A study into the impact of COVID-19 on corporate debt and a striking resemblance to previous financial crises.

What is corporate debt and why is it a ‘bubble’?

Over the course of the last decade, corporate debt has been increasing significantly as deceptive market conditions and low interest rates have led corporations and businesses into borrowing massive amounts of debt. The effect of such ‘irresponsible borrowing’ is only bound to get worse with the COVID-19 pandemic. This article seeks to analyse the impact of a global pandemic on corporate debt and how a prolonged economic shutdown might catalyse a financial crisis.

It offers an insight into the history of financial crises and draws a parallel between them. The article follows a trajectory from explaining the various possible links between each crisis to describing how the bursting of the corporate debt bubble is an example of history repeating itself and why it is bound to happen again in the future.

With the onset of COVID-19, oil and travel companies found themselves in the middle of a deadlock. Earlier, the oil companies had raised substantial corporate debt due to low interest rates in the market, expecting sharp rises in oil prices. As times get tougher, these sectors are being driven towards default and bankruptcy. An easier corollary would be – as we observe a precipitous fall in demand and consumption of services (including hotels, restaurants, flights) the companies are bound to default on their debts because of overall lower incomes.

To worsen the situation, US, European and Australian stocks are moving into bear market territory as a direct consequence of various travel bans and the economic slowdown. A bear market is characterized by investor’s transition from over-optimism to panic and pessimism. Corporate debt refers to the floating of corporate bonds by an organization. Corporate bonds are a form of debt security instruments issued by companies looking to increase liquid cash in their organization.

In exchange, corporate bonds are desirable from an investor’s point of view as they get several interest payments at a fixed or variable interest rate. Corporate debt is a product of “leveraged-lending” i.e. firms borrowing more when they are already in considerable amounts of debt. It is usually calculated as the ratio between a company’s net debt to EBITDA. While the average firm carries a net debt to EBITDA ratio of 3:1, Boeing, an exception has its debt ratio at 17:1 due to the 737 crisis.

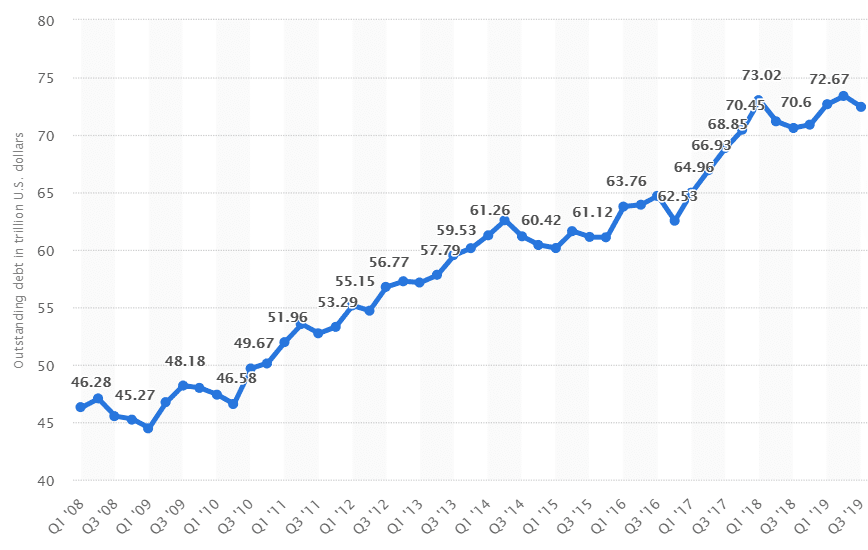

According to OECD, the global non-financial corporate debt as of 2020 was 13.5 trillion USD, which is twice the outstanding debt in 2008. For 2021, total debt is expected to remain broadly flat, but net corporate debt will spurge as companies have begun to spend their enormous cash reserves to restore optimum business operations. Net global corporate debt is set to rise by 500-600 billion USD this year. This torrent of inexpensive money has benefited all sectors of the economy, from airlines to theatres, cruise operators and hotel businesses.

For an in-depth understanding of why the corporate debt bubble is a “bubble” in the first instance, we have compiled some of the fundamentals of corporate borrowing:

1) Why bonds and not shares? For a business, debt financing is cheaper than equity financing and is preferred as it does not involve giving up control of the company.

