Amidst the global pandemic, when the Indian Economy is already under great duress, caught in a vicious cycle both in domestic and external sectors, the situation just got slightly worse after Moody’s Investors Service, a US-based Bond Credit rating Corporation, downgraded India’s foreign currency and local currency long term issuer rating to Baa3 ( acceptable ability to repay short term debt) from Baa2 (high ability or acceptable ability to repay short term debt) while maintaining a negative outlook, citing a prolonged period of low growth, further deterioration in government’s fiscal position and a prolonged erosion in India’s financial sector.

Moody’s, Standard & Poor’s (S&P) and Fitch are three prominent and renowned credit rating agencies. We had already seen Fitch downgrading India’s ratings to negative in the backdrop of Coronavirus outbreak but Moody’s, a company which has been historically so optimistic about India, giving a negative outlook in this rough phase for the economy somewhat implicates that it might be at the cliff’s edge of an imminent downgrade.

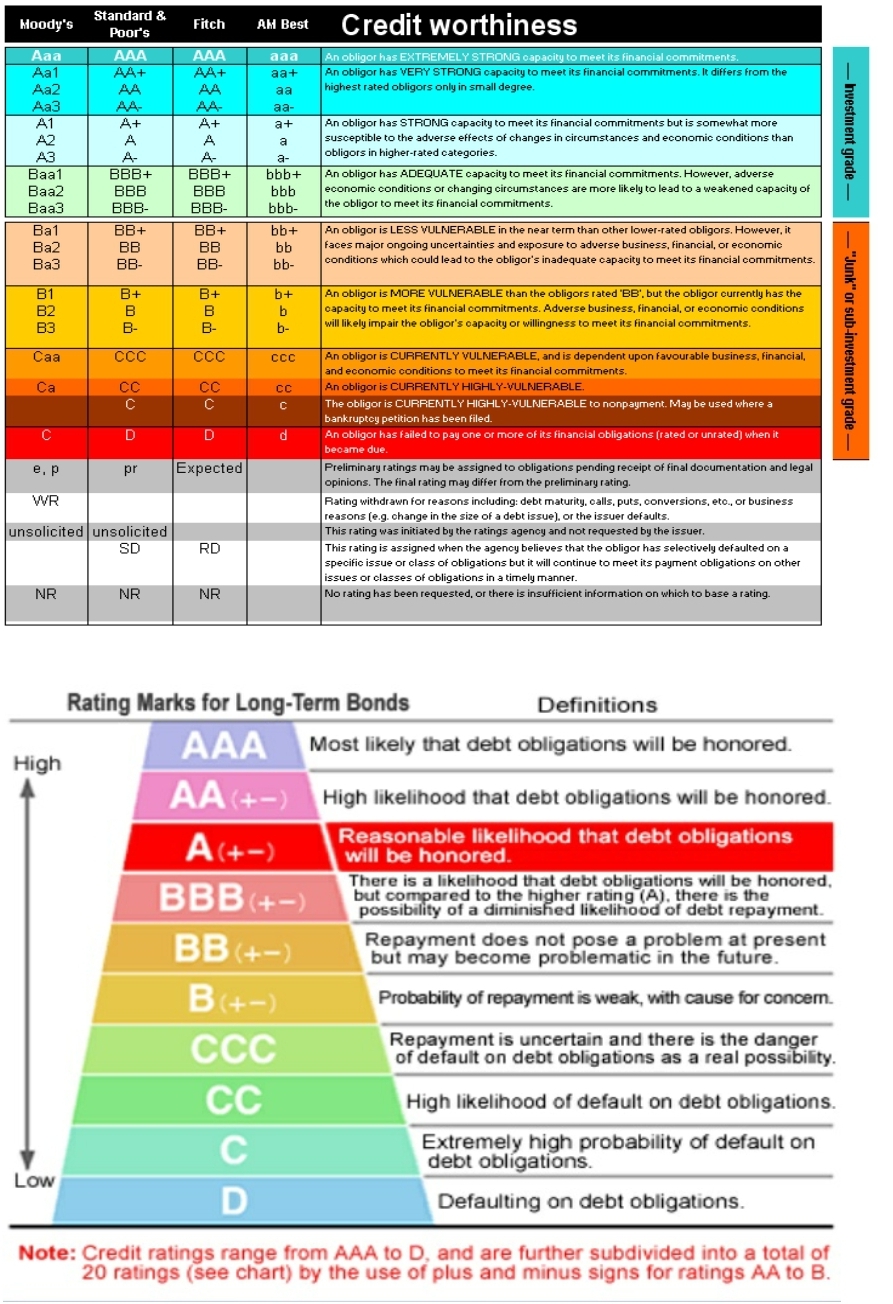

According to the ratings, India is 18 to 24 months away from being downgraded to ‘junk.’ The global credit rating agencies consider a rating of BBB (minus)/ Baa3 and above to be ‘investment grade.’

