Bailouts are the provision of financial help given by an individual, business, or Government to another company or Government. This is done when the concerned party is on the verge of bankruptcy. Not every bankruptcy needs to be bailed out; bailouts are only done when the potential fallout from bankruptcy is huge. For example, during the financial crisis of 2008, banks had to bail out or collapse the entire financial system. Similarly, during the auto-industry crisis of 2008-10, General Motors and Chrysler were bailed out because the American Senate thought that potential losses of jobs could outweigh the cost of bailouts. In the same way, governments can be bailed out too but only a few organisations are big enough to do so.

International Monetary Fund

IMF was one of the twin Bretton Woods institutions created after World War 2 along with the International Bank Reconstruction and Development (World Bank). The main reasons for its creation were:

Help Governments oversee fixed exchange rates that emerged after World War 2 for stabilization in international trade.

Provide short-term capital to help manage the balance of payments crisis to prevent the international spread.

Help provide capital infrastructure for any infrastructure projects.

The World Bank was tasked with providing capital to developing countries for any short or long-term infrastructure projects. However, it was the IMF instead which gradually emerged as the lender of last resort for countries with a BoP crisis. Beginning with the assistance given to European countries in 1952, with similar aid packages being given to the UK in the British Sterling Crisis (1967), and to Mexico in the Mexican Peso Crisis (1976). This trend continued with the IMF extending out loans to several Asian Countries in the Asian Finacial Crisis of 1997 and the Greece Eurozone Crisis in the 2010s, firmly establishing the IMF as the lender of the last resort to the World.

How Does This Work?

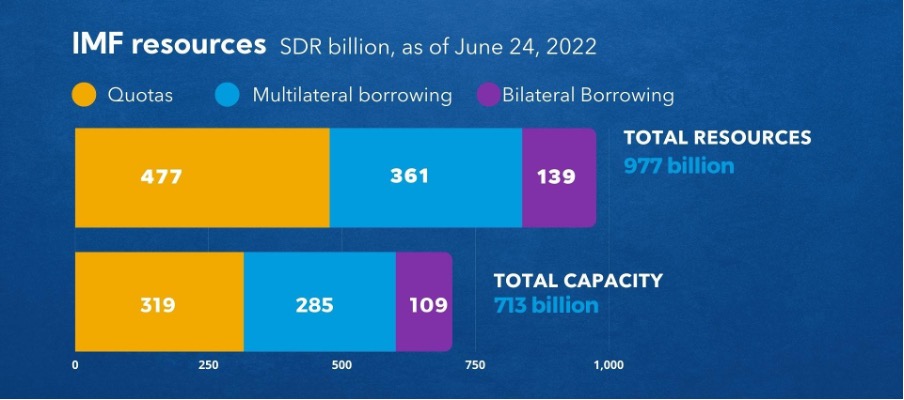

How does IMF generate enough money for lending? Generation of funds can be done through member quotas, New arrangements to borrow (NAB), and bilateral arrangements.

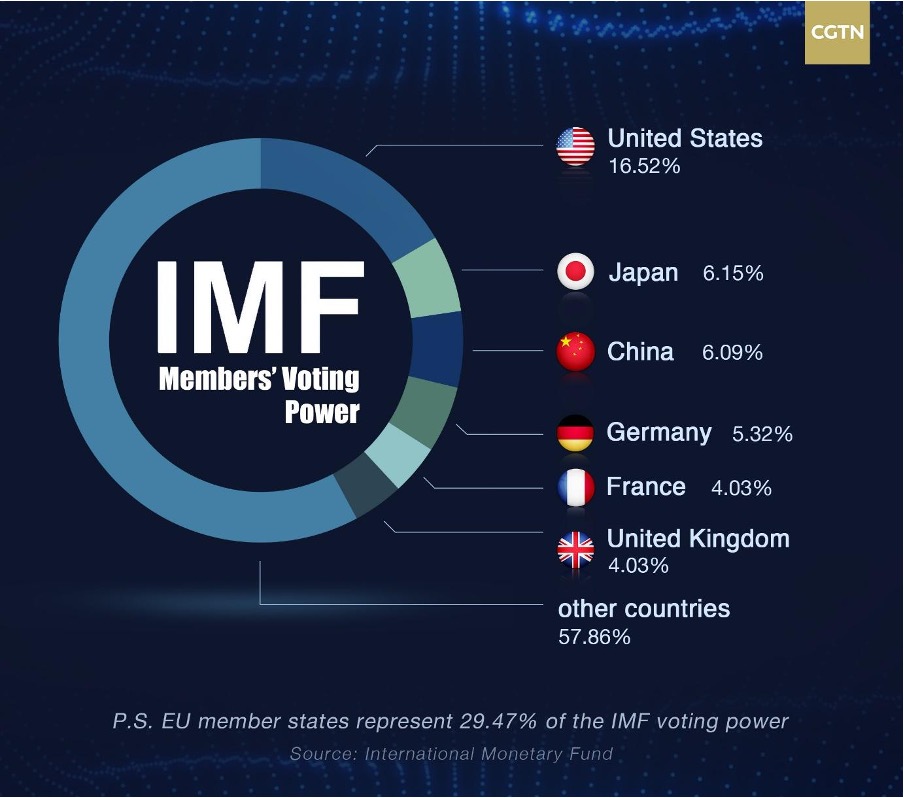

Member Quotas are determined by the amount of funding, each country contributes to Special Drawing Rights (SDRs). Special Drawing Rights are international reserve assets comprising The US Dollar, Yen, and Pound. It represents claims on the currency by member nations. The more a member country contributes, the bigger the claim on SRDs.These claims on SDRs also determine the voting powers within the organisation. The bigger the contribution, the greater the voting powers on policy matters. Normally, the extent of the quotas matches the political and economic power of countries. Currently, the US has the highest voting strength within the IMF.

