It is often spurious to drive conclusions about the real economy from movements in financial markets. Traders in financial markets usually have conflicting interests and do not necessarily understand how the economy works. Unfortunately, we are constantly showered by their biased (sometimes flawed) analysis in newspapers and television which affects our decision-making and might result in the real economy coinciding with the markets (as is the case in severe financial crises).

Gold is one such commodity whose prices reflect traders’ assumptions about the state of the economy and whose prices might drive distorted decision-making. To understand why, first the reasons for purchasing gold have been discussed.

Why Traders Buy Gold?

Traders usually buy gold as a hedge against economic uncertainties. Such uncertainties can be inflation, risks of a recession, rising unemployment etc. Gold also serves as a good commodity for diversification and allows traders to hedge geopolitical risks. Therefore, Gold is often seen as an insurance for traders rather than a commodity by traders.

USD & Gold - A Brief History

From the discussion above, we note that Gold is often inversely related to the USD. A falling USD usually indicates macroeconomic uncertainty, hence Gold prices tend to rise when the USD falls and investors rush to add Gold to their portfolio whose price is usually not very volatile.

However, this relationship did not hold under the Bretton Woods system (see graph below) which was abandoned in 1971. Under this system, countries had a fixed exchange rate system wherein the values of other currencies were pegged to the US Dollar which was itself based upon Gold. Before this system was abandoned by President Nixon, the US government guaranteed to exchange a certain amount of Gold for US Dollars.

President Nixon’s decision to abolish the Bretton Woods System meant that fiscal policy was no longer constrained by taxation or public borrowing. The non-convertibility of US Dollars meant that the US government was not revenue constrained in spending anymore and public debt issuance became merely an ex-post monetary operation to help the central bank maintain its target rate (discussed ahead in more detail).

Gold Price Movements

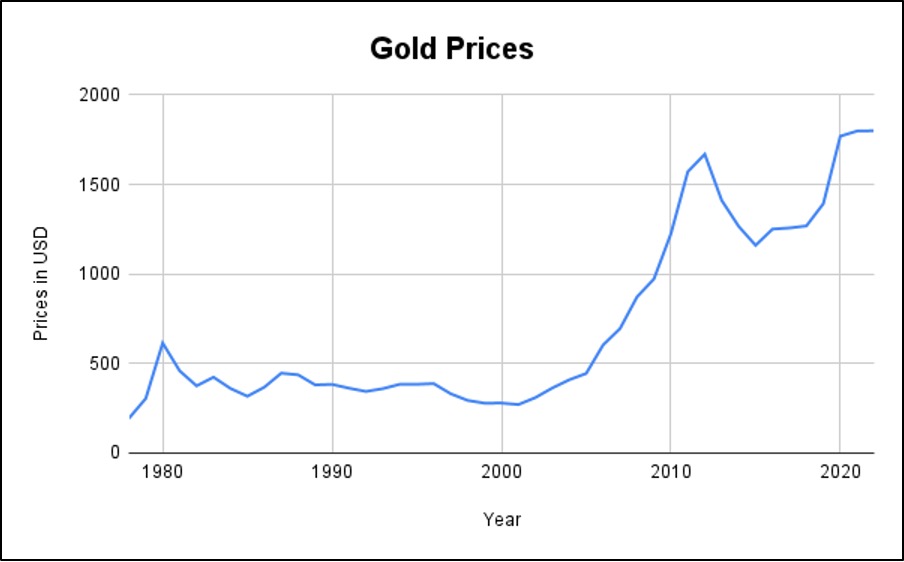

The graph below shows the changes in gold prices since 1978. Gold prices were relatively stable until the 2007-08 Financial Crisis – which explains why investors saw it as a good hedge- after which there was a huge surge in prices. While the US Dollar did depreciate relative to the Yen and Euro, this depreciation was too small to trigger such an escalation in prices.

The escalation in these prices coincided with the massive rescue packages such as the Troubled Asset Relief Program (TARP) were enacted. These packages, aimed at reviving the economy in the face of massive deleveraging from banks as they reeled from the crisis, increased the budget deficit of nations around the world.

Investors were likely jittered at the prospect of such packages (and deficits) accelerating inflation and leading to currency debasement. As noted above, investors usually hedge inflation risks by buying gold, which may explain the rise in gold prices.

