The US real estate market is currently in a state of flux, with several factors contributing to both challenges and opportunities for buyers and sellers alike. As the US real estate market once again takes centre stage, a question looms large: Is it a repeat of 2008? The US real estate market is a vast and dynamic sector that plays a pivotal role in the nation’s economy, representing a significant portion of its GDP and impacting the financial well-being of millions, both domestically and globally. There are some similarities between the two markets. In both cases, we are seeing rising mortgage rates, low housing inventory, and high home prices.

However, there are some differences. One of the biggest differences is the lending standards. In 2008, lenders were making subprime mortgages to borrowers with poor credit or low-down payments. This led to a wave of foreclosures when borrowers were unable to afford their mortgages. Today, lending standards are much stricter, making it less likely that borrowers will default on their mortgages. Another key difference is the economy. The economy was in a recession in 2008, with high unemployment and low wages. The economy is much stronger today, with low unemployment and rising wages. This means that borrowers are more likely to be able to afford their mortgages today than they were in 2008.

Overall, while there are some similarities between the current housing market and the 2008 housing crisis, there are also some key differences. It is unlikely that we will see a repeat of the 2008 crisis, but it is important to be aware of the risks involved in the housing market.

The US Real Estate Market Crash 2008: A Deep Dive into the Crisis

The US real estate market has long been a key indicator of the country’s economic health. The housing market crash of 2008, also known as the Great Recession, was a catastrophic event that had far-reaching consequences for millions of Americans. In the early 2000s, the US housing market was experiencing unprecedented growth. Home prices were on the rise, with the median sales price of existing homes doubling between 1997 and 2006. By 2006, the nationwide median home price had reached $221,900, up from $120,600 in 2000. A significant contributor to the crisis wasthe widespread issuance of subprime mortgages. These were loans offered to borrowers with poor credit histories or those who could not afford traditional mortgages. In 2006, subprime mortgages constituted roughly 20% of all mortgages issued. Investment banks bundled these subprime mortgages into complex financial products known as mortgage-backed securities (MBS) and sold them to investors. The total value of outstanding MBS in the US was estimated to be approximately $7.1 trillion by 2008.

Another factor that contributed to the crash was the prevalence of adjustable-rate mortgages (ARMs). Many homeowners took out ARMs with low introductory interest rates, which were later adjusted to higher rates. As these rates increased, many homeowners found themselves unable to make their monthly payments, resulting in widespread defaults. In 2007, home prices started to decline, leading to the bursting of the housing bubble. This created a situation where many homeowners owed more on their mortgages than their homes were worth. The Case-Shiller Home Price Index, which tracks housing prices, saw a significant drop in prices starting in 2007, with a peak decline of nearly 27% by early 2009. The housing market collapse led to a wave of foreclosures and mortgage defaults, causing severe stress on banks and financial institutions. Major financial institutions, such as Lehman Brothers, faced insolvency and declared bankruptcy in September 2008. The 2008 financial crisis triggered a severe recession in the US. The unemployment rate peaked at 10% in October 2009

In the aftermath of the housing market crash, significant efforts were made to implement new regulations and increase oversight of the financial sector. The Dodd-Frank Wall Street Reform and Consumer Protection Act signed into law in 2010, aimed to increase transparency and accountability in the financial industry. To avert a complete financial meltdown, the US government implemented various measures, including the Troubled Asset Relief Program (TARP), which provided funds to stabilize financial institutions. The Federal Reserve lowered interest rates and engaged in multiple rounds of quantitative easing to inject liquidity into the financial system. The crisis had global ramifications, with many other countries experiencing economic downturns.

The housing market took several years to recover fully. It was not until around 2012 that housing prices began to stabilize and gradually rise again. The 2008 US real estate market crash was a multifaceted crisis driven by a housing bubble, the proliferation of subprime mortgages, and the complex financial instruments known as mortgage-backed securities. It had profound and lasting effects on the US economy and the global financial system.

