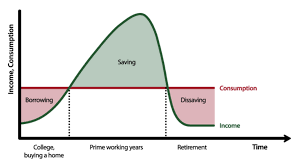

Permanent Income Hypothesis.

Related Posts

New Dawn for Indian Agriculture

Budget 2025 takes a bold step towards transforming Indian agriculture...

Income Tax reforms

The Indian government’s crucial economic document, the Union Budget of...

The Adani Saga

The Adani Group, one of India’s largest business conglomerates, finds...