Oil and gas sector is among the eight core industries in India and plays a major role in influencing the decision making for all the other important sections of the economy. India’s economic growth is closely related to its energy demand, therefore, the need for oil and gas is projected to grow more, thereby making the sector quite conducive for investment.

Recently, there has been a large spike in the petrol price, reaching up to Rs. 100 per litre in India. Petrol and diesel prices hiked by 35 paise per litre each- the steepest in recent times, according to a price notification of state-owned fuel retailers. The hike on Saturday is the 30th increase in prices since May 4. In 30 hikes, the price of petrol has risen by Rs 7.71 per litre and diesel by Rs 8.12 a litre. While the usual blame-games and criticisms have begun among the political parties, let us excavate the deeper truth and the factors that have led to this spike.

The main factors are the mismanagement of OPEC in regulating international prices, the taxes imposed on the oil, the Covid-19 pandemic, oil bond signed by the previous Government.

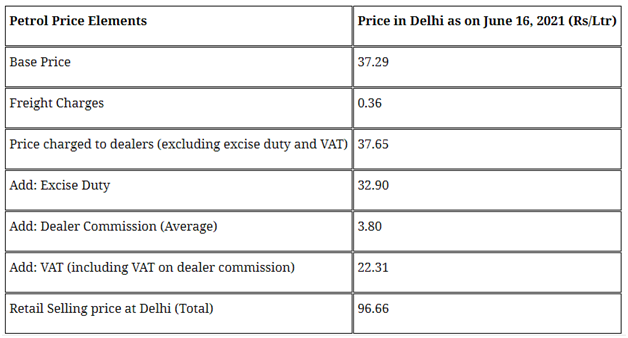

State and central taxes account for about 58 per cent of the pump price of petrol and 52 per cent of the pump price of diesel in the national capital recently. The central government had in 2020 hiked central excise duties on petrol by Rs 13 per litre and those on diesel by Rs 16 per litre to shore up revenues as economic activity fell due to the pandemic. In 2010, the prices of petrol were determined by the government and were revised every fortnight.

In 2014, the price of diesel was also deregulated and since 2017 prices are being revised on a daily basis. Since then, the public sector Oil Marketing Companies make decisions on the pricing of petrol and diesel based on international product prices, exchange rate, tax structure, inland freight and other cost elements. Currently, the central and state taxes make up for 60 per cent of the retail selling price of petrol and 50 per cent of diesel. Centre levies Rs. 32.90 per litre of excise duty on petrol and Rs 31.80 per litre. The recent developments have lead to increase in price up to Rs.100 in states like Tamil Nadu, Karnataka, Maharashtra, Madhya Pradesh, etc.

The current taxes levied being one of the reasons, the rise in oil price also has a connection with the oil bond made by the previous Government. Oil bonds are issued by the government to compensate oil marketing companies (OMCs), fertilizer companies and Food Corporation of India (FCI) for losses borne by them in the process of regulating prices, similar to government securities having a long maturity period extending over 15-20 years with interest.

The then Congress led UPA government took to oil bonds rather than subsidies as an alternative to regulate the fuel prices between 2005- 2009. Dramatic surge in crude oil prices coupled with the shock of 2008 Global Financial Crisis, were cited as reasons behind this move as the government thought to make payments to the OMCs in a staggered manner through the capital raised through these bonds and simultaneously shield the customers from the unprecedented escalation in prices of fuel.

According to reports, the government issued bonds worth Rs. 1.4 lakh crore, thereby prolonging the burden of financing subsidies.The current government is all set to redeem Rs 1.30 lakh crore UPA era oil bonds to public sector oil companies in lieu of the subsidies borne by them. A Principal Installment of Rs 10,000 crore will come up for repayment this fiscal year, the first since 2015.

In addition to this, due to covid pandemic, there was a demand shock which led the rate of crude oil to go down in negatives as the supply was much more, to which the OPEC cut the oil supply. But gradually, there was a sudden rise in demand which the OPEC failed to notice and hence leading to decrease in supply which gradually led to soaring up of prices.

The immediate solution might be cutting down the tax levied on petrol and diesel which might be the need of the hour for middle class households and economically weaker sections. However, there are chances of reverse effect in future. So, we should focus on long term goals by trying to shift to more reliable source like electrical energy, hydrogen fuel gradually reducing the number of vehicles dependent on petrol or diesel.

The Government has adopted several policies to fulfill the increasing demand. It has allowed 100% Foreign Direct Investment (FDI) in many segments of the sector, including natural gas, petroleum products and refineries among others.

In February 2021, Prime Minister Mr. Narendra Modi announced that the Government of India plans to invest ~Rs. 7.5 trillion (US$ 102.49 billion) on oil and gas infrastructure in the next five years. The Government is planning to set up around 5,000 compressed bio-gas (CBG) plants by 2023.

The Ministry of Petroleum and Natural Gas released an ‘Ethanol Procurement Policy’ on a long-term basis under the ‘Ethanol Blended Petrol (EBP) Programme’ (October 11, 2019), which covers modalities for long-term ethanol procurement, proposed mechanisms for long-term procurement contracts, pricing methodology and other topics and many more schemes. The solution for this problem is to reduce our dependency on oil and slowly shift to alternative means of energy resources since this is an exhaustible source of energy.

Written by- Venkatavardhan S

Edited by- Radhika Khandelwal