In 1991 the clouds of doom were in India, its imports increasing and due to lack of funds to fund them, the government was forced to take a loan from IMF on the guarantee of its gold reserves. India had only $1 billion worth of reserves left when the then Government headed by P V Narasimha Rao decided on the recommendation of then finance minister Dr Manmohan Singh.

Rest is history India was released from its cage in which it had entered soon after independence to be free once again, the market was liberalised and opened, LPG (Liberalisation, Privatisation, Globalisation) was implemented.

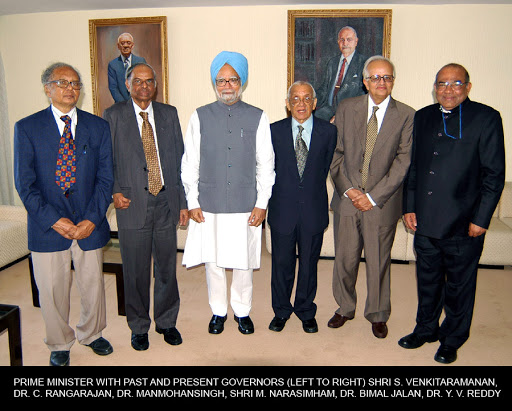

The real sector was reformed but what about financial sector for that a committee under the chairmanship of M. Narasimham, a former RBI governor was constituted to recommend the reforms, its official name was committee on Financial System it was appointed by Dr Manmohan Singh and another also under chairmanship of M Narasimham was appointed by P Chidambaram to check the pace and also recommend the reforms in banking sector.

This article is on the second committee whose report was submitted on April 22, 1998, to then Finance Minister Yashwant Sinha.

Why is it important?

It is important because when the next crisis knocked on our doors it was that protected us, in other news the recent merger of State Bank of Patiala, State Bank of Hyderabad and other State Banks with State Bank of India was in some ways recommended by the Committee

The crisis is a question whose answer I will tell you at the end (Hint: it is famous).

It gave birth to the first Indian Universal bank, Industrial Credit and Investment Corporation of India or in simple words ICICI bank.

Recommendations of the committee

• Increase and management of capital adequacy ratio; Capital Adequacy Ratio (CAR) is the capital required by banks to hedge their risks, it is the amount required to protect the bank from adverse risks of the open market. It was recommended that Government and government approved securities should have weightage of 5% as they will be traded on the market.

• Also, market risk should also be counted with credit risk. To reduce problems it can be implemented in phases.

• Due to the opening of the economy, there is a requirement of 5% of capital to hedge foreign market risk this capital should have 100% risk weightage.

• Including all above suggestions, it is recommended that CAR should be increased to 10% in phases with an intermittent target of 9% to be achieved by the year 2000. RBI can increase and decrease the CAR for specific banks. Banks should not be dependent on the budgetary distribution and banks that are able to raise funds from domestic or abroad should be encouraged to do so.

Next recommendation is a recommendation that has risen its face again in the ongoing NPA crisis, it was on Asset quality, NPAs and Direct Crediting;

• Due to a large number of public sector banks and their large number of NPAs the government had to spend 20000 crore for recapitalisation of these assets. As it is highly expensive and unsustainable in long run the committee recommend the ARF (Asset Reconstruction Fund) approach as recommended by the previous committee

• It has being decided that any asset which is in sub-standard category for 18 months for the first instance and for 12 months thereon should be counted in doubtful category

• All Government guaranteed advances which would otherwise be considered Non-Performing Asset (NPA) should be mentioned differently for fuller transparency and greater organisation

• The Committee believes that the objective should be to reduce the average level of net NPAs for all banks to below 5 per cent by the year 2000 and to 3 percent by 2002. For those banks with an international presence, the minimum objective should be to reduce gross NPAs to 5 per cent and 3 per cent by the year 2000 and 2002 respectively and net NPAs to 3 per cent and 0 per cent by these dates. These targets cannot be achieved in the absence of measures to tackle the problem of the backlog of NPAs on a one-time basis and the implementation of strict prudential norms and management efficiency to prevent the recurrence of this problem.

• For banks with higher numbers of NPAs in their portfolio, the committee recommends two ways for whom the ARF can’t be taken. First is the establishment of an Asset Reconstruction Company (ARC). Which would take over all the loan assets in a loss-making and doubtful category by buying them from the bank at realisable value i.e. the actual value of an asset if it would have been sold. The payment will be by NPA Swap bonds if stamp duties are not excessive.

• ARC can be established by a single bank or group of banks or by the private sector. If banks establish the ARC then they should provide staff by way of transfers or deputation. This is to ensure the staff has an institutional memory of NPAs. The funding of such companies can be done by treating them on par with venture funds for tax incentives. For this process, the Government should provide Tax incentives and minimal stamp duties. Other banks can securitize these bonds

• The alternate process will be the issuance of bonds on the realisable value as tier II capital. This will help to bolster capital adequacy and since banks will find it difficult to find buyers the government should back these bond instruments.

• Direct credit is the largest cause of NPAs for banks. The committee had decided to reduce the credit to be given to priority sector to be reduced from 40%to 10% but on discussion with government it has being decided that current practice can continue

• As banks have to already keep resources reserved for weaker sections to the tune of 10% other sectors may not require.

• Also, loans to SMEs and other priority sectors should be provided on basis of creditworthiness of the business.

• Interest rates for loans below 2 lakhs should be deregulated. The bank manager has the onus to decide the worthiness of the person applying for government scheme.

Other important recommendations:

• Banks should have a separate operation manual that is which is up to date

• The remunerations of chief executive, directors should be based on the market and not decided by government

• The term of the chief executive of a public sector bank should be meaningful and not less than five years. Intermittently it can be three years.

• The RBI cannot act as both regulator and owner of bank and has to disinvest from SBI

• To provide for banks to tap the capital market the government should disinvest to 33% from current limit of 51% by passing of law.

• The vigilance department should be trained on banking operations

• DFIs and other banks should be allowed to merge if none of them is a weak bank.

Implementation

The implementation was delayed due to protests by RBI employee union and other bankers union. Also, it was considered anti-poor, capitalist on its recommendations of rural and SME investment.

But many of the recommendations were implemented with the help of Khan Committee which was appointed by then RBI governor Bimal Jalan under the chairmanship of SH Khan who was the chairman of IDBI bank.

The recommendations pertaining to RBI and deregulation and merger of banks and formation of a three-tier banking sector was implemented.

Banks are provided greater autonomy to function and hire from the market.

The formation of the ICICI bank as a universal bank was the reason of this committee.

Sources:

Bulletin of RBI

RBI press release

SH Khan committee wants institutions to evolve, morph into full-bodied banks the Indian Express April 25, 1998

The answer is 2008 subprime mortgage crisis

To read the whole text of the report visit RBI

By Aviraj Singh Mehta