Member quotas are the major sources of funding. New Arrangement to Borrow (NAB) is the fund to mobilise new funds from member nations. This is a separate provision from member quotas.

Bilateral Borrowing Arrangements serves as the third line of defence after member quotes and new arrangement to borrow. This involves a method of raising funds through bilateral meetings with individual member nations. Contributing through this route doesn’t affect voting powers.

Benefits

Since most countries that turn to IMF for borrowing often face a BoP crisis, it must raise the question of the loan terms and conditions that places the country in the hands of the IMF. Does the loan help in reforms and economic growth or is the country trapped in a debt cycle?

Evidence suggests that generally, the effect of the lending-both short-term and long term tends to be positive. This seems intuitive since the condition for most IMF loans force Governments to make stabilisation and structural reforms. These reforms include fiscal prudence, opening up international trade, cutting tariffs, and creating a business-friendly environment overall.

The literature on this suggests that there is decreased inflation and better price stability in the long run. Thus, corroborating the role of engagement in restoring macroeconomic stability. With excessive Government spending under control, tax collections increase and later create greater spending on responsible social welfare programs. An increase in FDI inflows along with greater openness of the economy helps in increasing the growth rate of Real GDP per capita. Many countries including India’s famed liberalisation efforts of 1991 have seen poverty rates decline following the reforms.

Criticisms

While we have seen that IMF bailouts largely benefit a country, there are still many concerns associated with this lending process. One of the criticisms that the organisation has faced is that the conditions it imposes in return for lending are too strict. High-interest rates, fiscal austerity, trade liberalisation, and privatisation have been devastating for the local population. These policies may help the country in the long run but the short-term costs of these measures may be too large to ignore. This can be seen in the instance of Pakistan, where the IMF’s condition of removing its highly subsidised electricity distribution sector lead to blackouts for many in the country.

Also, it has been argued that while IMF may have had successes in dealing with financial crises in countries like India and Mexico, its attempt to impose the conditions it had employed in its playbooks in several African countries revealed that it was out of touch with ground realities. In some cases, such as in Greece the implementation of its policies may have even caused contraction.

Another risk the IMF lending creates is the possibility of moral hazard at a national scale. Moral Hazard refers to the situation when one party operates in bad faith with the other party of the contract. For example, a country may spend its borrowed amount on more subsidies and sops of the public instead of using it to reconfigure the economy.

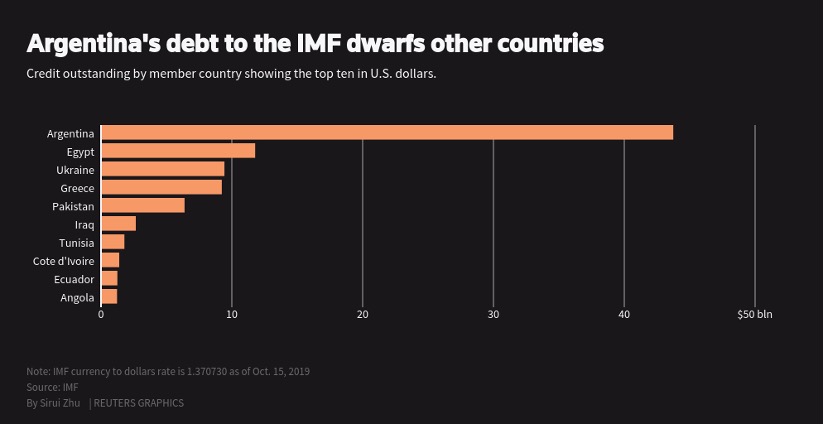

Case Study: Egypt

The selection of Egypt for this case study is undoubtedly not an unbiased one. The author wanted to choose a country where there are negative repercussions for the country since the other side of the debate is covered in detail and known (The Indian Case).

The Egyptian regime had spent years the country’s credit to fund a plethora of poorly-planned megaprojects that were often contracted to its own regime-backed companies. The state became saddled with debt when these companies had to pay no corporate tax at all.

In 2016, the IMF started a new loan program for Egypt. However, it did not raise any restrictions on this infrastructure building by private firms. Egypt was able to borrow even more money due to the IMF’s constant praise of Egypt’s financial reforms.

In 2020, Egypt had to turn to the IMF again for cash injections of $8 billion despite having “completed” the program in 2019. Overall labour force participation had declined from 47 per cent in 2016 to 42 per cent by 2019, and during that time, labour force participation declined especially among women and youth, dropping from 23 per cent to 16 per cent and from 30 per cent to 22 per cent, respectively. The IMF said its 2016 loan would promote “inclusive growth.” In 2016, the poverty rate was 27.8 per cent, increasing to 29.7 per cent in 2019-20, according to government statistics.

The case of Egypt warns us of the danger lending on such a large scale poses.

Writer – Anivesh Kashyap

Editor – Saba Godiwala