?By Saurabh Aggarwal

The Q3FY17 has been, by far, the most unexpectedly eventful quarter of the last five years, the prominent events highlighting the quarter would be Brexit, India’s Demonetization and election of Donald Trump, a real estate mogul, as the president of The USA. Well, it all happened for good. At the Dawn of the New Year, the investors are making profit bookings ahead of the events like quarterly results, GST implementation and Union Budget. Perhaps, the needed correction to the Bull Run is in turn giving room for new capital to flow in. Going back to 1HFY17, Nifty saw a great rally making all time high of 8952. Whereas, if we were to consider the absolute return (8th Jan, 2016 to 6th Jan 2017), it would be 8.44%. Investors, speculators and traders are expecting good quarterly results. Week gone by saw Nifty inching higher 0.7% and closed near 8250 level. India VIX remained sub 15% with not much activity.

The Q3FY17 has been, by far, the most unexpectedly eventful quarter of the last five years, the prominent events highlighting the quarter would be Brexit, India’s Demonetization and election of Donald Trump, a real estate mogul, as the president of The USA. Well, it all happened for good. At the Dawn of the New Year, the investors are making profit bookings ahead of the events like quarterly results, GST implementation and Union Budget. Perhaps, the needed correction to the Bull Run is in turn giving room for new capital to flow in. Going back to 1HFY17, Nifty saw a great rally making all time high of 8952. Whereas, if we were to consider the absolute return (8th Jan, 2016 to 6th Jan 2017), it would be 8.44%. Investors, speculators and traders are expecting good quarterly results. Week gone by saw Nifty inching higher 0.7% and closed near 8250 level. India VIX remained sub 15% with not much activity.

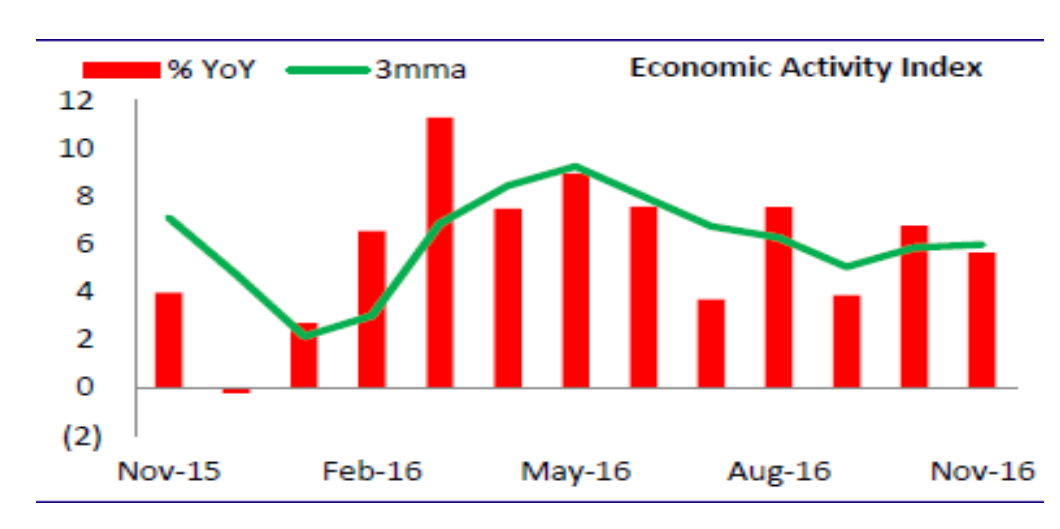

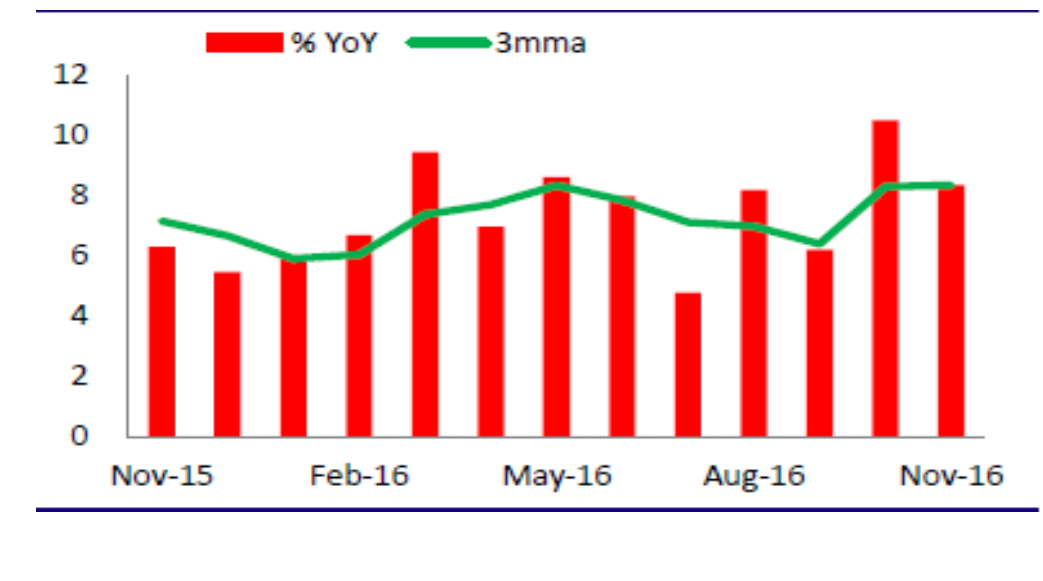

Assumptions as per the monthly Economic Activity Index (EAI) issued on 6th Jan, 2017:

