Financial deregulation can refer to a variety of changes in the law which allow financial institutions more freedom in how they compete. However whether such changes are beneficial or harmful to the economy, as a whole, has been widely debated. There has often been struggle in the past between proponents of regulation and proponents of no government regulation. If we look at the banking history of the US, we can realise that every economic meltdown is followed by tight regulation, which loosens up as the time flows and too much of such loosening then leads to another crisis.

In 1932, the whole of the US had been engulfed by depression, and unemployment had reached a tragic level of 23.6%. People lost faith in the banking system which compelled the Roosevelt government to come up with new banking legislature which would make banks more resilient to economic carnage and help in developing more safety nets. This marked the birth of Glass-Steagall Act, 1933 and Security Exchange Act of 1934.

The government had the forefront task of reinstating the customer confidence and mitigating the bank runs. The Glass-Steagall Act established a system of deposit insurance for consumers with the creation of the Federal Deposit Insurance Corporation (FDIC). The FDIC guaranteed consumer deposits up to a certain level, quieting the widespread fears of bank failures. In addition, the act prohibited banks from being “engaged principally” in non-banking activities, such as the securities or insurance business. Firms were thus forced to choose between becoming a bank engaged in simple lending or an investment bank engaged in securities underwriting and dealing.

The rationale for seeking the separation was the conflict of interest that arose when banks were engaged in both commercial and investment banking, and the tendency of such banks to engage in excessively speculative activity. With intent to prevent rate wars at exorbitant level, Regulation Q was placed restricting interest rate to 5.25% for savings account, 5.75% and 7.75% for time deposits and 0% for checking accounts.

In the late 1970s, inflation caused the market interest rate to rise above the limits mandated by Regulation Q. Investors found other financial products more attractive so the money started going out of the banking system, which in turn urged the government to phase out interest ceilings within 6 years. This was major step towards deregulation which came after 50 years of austerity. Throughout the 1980s and the 1990s there were debates on whether there is need to repeal Glass-Steagall Act, since the stringent laws of the act were making commercial banks less competitive. In 1986 Federal Reserve reinterpreted the restrictions of the act and ruled that commercial banks can derive 5% of revenue from investment banking business. Later, in 1996, the Federal Reserve issued an audacious ruling, allowing bank holding companies to own investment banking operations that accounted for as much as 25 percent of their revenues. The decision rendered Glass-Steagall effectively obsolete. The crumbling walls of Glass-Steagall received a final blow in 1999 when Congress passed the Financial Modernization Act. The act repealed all restrictions against the combination of banking, securities and insurance operations for financial institutions.