2) Why corporate bonds and not bank loans? Issuing bonds is preferred over taking bank loans as bonds carry fewer restrictions than bank borrowings (e.g. a bank may set an upper limit on taking loans till a company is able to pay off its previous debts).

3) Low-interest rates- Corporations have undertaken crippling amounts of debt due to the sole reason that the yield on them is lower than any other form of debt. Corporate bonds are seemingly lucrative for the investors as they are less volatile (fluctuation in returns is less).

4) Inferior investor protection, looser restrictions on corporate debtors- Since corporate bonds are not backed by any real collateral, it makes them highly unstable and vulnerable to market risks.

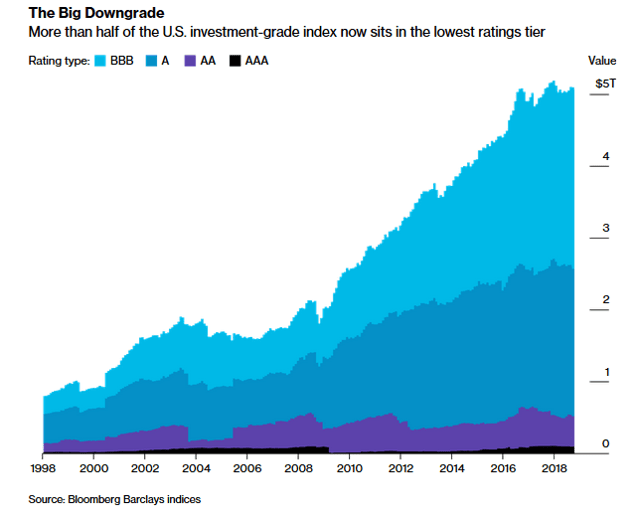

5) Decline in over-all bond quality- Almost all bonds are evaluated by credit rating agencies based on the issuer’s ability to pay back its debts or the ‘creditworthiness’ of a company. Based on this classification, bonds are divided into investment-grade and non-investment grade (or speculative) bonds. Bonds carrying a credit rating of AAA to BBB fall within the investment grade category and have relatively low-credit risk. Meanwhile, bonds with ratings below BBB are non-investment grade and carry a greater risk of default.

According to a report by OECD , in 2019 the issuance of non-investment grade bonds reached an all-time high of 25% of the total corporate bonds. More significantly, BBB bonds (the lowest rating bonds which enjoy the investment-grade status) peaked at 51% of the total investment-grade issuance. During 2000-2007, this percentage was just 39%.

6) Sell-offs- Considering the rise in issuance of bonds which are one level above ‘junk’ (i.e. BBB rated bonds) a downgrade to non-investment grade bonds might force investors to sell-off their bonds and put overarching pressure on the global bond market.

More than 50% of US corporate debt is BBB

How the corporate debt ‘bubble’ is likely to burst post-covid?

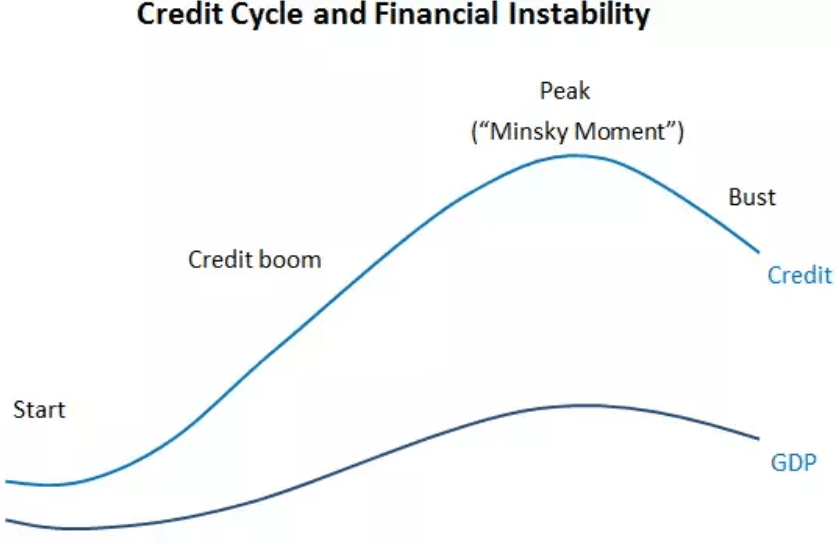

Charles Kindleberger’s Anatomy of Crisis

“The difference between genius and stupidity is that genius has its limits.”