The government of the policymakers of an emerging market economy, thus, strive to be rated at least as an ‘investment grade’ destination. This demarcation allows an emerging market to become more ‘investable’ in global investment portfolios. Thus, it drives foreign inflows into India and enables the Indian Government and companies to access the global markets in a greater manner.

Twenty-two years ago, on June 19, 1998, Moody’s had downgraded the economy as an aftermath of the country’s nuclear tests. In contrast, in 2003, on the back of five years of substantial reforms by the NDA Government, it became the first rating agency to upgrade India from junk to investment grade, and it had been very optimistic about it since then.

In its official statement, Moody’s said, “The decision to downgrade India’s ratings reflects Moody’s view that the country’s policymaking institutions will be challenged in enacting and implementing policies which effectively mitigate the risks of a sustained period of relatively low growth, significant further deterioration in the general government fiscal position and stress in the financial sector.”

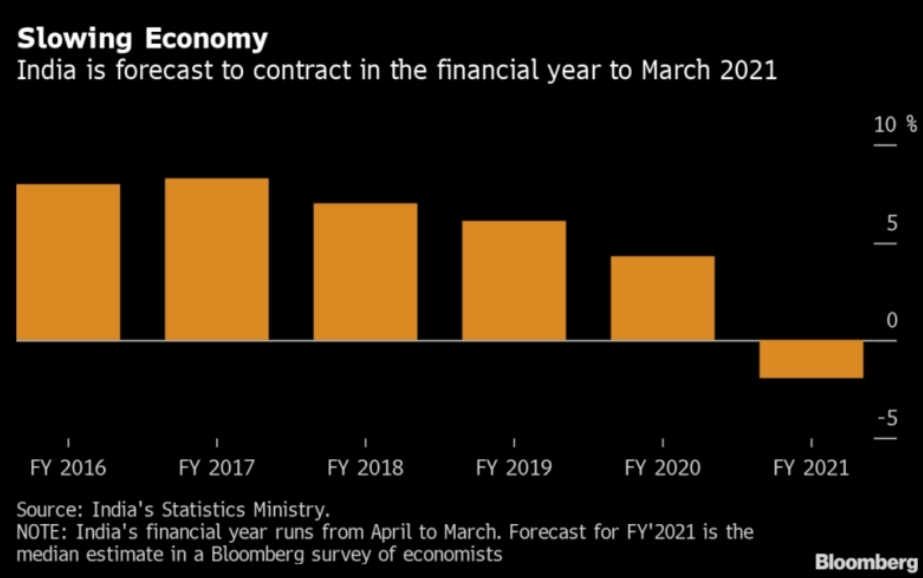

Taking the statement into consideration, if we observe the pattern, we would realize the growth in the economy appears to be a bit stunted after the introduction of GST. India’s growth outlooks have deteriorated sharply this year with a crunch that started in the shadow banking industry spreading to retail businesses, carmakers, home sales, and heavy industries. Growth has come down to a six-year low of 5% with Moody’s saying there’s a low chance of sustained growth at or above 8%.

