“Why would anyone investing in stock markets fear to invest money in a company which is debt ridden? Simply for the fact that when the next crisis comes, that company might be wiped out. Similarly, for countries, for international investors, the debt is going to show up in the sovereign credit ratings.”

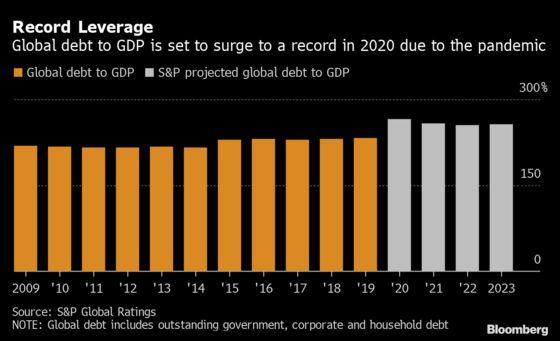

As the world reels from the shock of coronavirus, collapsing currencies, export earnings, and tourism revenues threaten to push the emerging markets towards a debt crisis like the ones that battered them in the 1990s. The collapse in output, spike in capital outflows and plunge in commodity prices have triggered balance sheet problems. Much of the emerging world has witnessed a double-digit contraction in GDP in the first 3 quarters of 2020. As global interest rates went down, investors’ risk appetite increased. New borrowing became an escape from debt default. According to Moody’s estimates, the debt to GDP ratio in the 19 biggest emerging markets has risen by an average of 10 percentage points in 2020 alone.

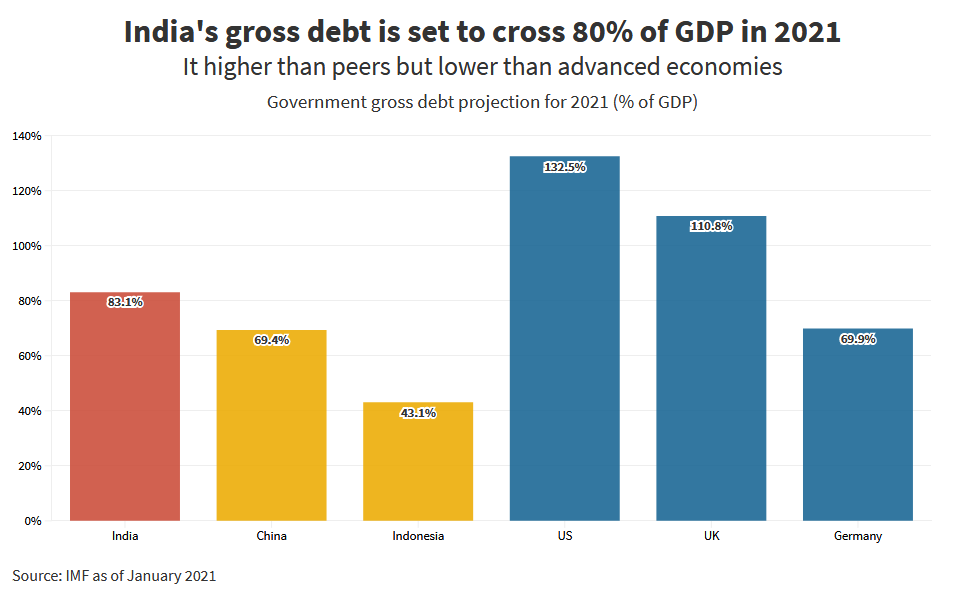

Speaking in context of India, the debt stood at around INR 147 lakh crore against this year’s estimated GDP of INR 194 lakh crore. The government plans to borrow another 12 lakh crore this year. Our debt stands at approximately 75% of GDP, compared to 40-50% in most other emerging economies. Advanced countries like the US and Japan may have even higher debt levels; however, their repayment capacity is also much higher than India.

In the US, they have printed 40% of their initial money stock. Unlike the dollar, emerging economies lack the privilege of capital markets which offer the depth of liquidity and legal certainty. If the Indian government fulfils its debt by printing more money, the value of that money goes down. Central Bank financing of government deficits has been associated with uncontrolled rates of inflation – not only hampering investment but also creating additional challenges for the poor.

Even before the pandemic, many developing countries were struggling to finance their debt. In October 2019, the IMF warned that 34 of 70 frontier economies were at “high risk” of falling into debt distress or were already distressed, up from zero in 2014. Zambia’s gross external financing requirement (i.e. amount required to make interest and debt repayments, and cover the current account deficit) stood at 172% of its foreign exchange reserves. Tunisia, Bahrain and Argentina — which is already in restructuring talks with holders of $83bn of foreign debt — are not far behind, with figures of 158, 153 and 133 percent respectively. These countries have had a high current account deficit for quite some time as it is difficult for them to raise debt domestically owing to the small domestic financial sector.

There are valid reasons for a government to borrow debt and thereby support the broader social and economic objectives. However, debt becomes unsustainable at the point where the government is unable to meet both its expenditure and interest payments. When the government is unable to finance its deficits, it faces a daunting choice – either contract spending and risk a social and political backlash at home, or borrow and spend beyond its constraints resulting in a backlash from international investors. As domestic public debt explodes and firms fear a currency crash, they might stop investing. In this case, the economy will have a tough time growing its way out of debt. A debt crisis ensues and the government must either default or inflate the debt away, both of which entail larger economic and social costs.

Written by Sejal Nathany

Literary Sources:

1. Business Insider

2. Chatham House

3. Financial Times