Unfortunately, assuming that higher deficits will lead to inflation reflects a poor understanding of the functioning of an economy with a fiat monetary system.

The only thing such panic buying does is spread unnecessary and far-fetched fears about the economy which might feed into the decision making of normal citizens, especially if the media gives a platform to financial market participants to advance their views.

As the graph above shows, there is no backing to the claim that higher deficits necessarily lead to higher inflation. Consequently, the surge in Gold prices reflects an unwarranted panic and a poor understanding of monetary economics.

A far more rational escalation in Gold prices was seen in 2022 when investors, worried about the impact of the rate hikes from most central banks around the world, decided to buy Gold as a safe haven.

Deficits & Inflation

Inflation should always be an important concern for policymakers. The erosion of purchasing power and the uncertainty it causes mean that inflation control should always take priority for monetary and fiscal policy. Having said that, it is crucial for policymakers to not shy away from high spending to advance the nations’ welfare and protect the nation’s most vulnerable citizens due to an irrational fear of deficits. Deficits arise when government spending is in excess of its revenues. While many implicitly assume this to be a consequence of excessive reckless spending, it may simply be a consequence of declining tax revenues due to an economic downturn. In the aftermath of the 2007-08 crisis, the sharp cutback in economic activity required a strong fiscal injection which inevitably widened deficits. Such an increase in deficits and government spending did not trigger a rise in inflation simply because there was a high level of unemployment after the Financial Crisis which meant that there were enough real resources available in the economy to meet the increased demand.

Consequently, investors cannot simply assume deficits or government spending is inflationary. What matters for inflation is the availability of the economy to produce the goods demanded within its real resource constraint.

Asset Bubbles

The sharp rise in Gold prices after the Financial Crisis and in 2022 triggered concerns that there might be a bubble, similar to the Housing bubble in Western countries. While such fears were unfounded, the alarming rise in Gold prices shows the risks of relying on flawed macroeconomic theory. Investors who were irrationally (as shown above) concerned about inflation due to deficits, pushed up the prices of Gold even when there was no threat of an economic slowdown or inflation.

As the 2007-08 crisis showed asset price bubbles can lead to heavy losses for financial institutions. When such institutions face losses, they then cut back on lending. In this way, a crisis in the markets manifests a problem for the real economy when the lack of bank credit leads to a business slowdown, reduced demand and higher unemployment.

Therefore, prescribing to the wrong school of economic thought might create unnecessary bubbles which can spill into the real economy.

Bretton Woods & Implications for Fiscal Policy

The Bretton Woods system was similar to the gold convertibility present before World War 2. The system and its implications for the relationship between the USD and Gold have already been discussed above. However, President Nixon’s decision of abandoning this system had significant implications for fiscal policy across all nations. When the system was in effect, countries with a gold surplus were able to expand their money supply and stimulate their economies. On the other hand, deficit nations were forced into higher levels of unemployment.

Consequently, the system was not sustainable from a societal welfare point. In fact, many prominent economists like Bernanke and Romer blame the Great Depression on the gold standard. While the Bretton Woods system was different from the gold standard in the sense that the convertibility of the currency was now into US Dollars and not gold, the same deflationary dynamics described above applied to countries with low dollar reserves.

Therefore, abandoning the Bretton Woods system was an important step in the creation of monetarily sovereign nations that could now make expenditures without subsequent taxation or public debt issuance.

Now that nations did not need to maintain a fixed exchange rate, fiscal policy could play a more significant role in achieving the goals of full employment and price stability.

Therefore, it is now important to realise that governments are not constrained in any way in terms of spending. The reason why monetarily sovereign governments now issue debt is not for raising sources of funds but instead a tool for their respective central banks to maintain a control over their target interbank rates.

The issue of government debt in response to government spending helps reduce the excess reserves that the original government spending created.

Consequently, discussion in both policy making and financial markets should not assume that the macroeconomic consequences of fiscal policy remain the same in the fiat monetary system today as they were under the Bretton Woods system.

The sooner we realise this the quicker we will be able to use fiscal policy to achieve societal goals and prevent damaging asset bubbles.

Written by – Rohan Dubey

Edited by – Mir Irfan Ali