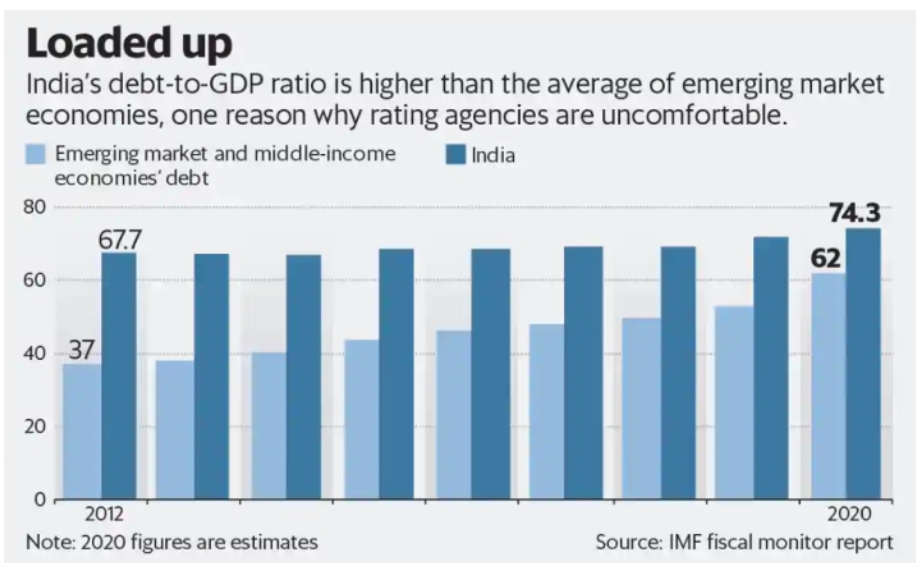

A significant deterioration in the fiscal position of government (both central and state) is detected because of less revenue generation. NPA’s continue to create a problem for the banks. On top of that, amidst the pandemic situation, the government has been allowing taxation and moratorium relaxations, and extension of the payback period for loans. This, too, adds undue pressure on the country’s fiscal position, which shall further deteriorate the fiscal deficit position. According to Moody’s, India’s estimated general government debt burden of 72% was quite high. This number is set to go up to 84% within 2020, as the government will be forced to borrow more.

Now summarizing all this up, if we try to have a close look at the bigger picture, we would realize the importance of ratings. Ratings are based on the overall health of the economy and the state of government finances. When India’s sovereign rating is downgraded, it becomes costlier for the Indian government as well as all Indian companies to raise funds because now the world sees such debt as a riskier proposition. As a result of the negative outlook, we can lose the potential investors who are willing to invest and help our economy grow. India’s nominal GDP growth has also been below 10% for the last two years and is expected to be so for at least two more years. The banking and financial sectors have been a mess, and India’s job creation problem is turning the demographic dividend into a disaster.

In such a scenario, was Covid-19 the only straw that broke the Camel’s back?

No. Moody’s was categorical that while this downgrade is taking place “in the context of the Coronavirus pandemic, it was not driven by the impact of the pandemic.”

According to Moody’s, “the pandemic amplifies vulnerabilities in India’s credit profile that were present and building before the shock, and which motivated the assignment of a negative outlook last year.”

In particular, Moody’s has highlighted persistent structural challenges to fast economic growth such as “weak infrastructure, rigidities in labor, land and product markets and rising financial sector risks.”

However, the Government reacted strongly to this negative outlook by the rating company, and the finance ministry issued a statement saying, “India’s relative standing remains unaffected.” The government explained that the fundamentals of India’s economy remain “quite robust” and the recent series of reforms would stimulate investments and strengthen the economy.

Not only this, a day after India’s sovereign rating downgraded, Moody’s also cut ratings of eight non-financial companies, including Infosys, TCS, ONGC, and three banks, SBI, HDFC Bank and EXIM. It also downgraded seven Indian infrastructure issuers, including NTPC, NHAI, GAIL, and Adani Green Energy Restricted Group, by one notch. Issuer ratings of IRFC and HUDCO have also been lowered.

After all this, the Indian government had a really hard time trying to make people understand that it was still on the right track when the stock markets jumped in for their rescue.

Stock markets on Tuesday (2nd June 2020) ignored the rating downgrade by Moody’s and rallied 1.57 percent even as Prime Minister Narendra Modi maintained that the country will get back its economic growth and pledged to undertake more structural reforms. The markets shrugged off news regarding the downgrade, which was trumped by the expectation of the economy opening up. In spite of many possible negative triggers, it was seen that positive sentiment was still driving the market.

But do you think that a positive sentiment or instilling few hopes among the Indian masses of an increasing GDP would keep the market under control for a long time, or should the government now realize, the gravity of the situation and start working right from the fundamentals with their focus and ideas aligned more towards the long term benefits, rather than the short term goals?

Until then, let’s open our eyes and face it when Moody’s is finally ringing the bell and making us realize that clearly ‘All’s not well’ with our economy.

- By Muskaan Kumari

Sources cited:

- The Economic Times

- Bloombergquint