The crisis serves as a stark reminder of the perils of speculative bubbles and lax lending practices in the real estate market, and it underscores the importance of robust regulatory measures to safeguard the stability of the financial system.

Is the US Real Estate Market Heading Toward a Repeat of the 2008 Crisis

The US real estate market has been a topic of concern for many homeowners and investors, particularly due to the memory of the 2008 housing crash. The collapse of property values and the surge in foreclosures during that time have left a lasting impact on individuals’ perception of the market. As a result, many Americans fear the possibility of another housing crash shortly. However, it is essential to analyze the current market dynamics and compare them to the conditions that led to the 2008 crisis. We will explore the differences between the present real estate market and the situation over a decade ago to provide a comprehensive understanding of the current landscape.

The Labor Market

One significant distinction between the current real estate market and the conditions preceding the 2008 housing crash is the strength of the labor market. During the Great Recession, the US experienced a staggering loss of 8 million jobs in a single year. However, today’s labor market remains robust, with virtually no job losses of such magnitude. While layoffs have occurred in specific sectors like technology and mortgage industries, they have not resulted in a net job loss. A strong labor market is a positive sign for the real estate market, as it indicates stability and provides individuals with the means to afford homeownership.

Less Risky Loans

Another crucial difference between the two periods is the prevalence of subprime loans. During the 2008 housing bust, subprime loans, which were high-risk mortgages offered to borrowers with low credit scores, played a significant role in the crisis. But in today’s market, these high-risk loans are virtually nonexistent. Lenders have implemented stricter lending standards and regulations to prevent a recurrence of the subprime mortgage crisis. The current real estate market’s overall stability has been strengthened by this shift towards safer lending practices. Currently, the Mortgage rates have been rising steadily over the past year, making it more expensive to buy a home. As of October 5, 2023, the average 30-year fixed-rate mortgage rate is 7.31%, according to Freddie Mac. Compared to a year ago, this is an increase of 3.04%.

Underbuilding and Inventory Shortages

A key factor that distinguishes the present real estate market from the conditions preceding the 2008 crash is the underbuilding and inventory shortages. Before the 2008 crisis, new-home construction was occurring at a rate of 7.65 million units annually. Currently, new-home construction stands at approximately 4.6 million units per year. The number of homes for sale remains low, which is driving up prices. In August 2023, there were 1.53 million homes for sale in the US, down 17.5% from a year ago, according to the National Association of Realtors (NAR). This significant reduction in construction has resulted in a massive housing shortage. Over the past decade, there has been underproduction in the housing market, exacerbating the supply-demand imbalance. The scarcity of available homes has contributed to the appreciation of home prices, making a price crash less likely due to the limited supply.

Delinquency and Foreclosure Rates

Mortgage delinquency and foreclosure rates are essential indicators of the health of the real estate market. In the previous housing bust, approximately 10% of all mortgage borrowers were delinquent on their loans. However, today’s mortgage delinquency rate stands at 3.6%, which is significantly lower than during the 2008 crisis. Additionally, the foreclosure rate is also remarkably low, sitting at 0.6%. These historically low delinquency and foreclosure rates reflect the overall stability of the current real estate market.

Price Stability and Inventory Shortages

Although there may be a slowdown in certain regions for home sales, prices are still robust and are rising. As of October, home prices were up nearly 6% compared to the previous year. This price appreciation can be attributed to the ongoing inventory shortages. The limited supply of homes on the market has created a competitive environment, driving up prices. The lack of inventory reduces the likelihood of a price crash, as demand continues to outpace supply. The rental market also played a vital role in the real estate landscape, with millions of Americans opting for renting over homeownership. The national average monthly rent for a one-bedroom apartment was approximately $1,200, while a two-bedroom apartment commanded an average of $1,400 per month. These figures brought to light the challenges associated with affordability and diversity that exist in the rental market in various geographical areas.