–Albert Einstein

The logical answer to that would be ‘simply because bubbles, by definition, always burst’. All economic bubbles are preceded by unsustainable economic activity. The factors constituting the bubble keep growing exponentially, finally causing it to implode.

Charles P. Kindleberger, in his book Panics, Manias and Crashes has outlined the basic structure of an economic bubble and delved into the impact of such bubble-formation, which ultimately results in a crisis. He has divided the structure into 5 phases:

1) Displacement: ‘An outside shock to the economy’ or a steep rise in the anticipation of profits. In case of corporate debt bubble, this was represented by low-interest rates following the Great Recession (2007-08). A similar scenario took place in the 1990s with the widespread acceptance of computers and the internet, ultimately leading to the dot-com crisis.

2) Boom: A period of ‘take-off’ or speculative boom where investors’ expectation of higher returns and profits leads them to buy what they do not need. Often a pre-conceived notion reinforces itself in the minds of investors allowing them to make irrational investments. This coupled with lack of information, want of a more ‘dependable source of income’ and irrationality on the part of corporate investors led them to invest hugely in corporate bonds.

In the world’s top economies, many ‘zombie firms’ are solely surviving due to the availability of credit at very cheap rates. These companies make just enough profits to pay off the interest-part of their debts, but not the principal amount. While the number of such zombie companies rose, prospective higher-yields lured investors to invest in these ‘skeleton’ bonds. Traces of such a period can be dated back to 1600s when prices of Dutch tulips suddenly escalated by several hundred percent reaching all-time highs (Tulip Mania). Similarly, in the 2000s rising real-estate prices and sub-prime lending permitted the public freer access to credit.

3) Euphoria: A period of ‘over-optimism’. Boom shifts to Euphoria when investor’s expectations become irrational or in Kindleberger’s words, “rational exuberance morphs into irrational exuberance”. During a period of euphoria, investors become less opposed to risk. The ‘greater fool theory’ serves as a psychological proof to this period of mania. It states that there is a presumption by every investor that there is a “greater fool” in the market who will be willing to buy the stock at a higher price than what the investor had initially paid.

