Wells Fargo secured the third position among the top 15 biggest banks in the United States in 2023 and has consistently been in the list of top 5 banks over the years. Considered the biggest auto-lender in the United States, with over US$ 1.875 trillion in assets, its continued presence in the top five banks highlights its enduring prominence in the financial sector.

History

Established in 1852 during the California Gold Rush, Wells Fargo’s roots trace back to the founding partnership of Henry Wells and William George Fargo, former employees of the American Express Company. Initially focusing on banking and express services, the company played a pivotal role in acquiring, selling, and transporting gold dust, bullion, and species from the West Coast to the East Coast.

Over the years, Wells Fargo evolved into a major stagecoach business, gaining a national reputation for its agents’ daring and professionalism. While stagecoaches waned in popularity after the completion of the transcontinental railroad in 1869, Wells Fargo’s coaches continued to serve areas without railroads well into the early twentieth century.

In 1998, Wells Fargo & Company took its current form through a merger with Minneapolis-based Norwest Corporation. The amalgamated business retained the Wells Fargo name, moved its headquarters to San Francisco, and became one of the “Big Four” banks in the United States. Throughout the 20th Century, Wells Fargo formalized its banking services, establishing itself as a leading commercial bank. The transformative acquisition of Wachovia in 2008 propelled Wells Fargo into a coast-to-coast banking giant, expanding its presence across the US and diversifying its service offerings through various acquisitions.

Business Model

Investing and Wealth Management:

Client Focus:

Wells Fargo’s Investing and Wealth Management segment is dedicated to serving business clients and high-net-worth individuals (HNWIs). The focus here extends beyond basic banking services, delving into comprehensive wealth management solutions, investment products, and retirement planning. This segment recognizes the unique financial requirements of its clientele and aims to provide tailored services to address their intricate financial needs.

Service Offerings:

Within this segment, Wells Fargo offers an array of services, including financial planning, credit facilities, and private banking. Clients can choose between automated self-directed trading or opt for a more personalized experience with a dedicated financial professional. The emphasis is not only on financial transactions but also on providing strategic advice and solutions that align with the long-term goals of businesses and high-net-worth individuals.

Comprehensive Approach:

Wells Fargo’s wealth management division takes a holistic approach to managing clients’ assets. It provides team-based management solutions, ensuring that a collaborative effort is employed to optimize investment portfolios. Alternatively, clients can opt for a one-on-one approach, benefiting from the expertise of a dedicated financial professional who guides them through the complexities of wealth management.

Financial Overview 2023:

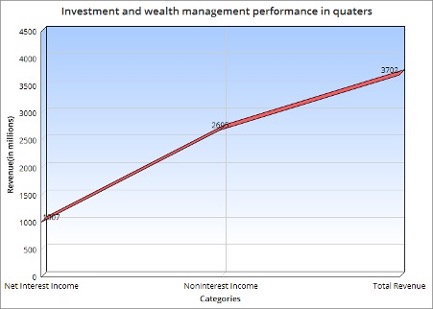

In the third quarter of 2023, the Wealth and Investment Management segment demonstrated resilient revenue generation. Despite a 7% decrease in net interest income, attributed to lower deposit balances and loan volumes, the segment experienced a noteworthy 5% increase in noninterest income. This rise was fueled by higher asset-based fees, driven by the appreciation in market valuations. The total revenue for the quarter reached $3.7 billion, marking a modest 1% increase compared to the same period in 2022. This performance reflects the segment’s ability to navigate challenges, capitalize on market opportunities, and enhance its fee-based income streams.

Wholesale Banking:

Business Clientele:

Wells Fargo’s Wholesale Banking division is designed to cater to the financial needs of both U.S.-based and global businesses. This segment encompasses a broad spectrum of services, with 13 different business lines.

Diverse Business Lines:

The 13 business lines under Wholesale Banking cover a wide range of services, including business banking, corporate banking, commercial real estate, insurance, and credit risk management.

Beyond Traditional Banking:

Wholesale Banking at Wells Fargo goes beyond the conventional scope of banking services. It includes specialized offerings such as equipment financing, enabling businesses to make significant investments in assets like mining equipment. Whether it’s crop insurance, commercial real estate financing, or energy-syndicated loans, Wells Fargo’s Wholesale Banking division is equipped to handle a myriad of financial needs.

Global Presence:

What sets Wholesale Banking apart is its global reach. With offices in 42 states and a substantial international presence from Santiago to Seoul, Calgary to Cairo, and Sydney to St. Helier, Wells Fargo caters to the financial requirements of multinational corporations. To be considered a Wells Fargo wholesale customer, businesses need to boast annual revenues of at least $5 million, underlining the focus on serving entities with significant financial operations.