The Role of Supply and Demand

First and foremost, the market exhibited a consistent upward trajectory in property values, with the median home price reaching approximately $350,000 in 2020. This steady price appreciation was influenced by factors such as population growth, low interest rates, and a limited supply of housing in many desirable areas, all of which contributed to robust demand. The interplay between supply and demand is crucial in understanding the current real estate market’s resilience. The shortage of available homes, coupled with strong demand, has created a favorable environment for sellers. Buyers, on the other hand, face challenges due to limited options and rising prices. This supply-demand imbalance contributes to the stability of the market, as it prevents a significant decline in prices.

Home Prices and Affordability

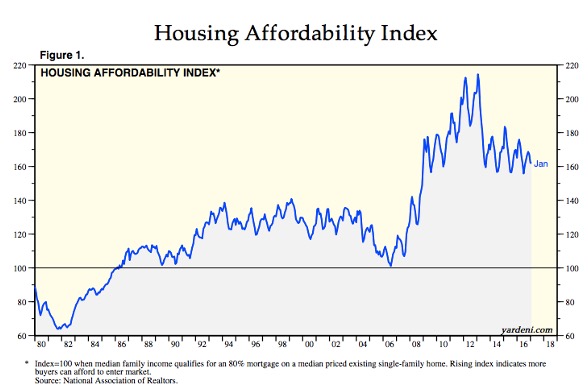

One key indicator of the health of the real estate market is home prices. In recent years, home prices have been steadily increasing, with some areas experiencing rapid appreciation. However, it is crucial to assess affordability alongside these price increases. The median home price in the US reached $420,284 in August 2023, up 2.9% from a year ago, according to NAR. This is making it difficult for first-time buyers and other budget-conscious buyers to afford a home. When wages remain stagnant and home prices rise, it may become more challenging for prospective buyers to enter the market, which could cause demand to decline.

Economic Factors

Various economic factors differentiate the present real estate market from the conditions leading up to the 2008 crash. Interest rates, for instance, play a crucial role in the affordability of housing. In the years preceding the 2008 crisis, interest rates were relatively low, prompting a surge in demand for housing. However, the current market is characterized by higher interest rates, making it less susceptible to speculative buying and price bubbles. The Federal Reserve’s monetary policies also contribute to the stability of the market, as they are designed to mitigate risks and maintain a balanced economy.

Opportunities for growth

Some experts believe that the housing market is headed for a correction, which could lead to lower home prices in the future. However, it is important to note that this is just a prediction, and there is no guarantee that home prices will fall. Buyers may be able to negotiate better prices with sellers as the housing market cools. This could mean getting a better price on a home or having more options to choose from. Homeowners who are looking to sell their homes may be able to get a good price, given the current high demand for homes. However, it is important to work with a qualified real estate agent to price your home correctly and market it effectively. The US real estate market is currently in a transition period. Buyers and sellers need to weigh the challenges and opportunities carefully before making any decisions.

Overall, while some factors may resemble those leading up to the housing market crash of 2008, it is essential to remember that every market cycle is unique. It is essential to take into account the regulatory improvements and enhanced oversight put in place since the crisis, even though there may be certain areas of concern, such as rising property prices and loosening lending standards.

These measures aim to prevent a repeat of the same circumstances that led to the 2008 crash. The current US real estate market exhibits significant differences compared to the conditions over a decade ago. The strength of the labor market, the absence of risky loans, underbuilding and inventory shortages, low delinquency and foreclosure rates, price stability, and economic factors all contribute to the market’s overall resilience. The regulatory measures and reforms implemented following the 2008 crisis have also played a crucial role in enhancing the market’s stability. While no market is entirely immune to risks, the present real estate market is fundamentally different from the conditions that led to the previous housing crash, providing reassurance to homeowners and investors alike.

In recent years, technological advancements and the proliferation of online platforms have also begun to reshape the real estate market. The rise of real estate tech startups and online marketplaces simplified property searches, making it easier for buyers and renters to find suitable properties. Additionally, the COVID-19 pandemic has prompted a shift in real estate preferences, with increased demand for larger homes, suburban properties, and homes with dedicated workspaces.

Written by – Anshika Gupta

Edited by – Saba Godiwala