As newspaper headlines read ‘ Beauty turns into Beast’, the story of Mamaearth’s IPO draws attention on various fronts right from its valuation to recent losses amongst other things. Before we delve into the analysis, let us understand what an IPO is and why it is done in the first place.

What is an IPO?

An Initial Public Offering (IPO) is the way via which a private company transfers some portion of ownership to the general public. The capital raised could be used to pay debt/invest in growth initiatives/allow more liquidity for current stakeholders who can sell all or some of their shares. For companies, IPOs serve as a good means of raising capital while for the general masses, they are a good way to gain ownership in a company.

About the company

Mamaearth is a 6-year-old company that was born out of the sheer need of baby care products in the most unadulterated form. The story traces back to when the founders Varun Alagh and Ghazal Alagh were expecting their first child. As most parents do, they researched about products and found out that most of them had toxins that are harmful for children. It was then that they had a vision in mind. It said, ‘A brand for a parent by a parent’. With the aim of making products which are mum-baby friendly, toxin-free, meet stringent international standards & are basically ultra-awesome, Mamaearth was born. Mamaearth’s journey through the years has been inspiring for many women. With a good intention and resources that are mostly sustainable, Mamaearth aims to inspire a generation along with selling products. As they file the IPO, it would be interesting to see how the exchanges treat the company today and hereafter.

Company Profile ahead of the IPO

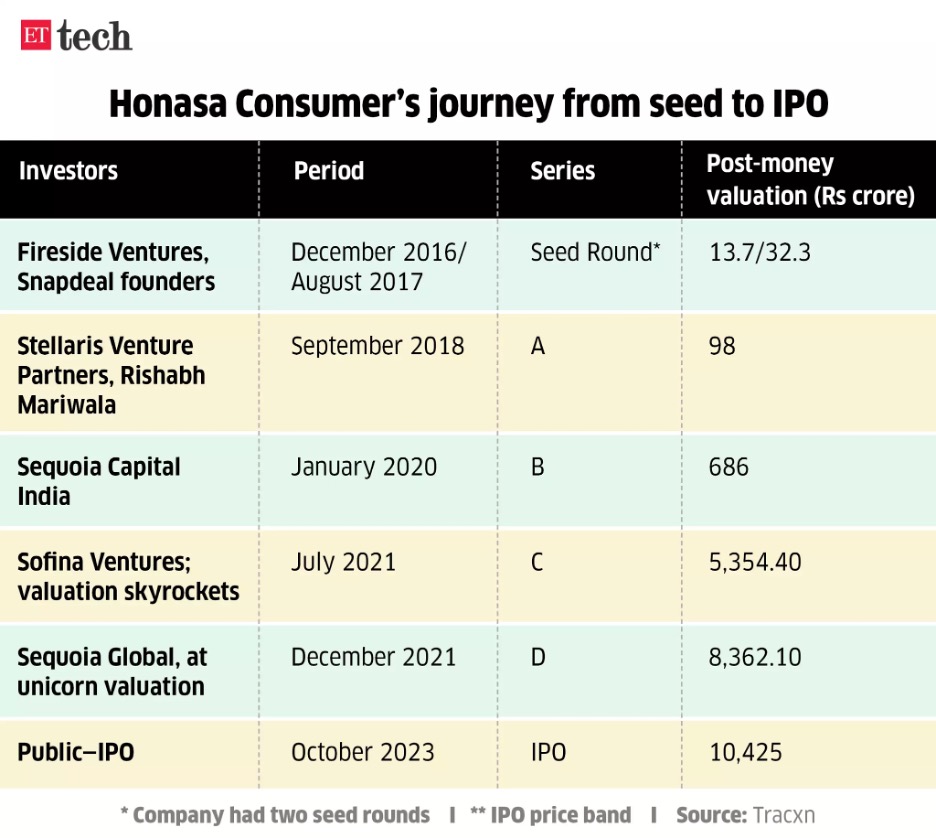

As for Mamaearth, an IPO had been long in talks. Mamaearth is a part of the product portfolio called Honasa comprising a total of 6 companies and falls in the category of Personal care and Beauty brands. The founders are Varun Alagh and Ghazal Alagh while the promoters(a) include both the founders and Sequoia. While the company boasts of a wide user base with much social media presence, the news of the IPO seems to create more noise than music. The reasons can be multiple. For a long time, the company has been finding it difficult to maintain steady profits. As per their balance sheets, the company recorded a loss of Rs 1331 crores in March 2021.