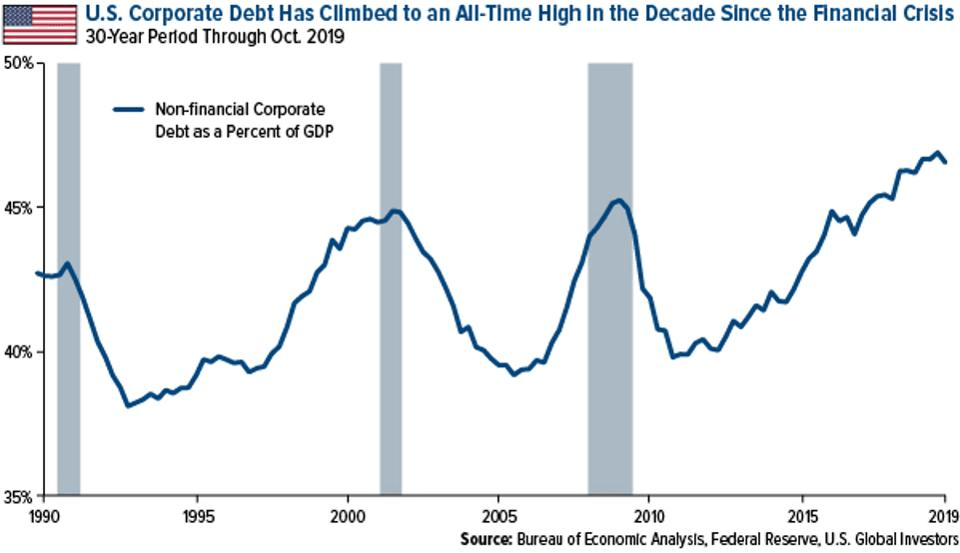

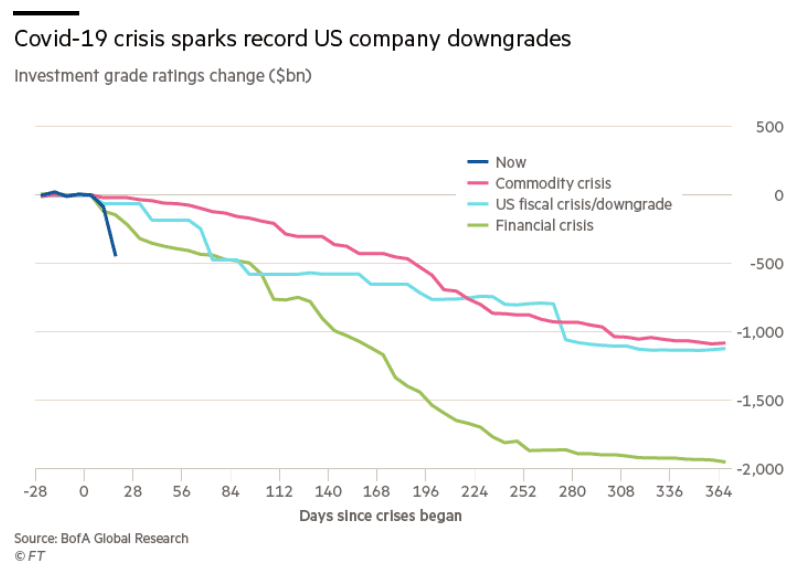

In the late 1990s doctors and lawyers were trading internet stocks in between appointments and tech stocks changed hands “three times as frequently as any other shares”. Corporate debt has been in a state of euphoria since the 2008 crisis as depicted below.

In case of non-financial corporate debt (excluding banks and other financial institutions) the figures have been continuously rising. The following graph(s) demonstrate the rise in corporate debt worldwide:

4) Distress: This is the ‘critical stage’ in bubble formation when buyers start to lose confidence. In 2008 financial crisis, the ‘distress’ phase began when homeowners started defaulting on home loans. Consequently, homebuilding companies, mortgage lenders and CEOs of investment banks had to dump hundreds of millions of dollars of stock. It is in this stage where “euphoric buying is replaced by panic selling”.

Distress stage in the corporate debt bubble was indicated by the shift from investment-grade bonds to non-investment grade bonds. As credit ratings dropped to BBB and below, the non-investment grade or ‘junk’ quality bonds led to investor pessimism. At this point, most prudent investors started selling off their bonds.

5) Panic: A period of ‘repulsion’. John Mauldin in his work Bubbles, Bubbles Everywhere draws an interesting, rather hysterical comparison between panic selling and the Roadrunners cartoon where the coyote keeps running off a cliff only to realize next that there is nothing underneath him. Such has been the position of investors in recent times. Clearly, the corporate debt bubble has surpassed the initial four stages of bubble-formation. As the COVID pandemic creates chaos in the economy, the bubble is likely to pop and lead to a market crash due to the combined effect of an overleveraged corporate sector, hampering of demand and supply, change in consumer behaviour, and indefiniteness of the virus.

NOTE: This is the author’s own interpretation and analysis of economic bubbles. There might be parallels drawn between dissimilar bubbles (debt bubbles and equity bubbles) but similarities have been pointed out only to offer empirical evidence substantiating the claim ‘what has happened before is bound to happen again’ and proving how investors have never really learned from their mistakes.

A “Minsky Moment” is Inevitable

Hyman Minsky has attributed the instability in the availability of credit as one of the most important factors leading up to a crisis.

During a bullish period, aggressive speculation by investors is accompanied by skyrocketing debts undertaken by both institutional and retail investors. Minsky has stated that there is an “inherent instability” in the financial market and the longer the period of such irresponsible, reckless speculation, the harder the economy is likely to crash.

During a bullish period, taking on extra debt seems not only irresistible but also profitable. It is at the height of this speculative optimism which Minsky has called the ‘Minsky Moment’. According to him, the shift in investors’ mindsets from confidence to scepticism marks this cycle. This is when borrowers (corporate organizations in our case) start realizing that their indebtedness is greater than their incomes and is hence, unsustainable.

A Minsky Moment has occurred almost each time before the past 5 financial crises. It is marked by an unprecedented rise in the price of an asset (Dutch Tulips in 1600s, real estate and stock market prices in Japan in late 1980s, tech-internet stocks in the 1990s, real estate again in 2000s finally leading up to the housing bubble) followed by bullish speculation and over-optimism on part of investors, ultimately causing a drop in inflated prices of the asset and marking the beginning of a recession.

