Almost a hundred years later, after adopting the socio-economic reforms by Mustafa Kemal (Kemal Atatürk), Turkey is entering into another impending economic crisis. The last major one being in 2000-2001, the question stands large as to why a country that identifies itself as an extremely important player in both, geopolitical and economic arenas is seeing a looming crisis again, within a short span of 20 years.

Being a part of a major economic forum like the G20, a founding member of the Organisation for Economic Cooperation and Development (OECD) and also the 20th largest economy of the world, Turkey had found itself a good footing economically and strategically. This was evident from its drastic reduction in poverty rates and growth into an upper-middle-income country since the 2000s.

The 2000-2001 crisis was caused mainly due to fragilities in the banking sector.

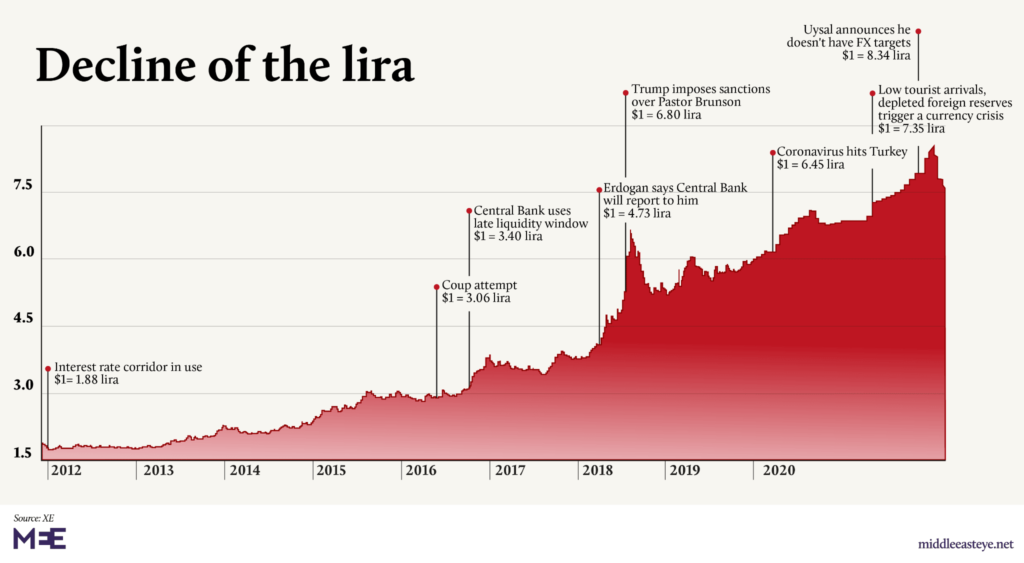

This crisis began by and large due to the lower interest loans issued even when the inflation had peaked to the double-digit of 54.4%, accompanied by an all-time high unemployment rate of 8.4%. Turkish lira then lost about half its value against the dollar. To top it off, the current account deficit due to the high oil prices also weakened the economy considerably. The crisis can be better understood by digging a bit deeper; during the 1980s. Turkey deregulated its financial markets and adopted an export-led policy.

This made the Turkish lira convertible and during the 1990s, following loose fiscal and monetary policies, it saw an increase in real growth and a rise in both external and internal public debt. High public debt and low level of savings caused dependency of the banking sector on foreign funds. In 1997, Turkey was struck by the Asian crisis, which worsened the already declining investors’ confidence in the economy due to macroeconomic imbalances, resulting in a huge capital flight. Finally, in the 2000-2001 crisis, capital outflows coupled with the banking crisis culminated into a currency crisis.

The International Monetary Fund’s (IMF) exchange rate based disinflation program, initiated in 1999, was in operation when the Turkish economy got hit by the banking crisis. After the crisis, a stabilization program aimed at rectifying the structural weaknesses was implemented in Turkey with assistance from the IMF. A comprehensive restructuring program for the banking sector, along with other macroeconomic reforms, was then kicked off. High economic growth rates achieved thereafter was mainly due to the inflow of short-term finance capital to Turkey, following high-interest rates in the asset market.

Over-supply of foreign exchange did overvalue lira, triggering massive imports, which ended up in large trade deficit and external debt. Dependence on cheap imports obviously led to lesser demand for domestic goods, reducing domestic production and employment. Thus, post-crisis adjustments pulled the economy to a high growth rate but with no jobs, high debt and widened trade deficit.

The present looming crisis yet again portrays the same phenomenon of the early 2000s. The highlight being cheaper loans, especially to the real estate sector, and to the tourism sector; which even though used to be a major contributor to employment generation and GDP, could not reboot itself due to the COVID-19 pandemic.

Apart from the boom initiating cheap domestic loans, the real estate sector itself had been at the receiving end of foreign investment and debt denominated in US dollars, whereas the lower profits earned were in the Turkish lira. The cost of servicing the debt became expensive, ultimately leading to the devaluation of the Turkish lira at present. The country has a larger import bill due to the major imports of oil and gold.

Turkey seems to be engulfed in a vicious circle of economic crisis. But, this time, this vicious circle has enlarged itself to include geopolitical and diplomatic ramifications as well.

