On the 31st of January 2024, the Reserve Bank of India barred Paytm Payments Bank from offering practically all its key services after February 29 due to persistent non-compliance and material supervisory concerns.

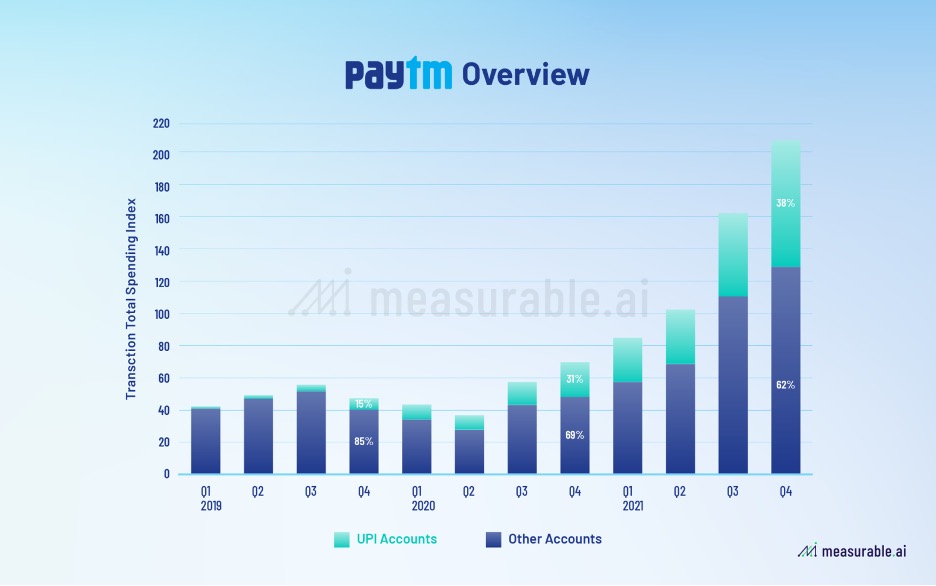

Think of making an online payment or simply using a UPI app, and Paytm will likely be the first thing to come to mind. Paytm or Paytm Wallet has captivated the Indian audience to the extent that it has become synonymous with UPI apps. According to the Paytm Payments Bank website, it has 100 million KYC-verified customers. The bank also claims to be the largest issuer of FASTags, with over 8 million FASTag units issued.

Within two days of the announcement, there was a huge drop in the share market price, plummeting by 36% to its lowest recorded point at 487. As a result, Paytm lost $2 billion in market value, affecting 300 million wallets, 30 million bank accounts, and 8 million FASTags in the Paytm portfolio.

By the 29th of February, Paytm Payments Bank will not be able to accept fresh deposits and will not be allowed to facilitate transactions via Savings bank accounts, wallets, FASTags, and UPI facilities. The question arises: why is the FASTag facility being affected? In this article, we delve into the backend tech of the UPI.

Whenever a transaction is made, such as from a customer to a merchant for the payment of any good, virtual money gets transferred from the customer’s bank account to the Nodal account via Paytm. Within 24 hours, the money gets transferred to the merchant. Here, the Nodal Account acts as an interim escrow where payments are pooled before being sent to the merchants. By looking at the suffix of the UPI account, one can observe that “@paytm” indicates that the Nodal account is with Paytm Payments Bank. Similarly, users of PhonePe will have their suffix as “@ybl”, indicating the existence of a Nodal account with Yes Bank. Another example is Google Pay, which is linked with HDFC Bank. This is because PhonePe and Google Pay rely on Yes Bank and HDFC Bank for Nodal bank services.

On the other hand, Paytm had been relying on its payment bank for its nodal account services for many of its transactions. This is how customers’ UPI and FASTag services are affected because Paytm Payments Bank is now restricted by the RBI.

What is the solution? To sustain itself in the market and save its customer base, Paytm has to change its Nodal account to another bank, which is indeed a difficult task. In December 2023, PPB recorded 2.8 billion transactions out of the 12 billion transactions made via Paytm. Now, the task is to find partners to process almost 3 billion transactions before the 29th of February. It takes an average of 2 to 3 months just to set up a Nodal account, let alone building the capability to process 3 billion transactions.

It is speculated that Yes Bank and ICICI have the potential and infrastructure to seize the opportunity. If the speculation proves true, these banks will benefit from the RBI restrictions.

The second issue that Paytm must address is their merchant issue. Paytm has an estimated 37 million merchants who use the Paytm payment bank to receive money. The burden is now on Paytm to convince these merchants to stop using Paytm bank accounts and link to other bank accounts for their UPI addresses. They might also have to change their QR codes. Issuing new QR codes and updating them on the millions of soundboxes linked to Paytm Payments Bank poses a significant logistical challenge.

Additionally, another issue is the disruption to the ecosystem. Paytm had strengths in its strong relationships with its merchants and the range of products and services it could offer with its backend system provided by Paytm Payments Bank. Now, this ecosystem is being disrupted, putting Paytm at risk of losing a large number of merchants to other platforms, which may result in losses of 300 to 500 crores.

Also, considering that lending exceeds 20% of their revenue, it will affect their partner relationships and a large chunk of revenue.

Now, the most important question arises: Why did the government take such harsh steps towards Paytm, despite it being a savior for India during demonetization and filling the credit gap in MSME in India? Paytm Payments Bank received its license in 2015 and started operations in 2017. Paytm included a clause in its KYC form, making customers have a default Paytm payment bank account as a result of doing KYC. Since KYC was required to use features like the Paytm wallet, millions of users in 2015, 2016, and 2017 opened up a Paytm bank account by default. Now, this is a gray area because they did not obtain direct consent from the customers to open a bank account. Another set of challenges emerged when Paytm started their savings account in 2017 and recruited agents. The situation worsened as agents were incentivized to help people open savings accounts with a payment of 50 rupees. These agents attracted more agents, creating a multi-level marketing scheme. The main issue was that how these agents obtained consent from the people was not clear. Here, the RBI intervened and prohibited Paytm from opening more bank accounts, as it found that third-party agents were making decisions for consumers to open bank accounts.

Lastly, in the latest hearings about banning Chinese loan apps and betting apps, Ant Financial and Softbank, Chinese companies, hold 9.89% and 6.46% stakes in the company, respectively, according to stock exchange data as of December 2023. This raised concerns for the Indian government about the possibility of data leaks to China, which is why the government had been closely monitoring Paytm for some time.

To conclude, the Indian Government will always control the business ecosystem, where geopolitics plays a vital role. What remains to be seen is how Paytm handles this situation and makes a comeback in the market.

Written by – Riya Kumari Shah

Edited by – Kushi Mayur