment among the youth in India presents a significant challenge, with the latest data revealing an unemployment rate of 17.3% for those aged 15-29, nearly three times higher than the overall rate of 6.6%. This disparity underscores the severity of the crisis, exacerbated by the limited job opportunities available in both the government and private sectors.

One of the primary drivers pushing urban youth towards borrowing and debt is the scarcity of suitable employment opportunities commensurate with their qualifications and aspirations. Despite economic growth, job creation has not kept pace, resulting in a mismatch between the skills possessed by young individuals and the demands of the labor market. As a consequence, many find themselves underemployed or working in precarious, low-paying jobs, leading to financial instability.

Additionally, the allure of urban lifestyles portrayed through social media and peer pressure further exacerbates the situation. Young individuals often feel compelled to maintain appearances and keep up with their peers, leading to increased spending on consumer goods, travel, and experiences beyond their means. This desire to fulfill societal expectations and achieve a certain standard of living drives many to resort to borrowing to finance their lifestyle, contributing to the growing debt burden among India’s youth.

Moreover, the rise of the gig economy, characterized by short-term contracts and freelance work, adds another layer of financial uncertainty for urban youth. While providing flexibility, gig work often lacks stability and benefits, leaving individuals vulnerable to income fluctuations and unable to build financial resilience.

The lack of financial literacy and awareness among young urbanites further compounds the problem. Without proper understanding of concepts like interest rates, credit scores, and debt management, many inadvertently fall into debt traps, relying on high-interest loans and credit cards to fund their lifestyle. This cycle of debt can quickly spiral out of control, leading to long-term financial repercussions and hindering opportunities for economic advancement.

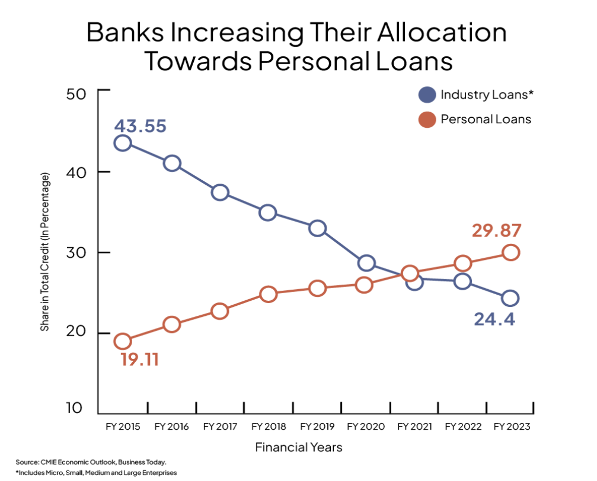

The reliance on credit has become a cornerstone of economic activity, particularly among the low- to middle-income segments. Retail loans, including unsecured loans, have seen significant growth, with data indicating that unsecured loans now constitute 30% of total assets under management for large Non-Banking Financial Companies (NBFCs). This surge in borrowing-driven consumption has contributed to India’s resilient consumption landscape, with credit card outstanding amounts reaching Rs 2.10 lakh crore in March 2023, marking a 28% increase from the previous year.

Individuals leverage credit and no-cost EMI schemes to indulge in luxury without immediate financial strain. This behavior underscores the allure of flexible payment options and the desire to maintain curated lifestyles. However, concerns have been raised about the sustainability of this borrowing spree. Rising delinquency rates for credit cards and defaults in credit card payments signal potential financial distress among borrowers. Financial regulators, including the Reserve Bank of India (RBI), have issued warnings to lenders regarding the risks associated with high credit growth in the retail segment, emphasizing the need for responsible lending practices.

Conclusion and Future Projections:

India’s middle class, particularly the urban upper-middle-income segment, has witnessed remarkable growth over the past three decades, fueled by a steady rise in GDP per capita. This growth has led to significant expansion across consumer categories, with consumption expected to escalate further as per capita income surpasses $2,000. The future consumer landscape will be characterized by diversity, with affluent urban consumers driving premiumization, while the aspirational middle class presents opportunities for new-age products and business models. Despite potential challenges such as economic cycles and evolving trends, India’s consumption journey is poised for profound transformation by 2047, with consumer spending projected to soar three to four times its current level. This reflects a significant milestone in India’s economic journey, highlighting the transformative impact of its middle class on the broader economy.

Written by Annesha Sengupta

Edited by Aliya Khatri