In March 2022, they earned a profit of Rs 14 crores. Indeed, it was a green signal for a prospective IPO. However, things turned upside down when the year 2023 came with a loss of Rs 141 crores indicating a threat to the IPO. This loss was majorly attributed to the acquisition of the company called Momspresso which according to RHP(b) was scaled down on various business fronts ahead of the IPO. The company boasts of a great gross profit of around 70% however fails when it comes to revenue. This is primarily due to the high amount spent on marketing and advertising. The company does not manufacture the products nor has a patent(c) under its name. Heading back to the IPO, the company has demanded a valuation of 10,000 crores while holding its own asset value at 1048 crores. The P/E ratio(d) for the same comes out to be 390 (with EPS as 0.83) which when compared with the sector P/E of 46 breaks all expected norms. The figures reflect a wide disparity when compared with competitors and call for a careful evaluation by retail investors.

Shareholding pattern

The shareholding pattern involves Varun Alagh owning 34.3% of the shares and Ghazal Alagh owning 23% of the shares in the company. The VC firm Sequoia owns 24.01% of the firm. Other shareholders are Bollywood actress Shilpa Shetty and Marico’s Rishab Harsh Mariwala amongst others. The founders will be offloading their shares 31.86 lakh and 1 lakh shares respectively.

IPO Size

The total IPO size(e) is of Rs 1700 crores wherein there are fresh issues worth Rs 365 crores and Rs 1335 issued as OFS(f). This points at the prospect of more money going into the pockets of the early investors and promoters and less being left for the company to invest in its operations. The company had reserved 75% of the issue for Qualified Institutional Buyers (QIBs), and 15% for the High Net-Worth Individuals(HNIs) portion. For retail investors, the company had reserved 10% of the issue size. The promoters seem to be making enormous profits from the IPO.

Snapdeal’s co-founder Kunal Bahl and Rohit Kumar Bansal’s acquired shares of Honasa at an average cost of Rs 3.21 per share each and at the upper end of the price band (Rs 324), they will make up to rs 36.54 crores of individual profit by selling 11,93,250 equity shares each. Marico’s promoter, Rishabh Harsh Mariwala’s weighted average cost of acquisition was Rs 6.05 per share. He will be making gains of about 54 times for 57,00,188 equity shares being offered in the OFS. His absolute profit, net of cost, is likely to be around Rs 181.23 crore. Bollywood actress Shilpa Shetty Kundra, who is offering 13,93,200 equity shares in the OFS process, acquired shares at Rs 41.86 apiece, will make gains of about 8 times over her investment. Her absolute profit in the issue is seen at Rs 39.30 crore. While the IPO size for the company may have reduced significantly from what was proposed in 2022, there are still some loopholes that need to be mended.

What’s the conclusion?

The company has advantages owing to its wider digital reach and user base, omnichannel distribution strategy , visionary founders, consumer centric innovation and positive gross profits. However, an unstable revenue, controversies around bad acquisitions, offloading of shares by promoters and founders, more money going towards the early shareholders and less towards company growth, less retention of customers, unusual P/E as per the industry and the absence of a patent make the investment risky for retail investors especially risk-averse investors.

Glossary

a. Promoters: Promoters are individuals or entities that have founded the company or have been instrumental in its early growth. Mamaearth’s major promoters are Varun Alagh and Ghazal Alagh.

b. RHP: A Red Herring Prospectus (RHP) is a preliminary registration document that is filed with SEBI in the case of a book building issue which does not have details of either price or number of shares being offered or the amount of issue.

c. Patent: A patent is the granting of a property right by a sovereign authority to an inventor. Mamaearth does not have a patent which means that any other company can utilize the same third party manufacturer or even the same products.

d. P/E ratio: The price-to-earnings (P/E) ratio relates a company’s share price to its earnings per share. A high P/E ratio could mean that a company’s stock is overvalued, or that investors are expecting high growth rates in the future. For mamaearth, the P/E is high as compared to the sector P/E indicating possibility if the stock is overvalued.

e. IPO size: The Issue size in an IPO means the number of shares issued multiplied by the amount of each share.

f. OFS: An Offer for Sale is a simpler method whereby promoters in public companies can sell their shares and reduce their holdings in a transparent manner through the bidding platform for the Exchange. The IPO saw the sale of 3,186,300 shares by Honasa promoter Varun Alagh and up to 100,000 shares by his wife Ghazal Alagh. Others included Shilpa Shetty,Snapdeal’s Kunal Bahl amongst others.

Written by – Arushi Bhatt

Edited by – Shamonnita Banerjee