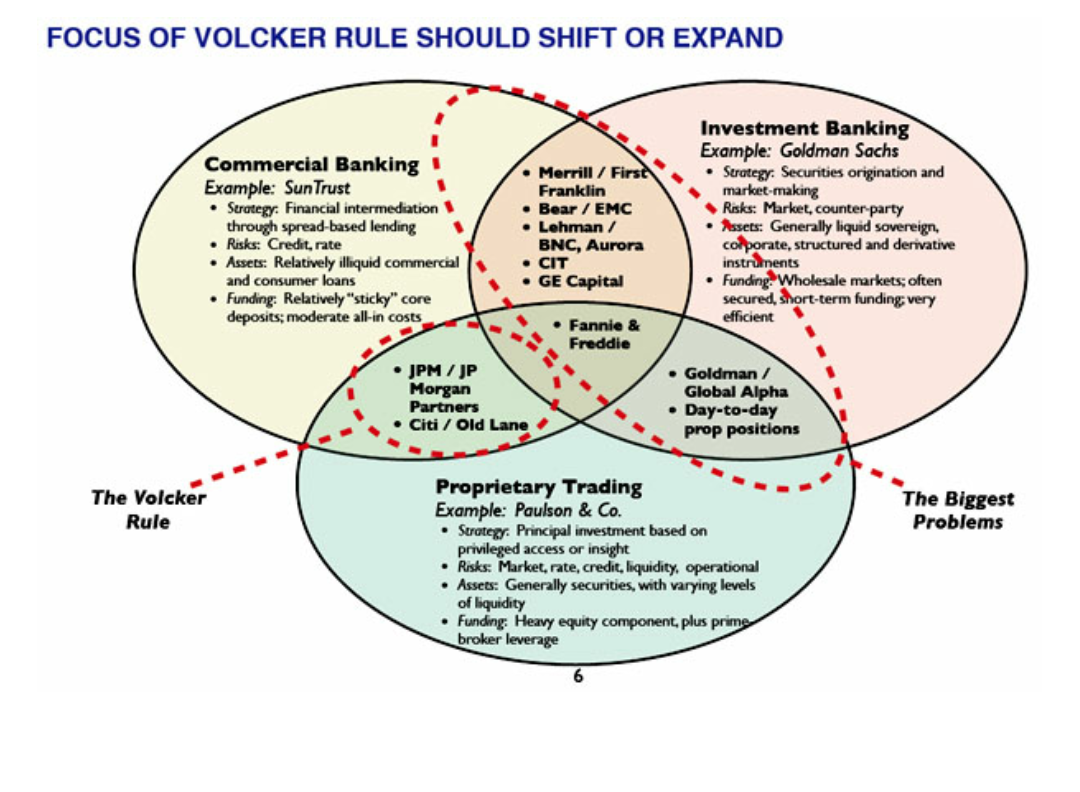

Many economists have contended that repeal of Section 20 and 32 of Glass-Steagall Act has been one of the major causes of financial crises 2007-09. Economics Nobel Prize laureate Joseph Stiglitz, for instance, argued that “when repeal of Glass-Steagall brought investment and commercial banks together, the investment-bank culture came out on top,” and banks which had previously been managed conservatively turned to riskier investments to increase their returns. As a response to financial crisis of 2008, Obama administration passed a massive piece of financial reform legislation in 2010 called the Dodd-Frank Wall Street Reform. The act aims at preventing consumer from risky behaviour, abuse or financial loss of financial institution; to prevent institutions from becoming too big to fail, to end government bailouts funded by taxpayers and to end risky and abusive financial services practices. Many new agencies were created to get propositions of this act implemented effectively. These agencies aimed to protect consumers by preventing predatory mortgage lending and make mortgage, credit card and loan paperwork easier to understand. A key component of Dodd-Frank, the Volcker Rule, restricts the ways banks can invest, limiting speculative trading and eliminating proprietary trading. It prohibits banks from conducting certain investment activities with their own accounts, and limits their ownership in hedge funds and private equity funds.

Five years after the passage of the Dodd-Frank financial law, the causes and effects of the failed economic recovery are apparent throughout the banking system. The Federal Reserve’s stimulus package has inflated bank reserves, but lending has barely increased. Today banks maintain an extraordinary $29 of reserves for every dollar they are required to hold. In the first quarter of 2015 banks actually deposited more money in the Fed ($65.1 billion) than they lent ($52.5 billion). According to the Federal Deposit Insurance Corporation, 1,341 commercial banks have disappeared since 2010. Remarkably, only two new banks have been chartered. By comparison, in the quarter century before the financial crisis, roughly 2,500 new banks were chartered. Even during the Great Depression of the 1930s, an average of 19 new banks a year were chartered. Donald Trump’s has promised to dismantle the Dodd–Frank Wall Street Reform and Consumer Protection Act. Trump has promised to replace the law “with new policies to encourage economic growth and job creation.” However, we should realize that all of us—including the too-big-to-fail banks themselves—can breathe a little easier in this stressful environment, thanks to the Dodd-Frank Act.

Thus we can conclude that stringent regulations are inherent policy of every economy who is trying to recover from turmoil. When the economy recovers and investment climate becomes rosy, the severity of regulations comes down. The same regulations which averted the things from going worse, people find them imperilling their freedom. The loosening of regulations can make financial system vulnerable to another crisis. Deregulation is undoubtedly welcomed but the proportion in which it takes place should essentially be regulated.

By Chintan Matalia

Sources:

- Sherman Matthew, ‘A Short History of Financial Deregulation in the United States’ http://cepr.net/documents/publications/dereg-timeline-2009-07.pdf

- http://www.investopedia.com/terms/d/deregulate.asp

- Pic Source: The Sydney Morning Herald

One of the articles from The Economic Transcript, U.S section (February, 2017, issue).