By Adityapal Singh Jaggi

“Will they, won’t they?” That is what is going on in the minds of investors and other market participants. Fed hiked their benchmark rates last year in December after nearly a decade of zero interest rates. At the start of the year the Fed had warned the market to expect four hikes but that warning couldn’t materialise due to different political upheavals, mainly BREXIT.

With the incoming President Donald Trump looking to use fiscal stimulus including tax cuts and spending on infrastructure, the Fed is looking to increase the benchmark rates.

The Central Bank has adopted an accommodative monetary policy for nearly a decade now, and it has failed to match its expectation regarding inflation and growth. Mr. El Erian has rightly told in an interview with Bloomberg that the “Fed won’t be the markets’ best friend forever.”

U.S. consumers’ expectations for inflation between five and 10 years ahead bounced to 2.7 percent this month, according to preliminary results of a University of Michigan survey released that were mostly collected before the Nov. 8 election. They fell in October to 2.4 percent, a level that marked the lowest in 37 years of data.

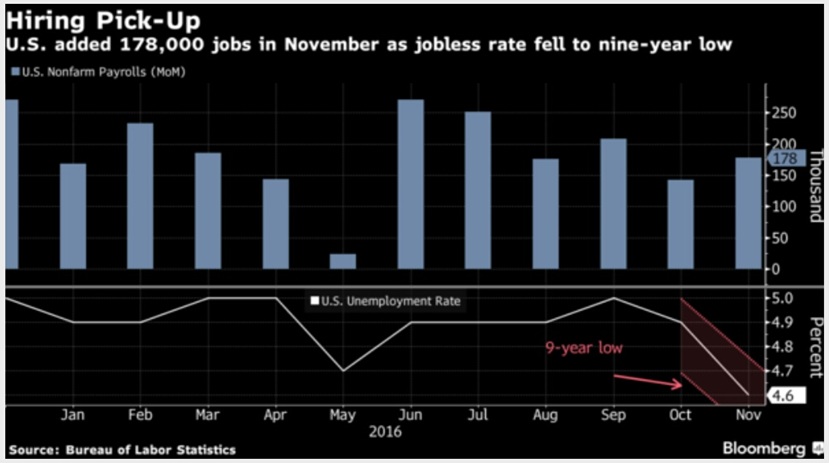

Janet Yellen, Chairperson of Federal Reserve Bank, has said that she wants to run a heated up economy with tight labour force. Well, that is coming true with the election of Donald Trump as President and the November Jobs (non-farm payrolls) data coming at 178,000 v/s expectation of 180,000, missing the target marginally. With this report the Unemployment has fallen to a 9-year low of 4.6%. But there is a catch to this: the labour-force that is actively looking for jobs counts as unemployed; labour force dropouts don’t.

The 10-year treasury bonds are giving a yield of 2.3%. The Fed should be worried about not falling behind the curve.

The case now stands at wage growth which will give us an idea of inflation. The inflation adjusted wage growth, which is the real wage, has not seen any growth in nine years. Yellen has advocated for productivity umpteen numbers of times.

Earlier, Donald Trump was against the Federal Reserve, and now that he has become the President, the question that comes to our mind is regarding central bank’s independence, for which Janet Yellen strongly advocates.

For the first time the market participants and the Fed governors are in sync, as both are expecting the short-term rates to be hiked.

Minutes from the November meeting showed that there will be a rate hike relatively soon if the data received was according to their expectations.

The GDP also expanded, at inflation and seasonally adjusted annual rate of 3.4% in the third quarter, thus marking the strongest growth in 2 years.

Inflation has reached 2%, but not according to the Fed’s gauge of overall inflation, which still shows 1.4% and the jobs market is also looking healthy thus propelling the economy towards its target of achieving full employment.

The Federal Reserve following a low interest rate has also created weakness and asset bubbles in the economy other than being a disaster for savers, money funds, and pension funds which has pushed the funds to hunt for yield in emerging markets.

With the prospect of interest rates rising, capital has travelled from emerging economies back to Wall Street. This has also further strengthened the might of the dollar.

The 30 day Federal Fund Futures are showing a probability of 95% in interest rates rising. Many market participants are in the mindset that the Fed is already lagging behind the curve.

The important thing will be what happens after the meeting. What will Janet Yellen say about the economy, growth-rate, unemployment, inflation as well as the road map of future hikes? Even a slight misstep in using the right words can make the markets tumble down, especially the emerging markets.

Furthermore, the Fed is the only central bank in the developed world looking to raise interest rates.

Many economists are suggesting that the Fed should wait and see if Trump’s policy creates huge deficits in the budget and then react to it. But after the Great Financial Crisis in 2008, the policies of the Federal Reserve have shifted from being reactive in nature to proactive. But being proactive is also not good, as it can stop the growing economy in its tracks.

Last time when they raised interest rates, Nifty 50 and other major indexes had become range-bound for 1-3 months before December 2015. There will be a tumultuous fall if Yellen in post-meeting press conference says that “3-4 hikes can be expected in the coming year.” Already there has been an outflow of FPIs (FIIs).

This month’s Federal Open Market committee is scheduled to meet on 13-14 December in which they are poised to raise the benchmark rates.