The main purpose of creating any index is to highlight/identify the trend of a particular market or sector (Digital Payments sector in the case of RBI-DPI) and compare it to a particular benchmark or goal. Through an index it is easier to judge the performance or growth of the underlying asset/institution (Since 2018 the RBI-DPI was up by 270.59%, meaning digital transactions in the country based on a consolidated basis had increased by 270.59% since March, 2018 upto March 2021).

As on 28th July, 2021 the Reserve Bank of India – Digital Payments Index (RBI-DPI) was up by 30.19% (i.e. from 207.84 in March 2020 to 270.59 in March 2021) which reflected a significant growth in the quantum of cashless transactions undertaken in the country.

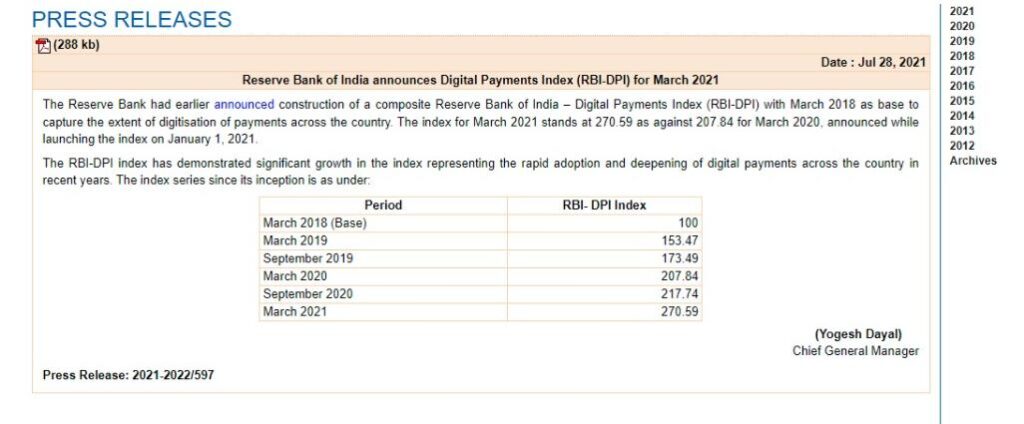

The Reserve Bank of India (RBI) had earlier announced the construction of a composite Digital Payment Index with the aim of capturing the extent of digitalized payments i.e. cashless payments and also tracks their overall growth across the country. For the purpose of this index, March 2018 has been taken as the base year (i.e. as on March2018 the index value would be 100) and the index has grown since as follows:

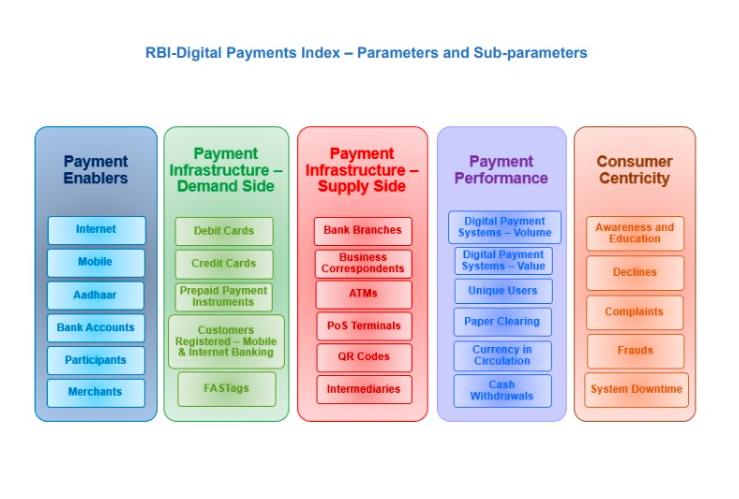

It was in the Statement on Developmental and Regulatory Policies released by RBI on 6th February, 2020 under Part IV – “Payment and Settlement System” where it was announced that in order to track the on-going growth of digital payments in the country, RBI would construct a composite “Digital Payments Index” and that it would be based on multiple parameters which would reflect the overall impact of and growth through digital payment modes. The 5 broad parameters (along with their respective weights) of RBI-DPI are as follows:

1) Payment Enablers (25%),

2) Payment Infrastructure – Demand-side factors (10%),

3) Payment Infrastructure – Supply-side factors (15%),

4) Payment Performance (45%) and (v) Consumer Centricity (5%).

Each of these parameters has sub-parameters which consist of various other measurable indicators. A further break-up of these parameters has been captured in the following chart:

Over the last few years, the Central Government has started various digital initiatives which encapsulate the spirit and intention of the government towards making India a cashless (digital) economy. Some of these initiatives can be summarized as follows:

1) Aadhaar Enabled Payment System (AEPS) – It is a payment system which seamlessly enables financial transactions through an Aadhaar-based authentication. Through this payment system users can transfer funds, make payments, deposit cash, make withdrawals, make enquiry about bank balance, etc.

2) DigidhanAbhiyaan – An initiative which was introduced to help users undertake real time digital transactions.

3) PayGov India – Being a national payment service platform it provides users with end-to-end transactional experience along with a payment gateway interface for online payments. It also provides a facility through its national and state portals to make online payment using net banking, credit cards and debit cards.

4) PradhanMantri Jan-DhanYojana (PMJDY) – An initiative which was introduced to provide access to basic banking facilities to each household in the country. Access to financial literacy, access to credit, insurance and pension facility were also made available.

The Unified Payments Interface (UPI) payments recorded an 82% jump in volume and a 99% jump in value during the second quarter (Q2) of 2020-21, which was the same when compared with the second quarter (Q2) of 2019-20, according to the Worldline India Digital Payments report.

Further, around 19 banks joined the UPI ecosystem which brought the total number of banks under the UPI ecosystem to 174 and also the BHIM (Bharat Interface for Money) app (another initiative which enables direct bank-to-bank transfer using one’s mobile number or payment address) was made available to customers of 146 banks. Lastly, in Q2 of 2020-21 around 0.52 crores of Point of Sale (PoS) terminals were deployed by merchant acquiring banks (banks that processes payments on behalf of merchants), which was 13% higher than what was achieved in Q2 of 2019-20.

Although the National Payments Corporation of India (NPCI) already publishes data on digital payments, it is for the very first time that RBI has published these details. In one of its press releases the RBI has stated that the RBI-DPI data will be published on its website semi-annually from March 2021 onwards with a lag of 4 months.

Written by- Nozer Irani

Edited by- Jasmine Kaur Bhatia