- India’s economy grew decently in November: The country’s EAI grew by 5.6% in November 2016 (Exhibit 1). It implies a growth of 6.5% YoY in the first eight months of FY17, as against 6% growth witnessed in the corresponding period last year. (EAI has a very strong correlation with the real GDP)

- Strong growth of consumption: High growth in passenger traffic both in railways and airways. Rural wages were at its all time high. Considerable growth in government’s revenue spending, increased petrol consumption attributed the consumption to grow at 8.4% YoY.

- Realization of revenues: Growth in cargo traffic, growth in power generation and increased production of capital goods. Although, weak demand of consumer durables and less imports of capital goods due to demonetization. Investment Index shrank 2.5% as against 3.5% in the corresponding period last year.

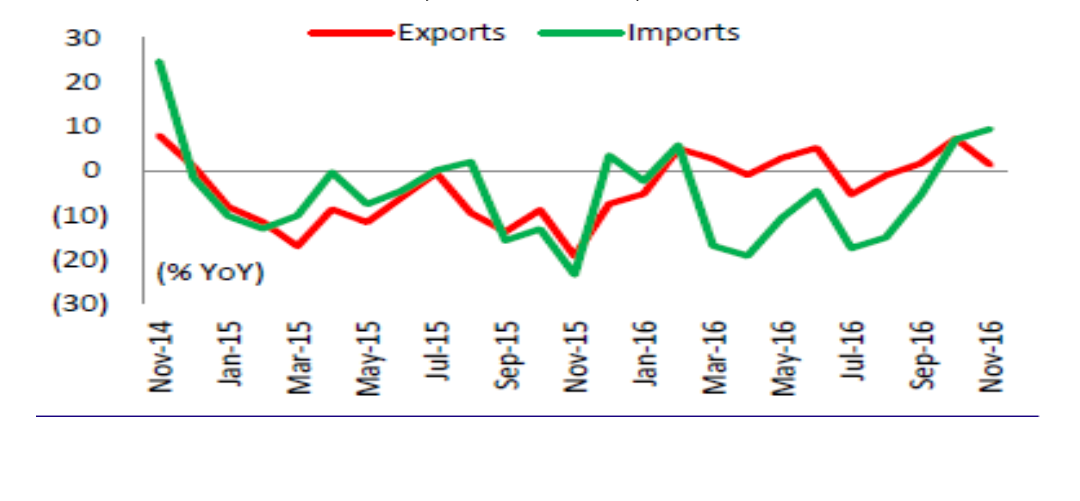

- External trade acted as a drag in November 2016: Finally, faster growth in imports in November led to significant widening in trade deficit, which acted as a drag on EAI for the first time in ten months.

Events:

Brexit: Britain ruling to get out of European Union will have impacts on trade and commerce but in bits and pieces. The impacts of Events like this will depend on the different policies adopted for different sectors. Also, from Indian economy’s perspective it is beneficial, as the country will be able to directly negotiate deals than with the Union as a whole. Latest development on the matter is that the parliament has finally voted to exit EU. Positive for Indian economy.

Donald Trump winning US elections: With the new president-elect we can expect an outflow of FIIs to US economy. Fed has decided to have three chances in FY18 for the rate hike. Also the curtailment of increase in number H1-B visas will play a negative impact on Indian IT sector.

Demonetization: The demonetization of currency had radical effects on the economy as it compelled the manufacturers and consumers to decrease their respective production and consumption. It had negative effects on the economy for the quarter Q3FY17 but we can expect unorganized sectors to move to organized with great growth and an optimistic approach.

Sectors like realty, consumer durables and discretionary and banking have huge potential to grow in the year. A Bearish outcome on Indian IT, consulting and software sectors can be seen, as the bill in the US Congress for limiting the jobs and reforming the country’s high-skilled immigration program has been proposed. The FIIs have been pulling out cash but the domestic institutional investors have been pumping in. Based on the assumptions and a strong faith in Indian equity markets, there is a huge growth story yet to come up. Also, nation’s demographics will prove to contribute immensely to the economy.

Note: Estimates of Economic Activity Index (EAI) for the month prior to the recently concluded month is released in the first two business days of every month. November EAI is released on 6th Jan, 2017. Bloomberg terminal as on 6th Jan, 2017