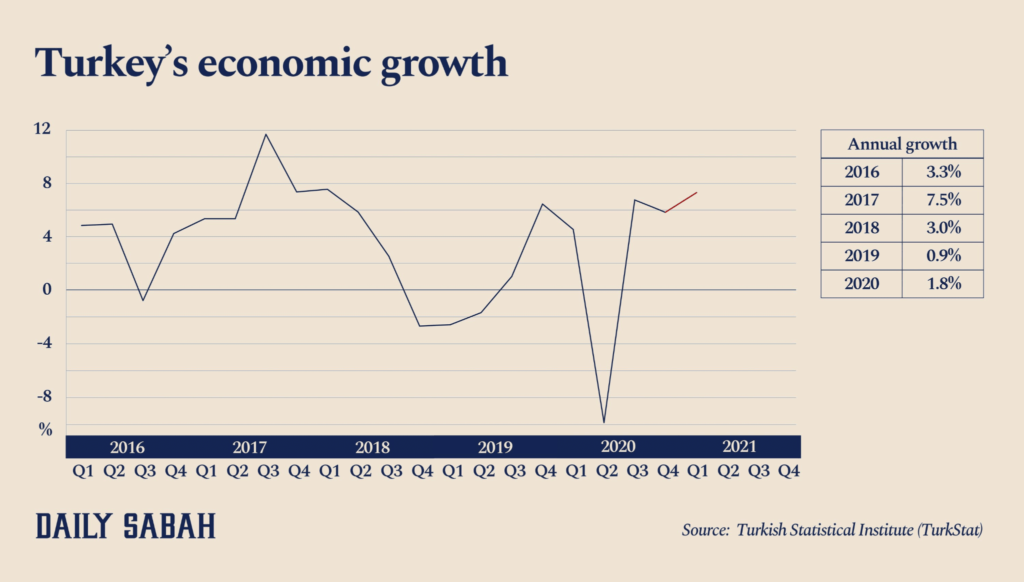

What has been called an interference against the ISIS in Syria has put Turkey neck-deep in political pressure. The SIPRI report stated that the military expenditure of Turkey seems to have spiralled to 77% between 2011 and 2020. This could be attributed to the aggressive foreign policy followed by Turkey. The year 2020 saw an exception, with a reduction of 5% in military expenditure. Whereas the same level of expenditure has not been channelized towards other sectors like agriculture, manufacturing or the social sector development. Even though the service sector has been the backbone of the economy, with tourism generating a share of 12.7% of GDP in 2019, it has taken a hard blow due to the pandemic.

The impending crisis, though aggravated due to the pandemic situation, had already been giving out signals in various forms, especially in the banking sector. Increasing stressed assets, putting pressure on the financial sheets of banks, a high Corruption Perception Index of 91 (2019), the war in Syria, so on and so forth, has expedited the events ultimately leading Turkey to be on the GREY list by the Financial Action Task Force. The expulsion of diplomatic ties with major countries including France and Germany is also being claimed as means to eclipse the economic crisis.

The Government’s policy to keep the interest rate low at such a crucial stage will only make the poorer pay a larger price. The purchasing power has reduced drastically, the existing low rates will reduce it more, pushing more people to extreme poverty. The immediate step that Turkey needs to look for is to raise its interest rate, through a strongly autonomous Central Bank as well as have a multi-stakeholder approach when it comes to the financial tasks ahead.

The banking sector needs a better and more independent financial regulating mechanism to look into the vulnerable position of the banks. Restructuring of loans is the need of the hour due to the growing issue of stressed assets. A more transparent route needs to be put up in the banking sector which can build investor confidence. This again is highly crucial since the foreign investment in Turkey is characteristically hot-money.

Even though agriculture accounts for almost 25% of the labour force, its contribution to Turkey’s Gross Domestic Product (GDP) over the decade has declined. This has been mainly due to the focus on the service sector where foreign investment was intensively used. The OECD Evaluation of Agricultural Policy Reforms report calls for a policy change so as to increase competitiveness with respect to agricultural output. On the same lines, since Turkey does not have the boon of natural gas and oil fields, (and hence, its large import bill), it is all the more relevant that it transitions its sectoral importance from tourism (services) and military to agriculture and manufacturing.

The mechanisms initiated by Turkey to absorb the shocks of the pandemic was well received. As a response to this, the labour market has shown signs of recovery. But a large part of the population including the unskilled workers and women were left out. Formal employment was seen to be rather low. The year 2020 saw an increase in the poverty rate from 10.2% in 2019 to 12.2%. This was also due to the impact of COVID-19 which has widened the gender gap.

Inclusive growth is also a major thrust area for Turkey to focus on to strengthen the economy. Households and other smaller firms need to be adequately given room for growth by prioritising loans. The manufacturing sector is one where Turkey needs to improve so as to be better inculcated as a part of the global supply chain.

Also, since the world economies are seeing inflation, it is expected that liquidity will be tightened by the developed economies, which will again strangle the countries excessively dependent on foreign investments. A major sectoral realignment is what Turkey should focus on. There is an urgent need for a stronger macroeconomic framework, one which can help it move past this vicious circle of crisis.

All said and done, it needs to be said that each case of debt-currency crisis varies depending on the mandates by the Central Bank regulators. If having a large foreign exchange reserve exists, which can source itself, then, along with an increasing interest rate, Turkey’s economy can be fetched out of its crisis. In the case of Turkey, to be a major geopolitical player, the required thrust should come from a stronger macroeconomic agenda, one which can help in breaking off the vicious circle of crises.

Written by- Durga Balakrishnan and Dr Liji Lakshmanan

Edited by- Ubai Sura