The recovery from the Great Recession marks the beginning of the longest bull market in history, lasting more than 10 years. (2009-2019) It was driven by “slow but steady economic growth, record corporate profits and low interest rates”. Experts had earlier predicted the end of the ‘best bull market in history’ by the end of 2019 but corporate debt amongst other equity variables was at an all-time high, right up to February 2020. The outstanding global corporate debt at the start of the year was approximately 13.5 trillion USD meanwhile US’ S&P 500 index finished at record highs on 19th February. As of March, virus-hit stocks had seen a major downturn by 25% worldwide.

The last ingredient missing for a Minsky Moment to occur is — complacency . The fact that no one believes a financial crisis can happen can be the very root cause of ticking it off. In Economics, this is known as a self-fulfilling prophecy wherein investors’ pessimism turns into reality just because they believe it will, inevitably leading to a market crash.

At this juncture, a Minsky Moment is likely to prick the corporate debt bubble built up by low interest rates and declining credit ratings.

Crisis: An inherent feature of Capitalism

While the last two sections furnished the reader with a theoretical understanding of financial crises, this segment bases its argument on the fundamental structure of new-age capitalism. To quote Marx, “The real barrier to capitalist production is capital itself.” Grasping this concept involves an overview into the capitalistic system of production and the underlying contradictions within it.

The Labour Theory of Value initially postulated by Adam Smith and Ricardo and later reiterated by Marx states that ‘the value of a commodity is based on the labour put in to producing it”. Now, the everyday workings of a daily-wage labourer can be split into two broad parts: (a) producing value equal to wages received (b) producing surplus value. It is the latter (or “surplus value”) which is the source of all capitalist profits. Overproduction, appropriation of labour and exploitation of workers are the founding pillars of Capitalism.

The inherent conflict begins when in order to maximize profits, the bourgeois or the capitalist class start looking for ways to cut down workers’ wages to the bare minimum while being able to extract maximum surplus out of them. The aim of capitalism is neither economic nor societal growth, but profits only. This ultimately ends in a crisis of overproduction- thus “capitalism sows the seeds of its own destruction”.

The system employs the unparalleled rise in corporate debt as one of the countermeasures to such a crisis. As availability of credit helps only in stretching businesses and markets beyond their natural limits, such an increase in the availability of credit merely sustains the economy and prolongs the inevitable.

What happens once the ‘bubble’ bursts?

1) Most oil and travel companies are likely to face credit downgrades. ExxonMobil (US’ biggest oil company) has been downgraded from AA+ to AA by Standard & Poor’s Global Ratings . It further downgraded Boeing’s debt from A- to BBB due to the significant reduction in global air travel. A solution to this would be government intervention. Federal or Reserve Bank bailout money can help extend financial support to companies facing potential threat of bankruptcy.

2) Alternatively, corporations on the brink of bankruptcy can resort to the ‘debt-to-equity swap’ mechanism of corporate debt restrucuring (CDR), wherein creditors agree to forego some amounts of debt in exchange for a share in the distressed company. However, this would defeat the entire purpose of choosing debt financing over equity financing.

3) The Government, in line with central banks have announced massive stimulus packages to bolster the economy. This includes overwhelming credit programs meant to aid corporate borrowers. According to a Bloomberg report, investment-grade issuers issued 109 billion USD recently. However, these credit schemes are highly unlikely to help the non-investment grade issuers which account for more than 50% of the global debt.

Therefore, a suggestion to all governments would be regulation of credit flow. The government needs to be conscious of where the money is being used and which sectors of the economy need to be prioritized.

4) The RBI and Federal Reserve Bank have taken impressive measures to mitigate the probability of a health pandemic becoming a financial pandemic in the future. The US Federal Reserve has moved to purchase corporate bonds itself and laid down a two-fold approach. The first scheme would help companies to issue new bonds and the second is targeted at enhancing liquidity for outstanding corporate debts.

5) Similarly, RBI recently announced its “targeted long-term repo operation” or TLTRO which incentivizes commercial banks to invest in high-grade corporate bonds by offering them up to 1 lakh crore for a three-year period. This kind of intervention by a central bank is rare in case of monetary policy actions. TLTRO will have a direct and immediate impact. Lately, increase in yields would have put-off many issuers from issuing fresh corporate bonds but with RBI urging banks to invest in such bonds, new issues are likely to surge in the upcoming quarter.

Written by- Rishubh Agarwal

Edited by- Krish Sharma