The “Ouroboros” a Greek symbol of dragon eating its own tail depicting “eternity” ideally symbolises the “perpetual” economic crisis in Greece. A minor country in the grand scheme of things in Europe became a test case for a strategy that could be likened to rolling a snowball uphill. A research paper in January 2015 by University of London explained how the “Euro” is creating hurdles for Greece in coming out of the crisis that started in the aftermath of the financial crisis of 2008.

After the Introduction of Euro in 1999 there was massive capital inflow into countries like Greece and Portugal from France, Germany and other European countries because the per capita income of these countries was 61% of the level of Germany, France and others suggesting the ample potential of growth. Prices and Income increased initially thanks to massive government expenditure but were not accompanied by similar rise in productivity, so the economy became more and more dependent on the Inflow of capital to breathe. Reduction in international capital flow after the 2008 crisis created pressure on Greece to close its external deficit and balance its trade. In order to do this the economy needed to increase its exports of tradable goods and service and reduce imports. For this the competitiveness had to first be restored. Earlier it was done by devaluation of currency but joining Eurozone forfeited them that option because Greece no longer had the sovereignty to decide Euro rates.

Now the only way to restore the competitiveness was to reduce the nominal wages and bring about an improvement in productivity. This can be a very painful and slow process especially in rigid political environments. The massive bailout that ultimately came at the last moment brought with it harsh austerity measures to reform the pension and state tax system through sale of nonperforming assets and reduction in wages.

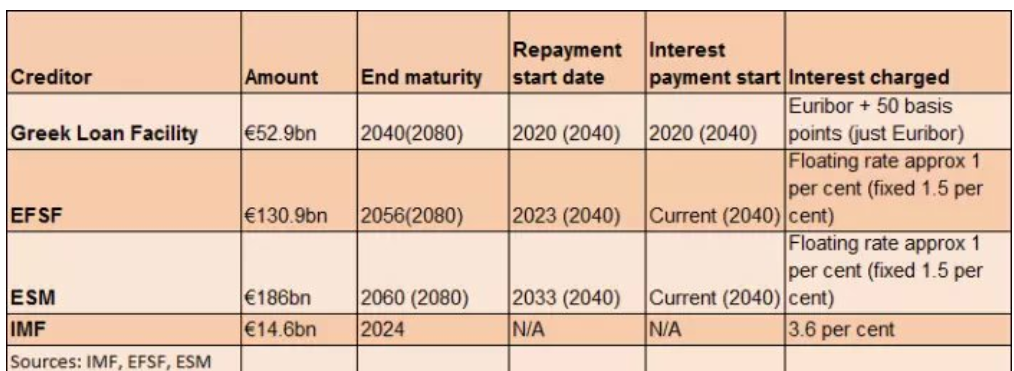

Greek debt has racked up debt equivalent to 180% of its GDP. In total, the Greek government debt pile stands at € 321 Billion. Of this €248 Billion is owed to its official creditors: Its fellow member states (Greek loan facility) and Eurozone’s two rescue funds: The IMF and European Central Bank. These liabilities have accumulated over 6 years as it has received three international bailouts and will keep paying it till 2060. Its Debt to GDP ratio is highest after Japan. According to the newly appointed Finance Minister, who first coined the term ‘fiscal waterboarding’ to describe Greece’s plight, the EU has loaded ‘the largest loan in human history on the weakest of shoulders – the Greek taxpayer’. Bailout proposed can only be used by Greece when it agrees to the creditors’ demand of harsh austerity. Like the second bailout tranche of €1.2 Billion, the third bailout of €86 Billion was agreed upon only when Greece agreed to comply with pension, tax reforms and privatisation.

According to OECD’s Average Annual Hours Actually Worked Per Worker survey a Greek worker spent 2046 hours a year which is 50% more time at work than the average German worker (1,371 Hours). Meanwhile, the earnings of private employees in Greece have declined by 25% and unemployment rate continues to be around 23%. Further, more taxes that came with harsh austerity imposed by “TROIKA” (European Commission (EC), the European Central Bank (ECB) and the International Monetary Fund (IMF) worsen the already reduced Income.

This has led to resentment among the public towards their government for an inefficient public sector and Troika for harsh reforms imposed.

Greek exit from the Eurozone and reintroducing the Greek currency “Drachma” is an revolutionary notion to solve the Greek Crisis. Proponents argue that reintroducing the Drachma would dramatically boost exports and tourism and would potentially render the economy more competitiveness. But it could also prove to be jumping from the frying pan into the fire.

On 29th May 2012 the National Bank Of Greece (not to be confused with the central bank, the Bank Of Greece) warned that:

” An exit from the euro would lead to a significant decline in the living standards of Greek citizens. According to the announcements, per capita income would fall by 55%, the new national currency would depreciate by 65% vis-à-vis the euro, and the recession would deepen to 22%. Furthermore, unemployment would rise from its current 22% to 34% of the work force, and inflation, which was then at 2%, would soar to 30%.”

As a part of its New Policy Of “Economic Easing” ECB (European Central Bank) is buying the government bonds from the European Countries. Since the start of this policy in March 2015 it has bought around €645 Billion in government bonds and is expected to purchase €1500 Billion bonds till March 2017 to lift the European economy out of stagnation. But Greece is being kept out of this policy whereas all other EU countries are highly benefitting from this “silent” Debt Relief.

Table 1 Cumulative purchases of government bonds (end of April 2016)

(million euros)

Source: ECB

ECB gives a technical reason for this exclusion saying that the Greek government bonds do not fulfill the quality criteria for this QE policy. But these technical problems can easily be overcome when the political will exists to do so. This is a highly political decision to punish the country that has misbehaved in the past. At one side “Eurozone” wants Greece to pay its debt but on the other side it imposes harsh austerity reforms neglecting that “Austerity suppresses growth and without growth debt cannot be repaid”.

It is high time this discrimination was stopped and the country struggling under massive debt was treated the same way as others.

By Khusal Gulati

Pic source: Zcomm.org

One of the articles from The Economic Transcript, Europe section (February, 2017, issue).

To get your copy subscribe now.