The Covid-19 pandemic has wreaked havoc amongst global economies particularly India, compelling them to kneel down and seek mercy from one of the most challenging quandaries of all time. A common feature of any crisis is its devastating impact on the economic scheme of things and this one is no different. With revenues declining and prices of essentials rising, the heightened levels of economic lethargy are puncturing market sentiments, affecting operations and thereby aggravating the conundrum of the policy-makers.

For the uninitiated, India did not set her foot into the pandemic on a sanguine note with economic growth hovering around the weak 4% mark. The domestic currency (INR) saw some serious depreciation against the US Dollars during the first of 2020. India’s debt-to-GDP ratio crossed 70% coupled with the predictions of it reaching 80% by the end of the current fiscal year. These economic indicators were enough to paint the sorry picture of the Indian economy and were a preview to the hardships due to being faced by Asia’s second-largest economy.

Now, the Reserve Bank of India (RBI) in an effort to abate the money market crash flooded the system with liquidity, along with measures such as loan moratorium and restructuring. There is no doubt that India Inc. badly needs access to cheap money in order to lay its safety net, but the central bank needs to be mindful of the time-frame, this excess money is circulating in the economy.

To make sense of the problem, an illustration will help. Let us assume that there are 10 goods/services and 10 rupees in the economy. Therefore, 1 goods/service equates to 1 rupee. Thereafter, when the central bank infuses say 100 rupees partnered with no change in the number of goods/services, the tally gets skewed and now 1 goods/service equates to 11 rupees. This is inflation. There seems to be an artificial influx of prices, without any backing of production or consumption boost.

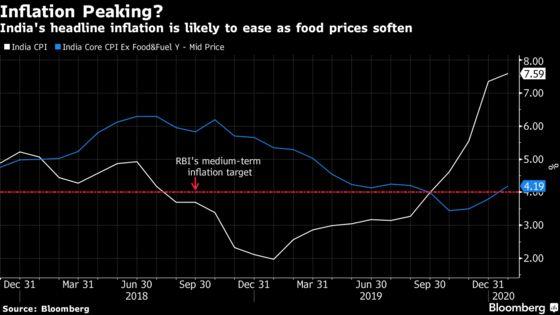

Having said that, the Mint Street, i.e. the RBI also has the powers to suck in the liquidity from the system when things go south. The central bank’s inflation target was 4%, with a range of +/-2% and the on-ground picture raises serious concerns. The July Consumer Price Index (CPI) stands at 6.93% way above their upper threshold. The unpragmatic Dalal Street rally on the back of massive retail participation also bears testimony to the liquidity boom in the status quo.

The question is what does the RBI do now? Does it seal the liquidity trap? The economists argue that the greater trouble lies in the way the central bank apportions this money amongst the participants of the economy. They propose to the RBI to render this money towards MSMEs and the Below-Poverty-Line (BPL) folks who would assist in expanding the production capacity of goods and services. Funding boost in programs such as the likes of the Public Distribution System (PDS), Mahatma Gandhi National Rural Employment Act (MGNREGA) will enable the lower strata of the society to assist in the growth story of India.

The problem that needs to be recognized in this entire episode is the way the Indian policy-makers have acted in the past. It is imperative for them to realize the vulnerability of the situation and not be dogmatic about their approaches. Also, it’s high time that the RBI and the Government of India (GoI) discover common ground as there exists a clear divide between the way the two concerned entities approach and act. Finally, while the economic indicators connote that currently, too much money is chasing too few commodities (inflation in other words), the only thing that is going to get the Indian economy out of the woods is a robust policy nomenclature.

Written by- Shyam Agarwal

Image & Statistical Sources:

- CNBC TV-18;

- Bloomberg.