Revenue Generation:

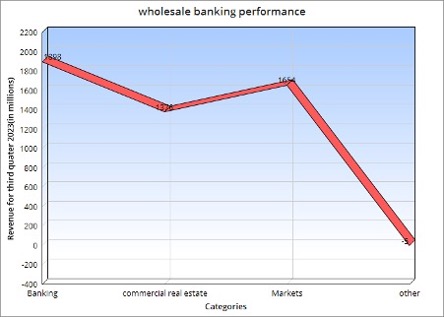

The financial performance of wholesale banking for the third quarter of 2023 showcased notable growth across key segments. Total revenue reached $4.92 billion, marking a 21% increase from the same period in 2022. Banking saw a 20% rise, propelled by elevated lending revenue, robust treasury management results, and increased investment banking activity. Commercial Real Estate revenue increased by 14%, driven by higher interest rates and increased revenue in low-income housing. Markets experienced a remarkable 33% surge, attributed to gains in structured products, equities, credit products, and foreign exchange. Noninterest expenses rose by 15%, reflecting increased operating costs and personnel expenses.

Commercial Banking:

Everyday Banking Needs:

Commercial Banking is the facet of Wells Fargo that directly engages with retail and small business clients, addressing their everyday banking needs. This segment is where most individuals interact with Wells Fargo for routine financial services, including checking and savings accounts, loans, mortgages, and small investment products like certificates of deposit (CDs).

Beyond Basic Banking:

While Commercial Banking serves as a hub for basic financial services, it encompasses much more than typical retail banking. According to Wells Fargo, the community banking segment includes a wealth of services, offering a broad range of financial products and services that go beyond the traditional notion of personal banking.

Multifaceted Services:

Commercial Banking provides a multitude of services, catering to the financial needs of individuals and small businesses. The offerings include checking and savings accounts, credit cards, loans, and other financial products. This segment plays a vital role in Wells Fargo’s broader strategy, as it forms the primary point of contact for a vast customer base.

Financial Overview 2023:

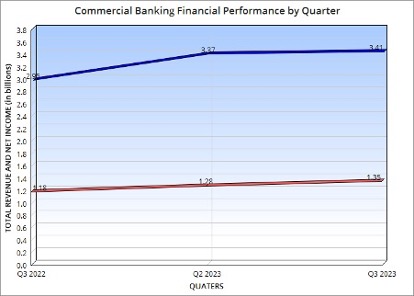

Commercial Banking’s third-quarter 2023 revenue reached $3.41 billion, marking a 1% QoQ and a significant 15% YoY increase. Middle Market Banking led the surge with a 23% rise attributed to higher interest rates and increased loan balances, partially offset by lower deposit balances. Asset-Based Lending and Leasing contributed with a 3% increase, driven by higher loan balances and increased revenue from renewable energy investments. Net income for the quarter amounted to $1.35 billion, reflecting a 6% QoQ and a 15% YoY growth. Despite challenges like a $52 million provision for credit losses and $1.54 billion in noninterest expenses, Commercial Banking displayed positive performance.

Scandals:

Wells Fargo faced a severe setback when the Federal Reserve put a limit on how much money and assets it could have – around $1.95 trillion. This action was taken due to the bank’s involvement in a series of problems that harmed its reputation. One major issue was the creation of fake accounts and credit cards by employees to meet sales targets. The bank initially denied this in 2013 but admitted to it in 2016, revealing over 3.5 million unauthorized accounts. This led to the repayment of fees, firing of 5,300 employees, and the CEO resigning. Wells Fargo also faced hefty fines, paying over $1.5 billion to authorities and $620 million to customers and shareholders.

The bank’s troubles extended to mistreating customers with auto loans and mortgages, resulting in a $1 billion fine. Another incident involved supporting expensive debt products, leading to a settlement of $1.1 million in repayments and a $4 million penalty. In 2018, the bank faced a $2 billion penalty for misrepresenting mortgage loans. In 2022, the Consumer Financial Protection Bureau imposed a $1.7 billion fine for unfair practices related to consumer loans. These scandals eroded trust and ethics, leading to government intervention and financial consequences. The Federal Reserve’s asset cap serves as a tangible punishment, highlighting the need for significant changes to restore the bank’s credibility in the financial world.

Written by – Vaishnavi Sahu

Edited by – Kushi Mayur